Student Loan Bubble: Not as Bad as It Looks

Here's a scary headline from yesterday: "Student loans soar 275% over past decade."

It's true. Total student loans outstanding were $241 billion in 2002. Today, it's $904 billion, and it shows no sign of slowing down. "Student loans could be the next housing bubble," former Labor Secretary Robert Reich said in March.

He may very well be right, but there's another side to this story.

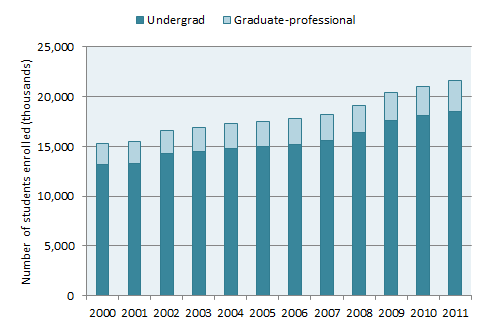

Yes, total student loans have surged over the past decade. But what else happened during that time? The number of students enrolled in colleges jumped 40%:

Source: National Center for Education Statistics.

The rise in college attendance has been ongoing for decades, but really spiked in recent years -- particularly among graduate students. As the jobs market dove in 2008, armies of recent college graduates ran to grad school in lieu of an employment market that had no room for them. In 2009, the number of people taking the LSAT (law school entrance) exam jumped 20% from the year before. The number taking the GRE (standard grad school entrance) exam popped 13% last year. "When job creation slows, there's an increase in the number of people who pursue a graduate degree," TheNew York Times reported two years ago.

Take that into consideration, and about one-third of the increase in total student loans over the past decade can be attributed to more people attending school, not an increase in the per-student debt burden.

What else happened over the past decade? Average weekly wages for those with a college degree increased 24.9%, according to the Bureau of Labor Statistics. That has to be factored in when comparing debt levels. The burden of $900 billion of student debt today just ain't the same as it was a decade ago. And a lot of the debt is being taken on for a good, rational reason: The average worker with a college degree now earns more than twice the wage of a high school grad, and wages for college grads increased faster than those without degrees over the past decade.

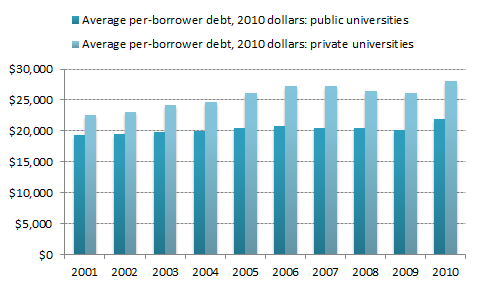

A great paper from the College Board puts these figures in the right context, calculating the average student debt among recipients of bachelor's degrees, per borrower, adjusted for inflation:

Source: College Board, Trends in Student Aid, 2011.

Is there an increase? Yes. Is it stratospheric? For the most part, no. In real (inflation-adjusted) terms, average per-borrower debt increased from $19,500 in 2001 to $22,000 in 2010 for students at public schools, and from $23,000 to $28,100 at private schools. The College Board offered more perspective:

"From 1999-2000 to 2009-10, average debt per borrower among public college bachelor's degree recipients increased at an average annual rate of 1.1% beyond inflation."

"From 1999-2000 to 2009-10, average debt per borrower among private nonprofit bachelor's degree recipients increased at an average annual rate of 2.2% beyond inflation."

That's hardly bubble territory. Mortgage debt during the housing bubble was increasing at more than 10% above the rate of inflation. And a lot of the rise in student debt above the rate of inflation can be rationalized by the fact that average wages for college grads have grown faster than inflation.

So what are we missing here? For-profit schools, such as Apollo Group (NAS: APOL) and DeVry (NYS: DV) .

College Board explains: "Students who earn their Bachelor's degrees at for-profit institutions are more likely to borrow than those who attend public and private nonprofit colleges, and those who borrow accumulate higher average levels of debt."

In 2009 (the latest year there's information on), only 16% of students at for-profit schools were debt-free, and 65% had more than $28,000 of student loans. At public schools, the same numbers were 40% and 14%, respectively. Iowa Sen. Tom Harkin shares another startling statistic: For-profit schools originate about 10% of student loans but account for nearly 50% of defaults. That's where there's excess, and maybe even a bubble.

Make no mistake: College is getting more expensive, and debt is going up any way you slice it. But for debt among students at not-for-profit schools -- which makes up the majority of college attendance -- it's hard to say we're at a bubble just yet. The numbers haven't changed that much in the past decade.

For more on how the recession affected the economy, check out my e-book, 50 Years in the Making: The Great Recession and Its Aftermath for your iPad, Kindle, or Nook on Amazon or Barnes & Noble. It's short, packed with information, and costs less than a buck.

At the time thisarticle was published Fool contributor Morgan Housel doesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.