This Is What the Death of Coal Looks Like

You may have heard recently that coal is dead. Everyone from BusinessWeek to Standard & Poor's has been pointing out the many reasons to think the coal industry is on its last embers:

In 1985, coal accounted for 57% of all power generated in the United States. It recently fell to just 34%.

According to the Energy Information Administration, Henry hub natural gas fell to $2.22 per million British thermal units in March, making it a significantly cheaper power source than coal, which sat at $2.41 per million BTUs.

Since just August of last year, the coal export price index has fallen more than 25%.

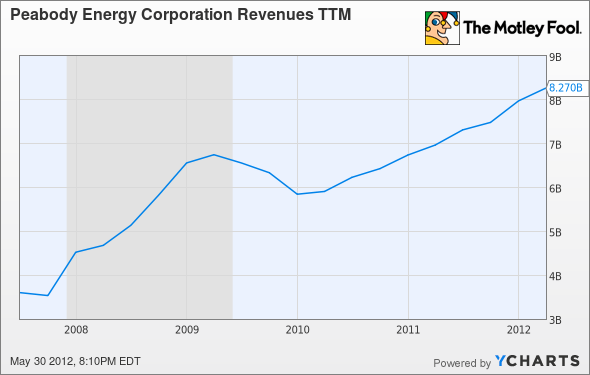

But here's a different stat to think about: revenues at Peabody Energy (NYS: BTU) for the past five years. This is what the death of coal looks like:

BTU Revenues TTM data by YCharts

B-b-but it's unpopular!

According to the EIA, natural gas is rapidly replacing coal as a source of power generation. Southern Co. (NYS: SO) , the largest electric utility in the U.S. by market cap, has cut its coal use by more than a quarter over the last five years, and in that same period, natural gas has risen from 15% to 30%. Peabody gets 82% of its sales volume from such customers, so how can the company's revenues possibly be going up?

Well for one thing, even as less coal is being used, the price of coal is rising to compensate. Southern Co.'s cost of coal fuel per kilowatt-hour has risen 54% over the last five years, easily offsetting its decreased use. It's possible that domestic generators have been converting the low-hanging fruit as well. Coal may be on the decline, but it's still the most used fuel source in a massive electric grid. Fellow Fool Sean Williams recently noted that according to the Aspen Environmental Group, it would cost $743 billion to convert all of the country's coal power plants into natural gas capable plants -- about 15 times more cash than most of the publicly traded electric utilities in the U.S. have combined.

A glowing future ahead

It will be years before the utilities can even afford to convert that many plants, much less secure the regulatory approval for all the necessary construction and infrastructure additions. In the meantime, Peabody has been getting an increasing slice of its sales internationally and worrying less about fickle domestic generators.

At its current rate, Peabody may get less than half its sales domestically within a couple years. The popular idea is that most international coal demand will come from China, as its rapidly expanding economy demands increasing amounts of energy, not to mention metallurgical coal for steel production. Fellow Fool Travis Hoium thinks import caps and a Chinese fracking boom will put a wrench in that thesis, but I'm not particularly worried -- China isn't even mentioned in Peabody's list of top countries by revenue, so declining demand from the country isn't likely to impact the company much.

Japan, however, has been boosting its coal imports considerably after shutting down all of its nuclear power plants in the wake of last year's Fukushima disaster. Japan was the world's top coal importer in 2010, and that was before it needed to replace a fuel that produced nearly a third of its energy.

Meanwhile, India is another of Peabody's top export destinations. A staggering 300 million Indians currently have no access to electricity, in part because of poor infrastructure and lack of generative capacity. Much of India's current capacity comes from coal, but India's natural coal resources have a high ash content, meaning that the country still needs to import large amounts of higher-purity coal like the kind mined in the U.S.

A simple value opportunity

While we may have so much natural gas we're running out of places to put it, we simply don't have the resources to use it yet. Union Pacific (NYS: UNP) Chief Executive Officer Jack Koraleski recently pointed out that gas plants are already running at capacity, and domestic generators will still have to turn to coal to fill electric demand. Union Pacific gets nearly a quarter of its revenues from hauling fuel, so Koraleski knows a thing or two about coal demand. And with countries like Japan and Germany turning their backs on one of their biggest fuel sources, coal is inescapable for now.

Coal companies, on the other hand, are priced like someone just figured out cheap and reliable fusion power. Peabody is priced just above tangible book value, while Alpha Natural Resources (NYS: ANR) and Arch Coal (NYS: ACI) trade for less than half their liquidation value. That might make Peabody look like the expensive one of the bunch, but with the only steadily rising profits and a P/E of about seven, far lower than competitors, I'd say it's pretty darn cheap, and I'm not alone. I made a Peabody CAPS pick a month ago that's already been clobbered, but the stock is only cheaper now. Add it to your wishlist today to follow the Foolish coverage.

You may be wary of Peabody after its continuing decline, but don't let it turn you off to energy investing completely. The Motley Fool has a new free report featuring the only energy stock you'll ever need. Read it today, and Fool on!

At the time thisarticle was published Fool contributor Jacob Roche holds no position in any of the stocks mentioned. Check out his Motley Fool CAPS profile or follow his articles using Twitter or RSS. Motley Fool newsletter services have recommended buying shares of Southern Company. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.