Analyst Debate: Is Hewlett-Packard a Top Stock?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "Motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today, we'll be discussing PC maker and networking provider Hewlett-Packard (NYS: HPQ) .

Hewlett-Packard by the numbers

Here are some facts about Hewlett-Packard to better acquaint you with the company:

Market Value | $44.9 billion |

Price/Book | 1.09 |

Forward P/E | 5.1 |

Cash/Debt | $8.3 billion/$30.1 billion |

Revenue (TTM) | $124 billion |

Net Income (TTM) | $5.23 billion |

Revenue Breakdown (MRQ)* | Personal systems: 30.8% |

Competitors |

Source: HP press release; Yahoo! Finance; author's calculations. Most recent available statistics given. TTM = trailing 12 months. MRQ = most recent quarter. *Figures do not add up to 100%, as they are based on consolidated net revenue following the elimination of $889 million in intersegment revenue.

Sean's take

What a disaster! Hewlett-Packard is just the latest example of what happens when a company becomes complacent and fails to innovate.

A major shift toward smartphones and tablets is underway, which has made the company's line of PC products, and even its networking components, largely obsolete. HP isn't the only company feeling the pain: Networking provider Cisco Systems recently cautioned that European spending would be weaker than originally anticipated, and Dell confirmed the trend that's making its PC products about as hip as Al Gore on Saturday Night Live. IBM appears to be the only PC maker seeing the advantage in cloud-based computing, and it has invested heavily in its future.

But is it too late already for HP? Former eBay CEO Meg Whitman doesn't think so, and she unveiled the first step in turning the company around last week. This step involves an all-out slash-fest -- axing 27,000 jobs, or roughly 8% of its global workforce, over the next two years, with 9,000 job cuts coming by October. This is being done to save up to $3.5 billion annually, but it will do little good if HP's long-term growth rate is 2% or less.

The company is facing huge inroads that I'm not certain it can conquer. For one, Amazon.com's EC2 pay-as-you-go and S3 storage platform have a huge head start on anything HP has put out, and it's the model by which other cloud companies base their platforms. Second, HP is already behind the eight ball with nearly $22 billion in net debt. Don't get me wrong -- the company is profitable, but it will need to rein in costs in order to preserve its profits, and laying off 8% of its workforce is the only way to do that. It's extremely difficult to grow while contracting a large chunk of your workforce. Finally, with half its revenue coming from low-margin personal computers, notebooks, and printing and imaging products, it will take an eternity to reinvigorate the company's bottom line.

I don't doubt HP will remain profitable, and it may even try to entice investors with a hefty dividend. But even though I rated the company "outperform" in my CAPS portfolio a while ago, HP seems like fool's gold now. At just five times forward earnings, I wouldn't bet against it, but I definitely don't consider it a buy here.

Alex's take

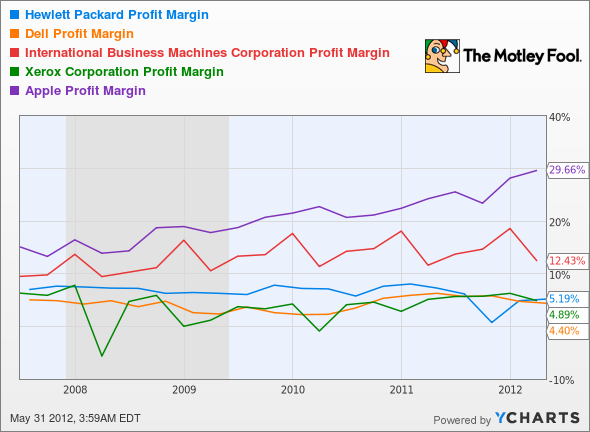

HP is the modern Xerox (NYS: XRX) . It built its current empire on the strength of innovative hardware and then became so bogged down in defending its claim that it forgot to push forward. Its primary revenue streams are commodity products with razor-thin margins -- just like Dell and Xerox.

HPQ Profit Margin data by YCharts.

On the other hand, IBM and Apple represent what HP wants to be -- and what it might have been with any real commitment to innovation. Both companies have seen margins grow by doing the exact opposite of HP: focusing on the service and the experience. That's why both have been outperformers, while HP continues to fall. HP, much like Xerox before it, seems to have no idea how to handle the technological transformation that's destroying its future. Sure, Xerox still exists. But, like HP, it fought yesterday's battles and lost tomorrow. In more than two decades, its share price has risen less than 20%, while the S&P 500 has become a three-bagger.

And what is HP doing to fight today's battles to win tomorrow? Cutting thousands of jobs, marginalizing its research and development, and staying the course -- which includes adding British software maker Autonomy to the ranks. The previous major acquisition became a running joke, and its latest doesn't have many good omens waiting. Autonomy CEO Mike Lynch has already been forced out, and IBM's response to the move was more or less to point and laugh. Remember, this was supposed to help HP on its path to becoming another IBM, with software and services and support (oh my!).

Meg Whitman is just the latest CEO to step out of the revolving door and into the corner office. Managing HP won't be comparable to her eBay stewardship. HP is a lumbering titan in a mature industry, while eBay was a first-mover in a very young industry. eBay is hardly known for its innovation, either. Its core business has scarcely changed in years. Whitman was a capable captain in the sun with the wind at her back, but HP sails in stormy waters. Whitman has two choices: She can help HP evolve or allow it to become a fossil. Even if it does adapt, there's little promise that such an evolution will help it fly again.

HP's valuation is at its lowest point in years. The same can be said of many tech companies, including Apple -- but Apple is enormously profitable and should still have growth ahead. I don't see similar growth for HP, and I don't see any indication that its leaders have any idea how to handle its problems. Technology moves fast, and HP just got left behind. I'd rather invest in companies on the right side of the battlefield -- the ones looking forward.

Travis' take

At this point, a bet for or against HP is a bet for or against its survival. Like Sean said, the company has missed the boat on the cloud and is now stuck with older, low-margin businesses like PCs and printers that won't get many investors excited. But the stock is trading at just more than book value (although much of that is goodwill), the company is still profitable with a trailing P/E of less than nine, and none of its businesses, vanilla as they are, will dry up completely anytime soon.

I'll actually make the argument that the right activist investor could do a lot to unlock value in HP's business, and maybe rebranding would spice things up. If Carl Icahn were more of a techie, I could see this being right up his alley. The company has four large businesses and two small ones that don't necessarily make sense together in today's environment. Two businesses focused on consumers and businesses separately would make more sense to me.

A company with $124 billion in sales doesn't just dry up overnight, and even if Whitman has to throw a few new ideas at the wall, there isn't much to lose at this point. She has the engineering personnel to turn the company around and the foundation of a tech giant, and there's nowhere to go but up from a PR standpoint.

With all of that said, buying HP now is like trying to catch a falling knife. It could go exactly as planned: You ride the stock higher and cash out a nice profit as the company recovers from its embarrassing lows. But if it doesn't go well, you'd better have a crash cart handy, because there's no limit to the downside in companies with dying businesses.

I don't think HP is dead yet, but it needs a shot of adrenaline, and I'm not sure where that's going to come from with 27,000 workers soon to pack their bags. I'd rather sit on the sidelines here and buy in after a turnaround is well underway.

The call

We have a consensus -- that is, we've collectively decided to remain undecided about Hewlett-Packard's future. The concerns raised by Travis, Alex, and me point to one primary concern that will keep HP out of most investors' portfolios: a lack of innovation. IBM, Cisco, Amazon, and Apple all stepped out of their comfort zones and moved their products into the next generation, while HP has been left holding the buggy whip. It's legacy PC and printing business won't be going away anytime soon, so there's still intrinsic value there, but until HP gets with the times, we feel it's not worthy of your hard-earned money.

Although we've chosen not to enter a CAPScall today, you can reference our previous selections at the TMFYoungGuns CAPS portfolio.

Even if Hewlett-Packard isn't the stock for you, you're bound to find three great ideas by clicking here and discovering which three stocks could lead the new industrial revolution, according to our analysts on the Stock Advisor team.

At the time thisarticle was published Fool contributor Travis Hoium is currently short shares of Amazon.com and manages an account that owns Apple. Fool contributors Sean Williams and Alex Planes have no positions in any companies mentioned. You can follow Sean at @TMFUltraLong, Alex at @TMFBiggles, and Travis on Twitter at @FlushDrawFool.The Motley Fool owns shares of IBM, Cisco Systems, Amazon.com, and Apple. Motley Fool newsletter services have recommended buying shares of Amazon.com, eBay, and Apple, as well as creating a bull call spread position in Apple. The Motley Fool has a disclosure policy. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.