Gold: It's Just a Metal, Folks

Despite its recent pullback, gold's bull run, which began more than a decade ago, has rewarded those who owned it through the financial crisis. For investors willing to put up with intermittent declines -- some of them substantial -- gold has lived up to its billing as a "safe haven" asset. Will it continue to live up to that reputation? Perhaps not, as recent evidence suggests that it has been relegated to the ranks of its grubby commodity peers. If you own gold on the expectation that it is an effective hedge for the rest of your portfolio, now is the time to re-evaluate that premise.

Safe haven or risk asset?

Over the past eight months, as I monitored the financial markets in the backdrop of the eurozone crisis, I've been repeatedly puzzled by gold's behavior. As Mr. Market was once again subject to schizophrenic "risk on/risk off" moods, gold was consistently putting up losses on "risk off" days -- contrary to expectations. In fishing around for explanations, I must tip my hat to the Financial Times' James Mckintosh for providing one possible interpretation of this phenomenon.

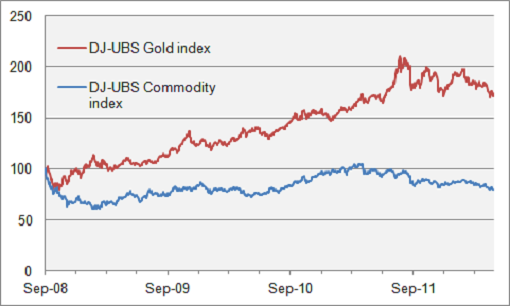

Let's compare gold's performance to that of the Dow Jones-UBS Commodity Index, which, as the name suggests, is a broad-based commodity price index. The first chart below begins with the fourth quarter of 2008, during which the financial crisis hit the world full-on (Lehman Brothers failed in October). Both indexes have been rebased to 100 at the beginning of the period.

Source: Dow Jones Indexes.

As we compare the two graphs during this period, we can see no clear relationship between gold and the broader group of commodities. As fear of financial and economic collapse increased, and as authorities across major developed economies responded with huge dollops of fiscal and monetary stimulus, investors began to treat gold as a currency no government can debase, rather than as a precious metal with limited industrial applications. It benefited accordingly, appreciating strongly; meanwhile, there is no corresponding trend for commodities, which look stuck within a range.

Putting things in focus

Now, let's focus on the end of that period. Here is the same graph for the year to date. I've again rebased the two indexes to start at 100 at the beginning of the period.

Source: Dow Jones Indexes.

Over this timeframe, the two graphs are a lot more tightly aligned. The chart suggests that gold price movements are now consistent with those of a broader set of commodities. By extension, the same factors are driving returns, including expectations for global -- and particularly Chinese -- GDP growth. Meanwhile, the notion of gold as a safe haven appears to have lost its appeal with investors.

Gold is no longer an effective hedge

This is consistent with my own observations that gold is no longer functioning as an effective hedge in the face of market upheaval. For example, the metal achieved its all-time high in early September last year -- well before the European crisis hit its (most recent) nadir in the fourth quarter. Since then, I have seen gold retreat with other risk assets on "risk off" days, giving the lie to its safe-haven status.

If gold were still trading as an alternative, "hard" currency, we should expect prices to be at or near fresh highs right now, given the level of fear related to the eurozone crisis. Indeed, if we look at other perceived safe-haven assets -- whether they be the Swiss Franc, German Bunds, Japanese government bonds, U.K. gilts, or U.S. Treasuries -- all are at or near historic levels. The SPDR Gold Shares ETF (NYS: GLD) , meanwhile, has declined by nearly a fifth since its Sept. 6 intraday high.

Not a currency, just a metal (albeit a precious one)

Last month and at the end of 2011, it was reported that the gold chart was in the throes of a "death cross" (which certainly sounds unpleasant), with the 20-day moving average moving below the 200-day average. I don't normally put much stock in technical analysis, but many people who trade gold do (there are no fundamentals to go on, after all). I'm told a death cross is a bad omen. Perhaps it is utter nonsense, but it can't help sentiment. Either way, investors who own gold should be aware that it is now trading like a metal, rather than as a safe-haven currency. If exposure to the commodities sector is what you're after, you'll want to look at this free Motley Fool report: "The Only Energy Stock You'll Ever Need."

At the time thisarticle was published Fool contributorAlex Dumortierholds no position in any company mentioned.Click hereto see his holdings and a short bio. You can follow himon Twitter. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.