Media Rebuttal: Enough About the Death of Equities

BusinessWeek published a story titled the "Death of Equities" in the late 1970s, arguing that "for better or for worse ... the U.S. economy probably has to regard the death of equities as a near-permanent condition."

That didn't happen -- stocks boomed soon afterward -- and ever since the article has become an illustration for how wrong the masses are at turning points in the market.

You'd think journalists would learn their lesson. But now they're at it again.

First came an article last week in Financial Times. It even used the same headline: "The Death of Equities." TheNew York Times also ran a piece, "End of the Affair?" which declared: "Investors are shunning the stock market, and who can blame them?"

Both arguments are specious, and I'd like to take a crack at some of the claims.

Here's the Financial Times (FT from here on out):

Allianz, with a total of about 1.7 trillion euros ($2.1 trillion) under management, has only 6 percent of its insurance portfolio in equities, while 90 percent is in bonds. A decade ago, 20 percent was in equities. It is far from alone: institutional investors, from pension funds to mutual funds sold directly to the public, have slashed holdings in the past decade.

OK, Allianz is one company -- anecdote alert! And yes, pension funds have indeed cut stock allocation from a decade ago, but come on... a decade ago was near the height of the dot-com bubble; it's not exactly a reasonable benchmark. U.S. pension funds recently held about 50% of their assets in stocks, down from more than 60% in 2000. But according to a paper by the Political Economy Research Institute, the average stock allocation was 30% to 40% in the 1980s, and as low as 1.5% in the 1950s. By any broad historical measure, pension funds' current allocation to stocks is generous.

Next up, FT:

The consequences are already being felt. Even the mighty Facebook is finding it hard to raise equity capital. With equity financing expensive, many companies are opting to raise debt instead, or to retire equity.

Wait, what?! Facebook's (NAS: FB) IPO was one of the largest in history, and commanded a valuation of 100 times earnings and 25 times revenue. The offering was oversubscribed 25 times over in Asia alone, and the company increased the size of the offering by 96 million shares at the last second because demand was so high. Facebook found raising equity "hard" in the same way that winning an Olympic medal leaves you "unaccomplished."

FT, round three:

Further, with equity returns virtually flat for more than a decade ...

Stop! I assume that calculation excludes dividends. The Dow Jones (INDEX: ^DJI) peaked in 2000 at 11,500. With dividends, it's now 49.4% higher. Up nearly 50% is not synonymous with "virtually flat."

Continue, FT:

Retail investors' conservatism has also driven money out of collective investment funds. In the U.S., inflows to bond funds have exceeded equity inflows every year since 2007, with outright net redemptions from equity funds in each of the past five years.

True, there's been outflow from equity mutual funds over the past five years (though it's small; roughly 3% of the total). But what about exchange-traded funds? Assets there have more than tripled since 2005 -- consistent with stories of investors cashing out high-fee mutual funds in favor of low-cost ETFs. Or how about individual stocks? According to Federal Reserve data, household ownership of corporate equities was higher in October 2011 (when the market was below current levels) than it was in 2005. Adjusted for inflation, household ownership of stocks and mutual funds combined was higher in 2011 that it was in 1998. And according to Gallup polls, the percentage of Americans who own at least some stocks has remained statistically unchanged over the last 14 years.

What else you got, FT?

"Overall, the past 10 years have been horrid. The question is why equity markets have not been down more," says Mr. Utermann.

Hold up. With dividends, the Dow is up 59.6% over the last 10 years, or an average annual return of about 5%. Considering we endured two wars, a collapse of the financial system, and the worst recession since the 1930s, that return is amazing. And more importantly, the reason returns were relatively low over the last 10 or 12 years is because returns from 1996-2000 were stupendously good -- returns that should have been spread out over 15 years were basically compressed into three. Stocks have returned almost exactly the historic average return since 1995.

Now, moving on to TheNew York Times:

Investors haven't just hunkered down, they have headed for the exits. Since the start of 2008, domestic stock mutual funds, a common way for individuals to invest, were drained of more than $400 billion, compared with an inflow of $52 billion in the four years before that.

Again, why the fixation with mutual funds? That's a dying product, folks. Looking at mutual fund activity and concluding that we're investing less is like looking at cassette tape sales and concluding that we listen to less music. Including all investment vehicles, households own more stocks today than they did during most of the dot-com bubble, adjusted for inflation. Isn't that a more meaningful number?

Round two, NYT:

[T]rading in the United States stock market has not only failed to recover since the 2008 financial crash, it has continued to fall. In April, average daily trades stood at 6.5 billion, about half their peak four years ago.

It's silly to use 2008 as some sort of benchmark. The market utterly crashed then, with some of the highest volatility in history. Of course volume is below that period. This is like pointing out that water levels in New Orleans are now below where they were the day after Hurricane Katrina.

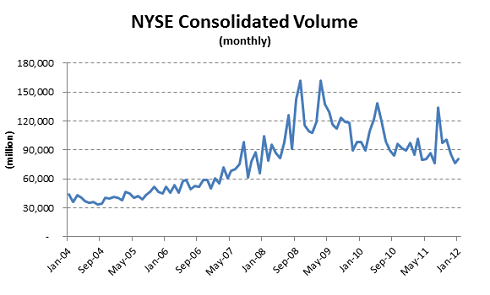

Look a little broader, and current market volume is substantially above where it was before the financial crisis:

Source: New York Stock Exchange.

I'd frankly enjoy if investors gave up on stocks in droves -- that's exactly when you want to start investing. But, sorry to say, they're not.

For a few great stock ideas our analysts are currently bullish on, check out The Motley Fool's free report: "The Future Is Made in America." It's free. Just click here.

At the time thisarticle was published Fool contributor Morgan Housel doesn't own shares in any of the companies mentioned in this article. Follow him on Twitter @TMFHousel. The Motley Fool owns shares of Facebook. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.