How Low Can Cabot Microelectronics Go?

Shares of Cabot Microelectronics (NAS: CCMP) hit a 52-week low on Friday. Let's take a look at how it got there and whether cloudy skies are still in the forecast.

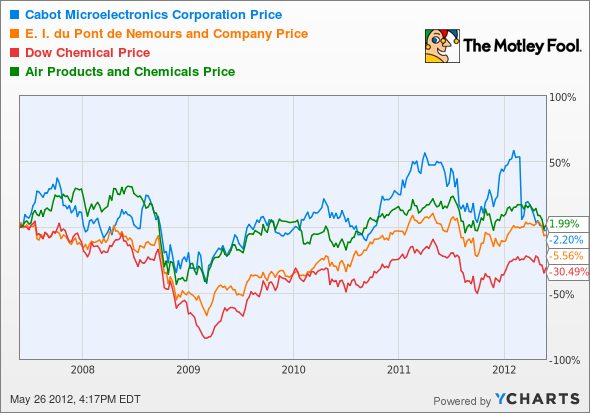

How it got here

If you're looking at a one-year chart on Cabot Microelectronics, the world's largest supplier of chemical-mechanical planarization polishing slurries to the semiconductor industry, you're probably wondering just what the heck happened on March 2?

The answer to this question relates to the company's announcement in mid-December that it was pioneering a new capital management initiative that would return money to shareholders. The company funded a $347 million, $15 per share special dividend that was funded 50-50 by cash on hand and a new revolving credit facility. I know what you're thinking and yes, it's extremely odd that management would fund a dividend with debt and that could be part of the reason why Cabot has been moderately weak of late.

Also to note was Cabot Microelectronics' 9.5% decline in revenue in its most recent quarter. A mixture of seasonal weakness, coupled with weaker demand in the semiconductor industry and a $3.7 million bad debt write-off related to the Elpida bankruptcy were a drag on margins year over year.

Still, Cabot remains bullish about the second half of the year and anticipates seeing strong semiconductor demand with fabless semi utilization rates improving and inventory levels returning to normal. Cabot could indeed have a case with contracted fabless chip makers Taiwan Semiconductor Manufacturing (NYS: TSM) and United Microelectronics (NYS: UMC) reporting a 10.4% and 11.4% increase in year-over-year April revenue, respectively.

How it stacks up

Let's see how Cabot Microelectronics stacks up next to its peers.

The past five years haven't been particularly kind to any CMP players, with Dow Chemical (NYS: DOW) being hit particularly hard among this group.

Company | Price/Book | Price/Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

Cabot Microelectronics | 3.0 | 8.7 | 12.1 | 6.8% |

DuPont (NYS: DD) | 4.6 | 9.5 | 10.0 | 6.0% |

Dow Chemical | 2.0 | 9.0 | 9.3 | 4.1% |

Air Products & Chemicals | 2.7 | 9.1 | 12.5 | 2.6% |

Source: Morningstar, author's calculations, CAGR = compound annual growth rate.

Although these companies are all trading within a stone's throw of one another based on these metrics, the comparison above is like trying to compare a grape to a watermelon.

Cabot is almost a pure play on CMPs and polishing pads for the semiconductor industry whereas DuPont and Dow Chemical manufacture CMP polishing slurries in addition to many, many other products, compounds, and synthetics. In terms of revenue alone, Dow Chemical totaled just shy of $60 billion last year to Cabot's mere $445 million. Steady cash flow created by significantly operational diversity is just one reason that both DuPont and Dow are able to pay out such robust dividends while Cabot doesn't offer a regular dividend.

That doesn't, however, mean Cabot should be ignored as it does boast the quickest five-year growth rate (as a smaller company usually will), and trades at a very marginal discount to cash flow than its CMP manufacturing peers.

What's next

Now for the real question: What's next for Cabot Microelectronics? That question is going to depend on whether the currently insatiable demand for smartphones, tablets, and laptops continues. As long as fabless semi manufacturers remain busy and inventories don't back up too much, Cabot should be in good shape.

Our very own CAPS community gives the company a three-star rating (out of five), with 44 out of 49 members rating it as an outperform. Although I have yet to make a CAPScall in either direction on Cabot, I am going to enter a limit order into the system to make Cabot an outperform call at $27.

"Why hesitate and not make it an outperform call now?" you may wonder. I'm a bit concerned about both the company's decision to take on $166 million in debt to fund a special dividend and the effects of excess inventory on sales over the next one to two quarters. I feel Cabot will make a very good hold over the long run because smartphones and tablets are getting cheaper. As these products get cheaper, more units will be sold and demand for CMP slurry and polishing pad products for refinishing wafers should rise, ultimately helping Cabot. At $27, I feel the reward finally begins outpacing the risk.

Just as I'm scouring around for the next great tech stock, our team of analysts at Stock Advisor has identified three stocks to own for the next Industrial Revolution. Find out their names for free by clicking here to get your copy of our latest special report.

Craving more input on Cabot Microelectronics? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.