How High Can Foot Locker Fly?

Shares of Foot Locker (NYS: FL) hit a 52-week high on Friday. Let's look at how the company got here and whether clear skies are ahead.

How it got here

The last year has been a good one for sporting goods retailers. The slow but steady economic recovery has put more money in the pockets of consumers and they're updating tattered sneakers with newer models just in time for summer.

The latest driver for Foot Locker was a strong performance in the first quarter of 2012. Sales rose 8.7% to $1.6 billion, and net income was $128 million, or $0.83 per share. But what was most impressive was a 9.7% increase in comparable same-store sales. This is one of the best indicators of health at retailers, and a close to double-digit growth rate is very impressive.

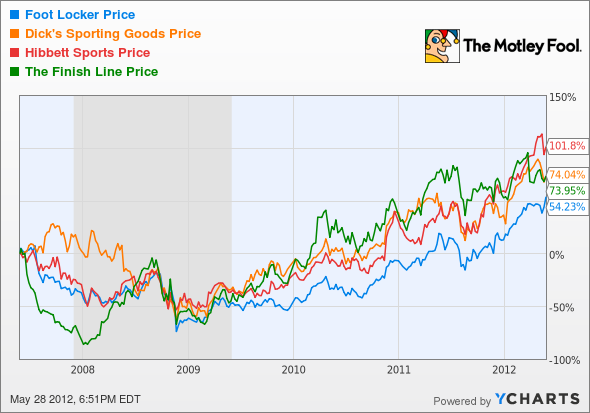

As well as Foot Locker has done, it is still underperforming some of its major competitors over the last five years on the stock market. Dick's Sporting Goods (NYS: DKS) , Finish Line (NAS: FINL) , and Hibbett Sports (NAS: HIBB) have all performed better as consumers have trended toward larger store formats.

But this underperformance means Foot Locker is now trading at lower valuation levels than competitors. On nearly every metric below, Foot Locker is still cheaper than the comparison companies, meaning there's still upside for shares.

Foot Locker | 0.9 | 2.3 | 9.7% | 12.5 |

Dick's Sporting Goods | 1.1 | 3.6 | 9.9% | 16.4 |

Finish Line | 0.8 | 2.1 | 12.4% | 11.8 |

Hibbett Sports | 2.0 | 6.7 | 19.4% | 19.0 |

Source: Yahoo! Finance.

The question is: Is Foot Locker's small store concept trending out or just maintaining its space in the market and becoming a value trap for investors? Competitors have been growing even faster than Foot Locker as athletes get used to one-stop shopping. For now, I think Foot Locker is maintaining its spot, but the model is becoming dated, and I wouldn't pay up for the shares.

What's next?

Despite strong comps, I wouldn't look at Foot Locker as a growth stock in the athletic retail space. The small mall store model just isn't going to explode when customers are trending toward larger stores like Dick's. But we can't overlook the company's 12.5 forward P/E ratio, low price to book and sales, as well as the 2.2% dividend. I think the stock can continue to rise although I would rather be in an athletics maker like Nike (NYS: NKE) , which has diverse retail channels, than betting on retail itself right now.

The CAPS community agrees with my tepid stance, giving the stock a two-star rating (out of five). If you're dying to buy a retailer, you could do worse than Foot Locker -- I just see better buys out there right now.

Interested in reading more about Foot Locker? Click here to add it to My Watchlist, which will find all of our Foolish analysis on this stock.

At the time thisarticle was published Fool contributor Travis Hoium owns lots of Nike shoes but does not have a position in any company mentioned. You can follow Travis on Twitter at @FlushDrawFool, check out his personal stock holdings or follow his CAPS picks at TMFFlushDraw.The Motley Fool owns shares of Dick's Sporting Goods. Motley Fool newsletter services have recommended buying shares of Nike. Motley Fool newsletter services have recommended creating a diagonal call position in Nike. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.