US Airways Soars to a New High: Is It Still a Buy?

Shares of US Airways (NYS: LCC) hit a 52-week high on Thursday. Let's take a look at how it got there and see if clear skies are still in the forecast.

How it got here

US Airways and the entire airline sector are roaring higher as a wave of price target and earnings estimate upgrades have come rolling in just this week from JPMorgan Chase, Dahlman Rose, and Bank of America Merrill Lynch. Primarily, there were three reasons for the upgrade and the bounce in US Airways' stock.

First, jet fuel prices have fallen by $0.40 since February, which should translate into $5.5 billion worth of savings for the entire industry. While this is good news for most airlines that hedge, this is fantastic news for US Airways, which doesn't hedge its fuel costs at all and is the most susceptible to prices rising. Secondly, earnings estimates for the airline sector haven't budged despite the drop in fuel costs and the relatively bullish airline traffic figures we've witnessed over the past couple of months. Finally, US Airways is one of the many airlines raking in huge margins from baggage fees. In all of 2011, according to data collected by the Bureau of Transportation, US Airways ranked third among all airlines (behind only Delta Air Lines (NYS: DAL) and American Airlines) having collected $506 million of the $3.36 billion airlines received in baggage fees.

Still, challenges remain including highly volatile fuel prices and the resurgence of regional carriers like Allegiant Travel (NAS: ALGT) and Spirit Airlines (NAS: SAVE) , which have more flexibility with their route coverage and are more reliant on optional fees and low-teaser rates to drive profits.

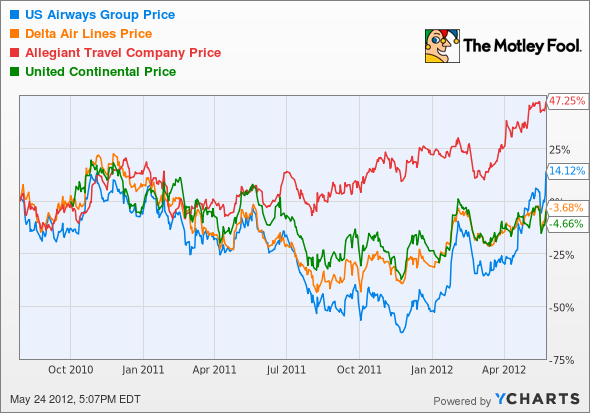

How it stacks up

Let's see how US Airways stacks up next to its peers.

Don't let this chart above fool you. If not for the United Continental Holdings (NYS: UAL) merger two years ago, Allegiant would be shown up 100% over the past five years, with US Airways and Delta down 65% and 40%, respectively.

Company | Price / Book | Price / Cash Flow | Forward P/E | Debt / Equity |

|---|---|---|---|---|

US Airways | 9.5 | 3.7 | 4.2 | 2,219% |

Delta Air Lines | N/M | 3.3 | 4.2 | N/M |

Allegiant Travel | 3.3 | 9.2 | 13.3 | 38% |

United Continental | 5.1 | 5.8 | 4.1 | 824% |

Source: Morningstar, Yahoo! Finance, N/M = not meaningful.

Yes, the airline sector looks incredibly cheap based on forward earnings multiples -- but make no mistake about it, this is the same sector that has witnessed more than 100 bankruptcies since 1990.

The biggest difference I've noticed is the bifurcation between regional and national carriers I alluded to earlier. National carriers with larger fleets are being forced to spend untold billions upgrading to newer planes to save on fuel costs in order to be competitive with regional airlines and their smaller, more agile routes and pricing policies. It's very easy for Allegiant to shut a route down if it becomes unprofitable, but if US Airways tried the same thing, passengers would be lined up with pitchforks outside its corporate headquarters.

That big difference can be seen in the huge debt loads carried by the national airlines. Delta Air Lines actually has so much debt it would wipe out all of the equity in the company if it were liquidated. US Airways, despite two bankruptcies in the past decade, still boasts a large amount of debt relative to shareholder equity, and even United Continental, which was expected to see huge synergies from its merger, is carrying an excessive amount of debt.

What's next

Now for the real question: What's next for US Airways. That question is going to depend on whether jet fuel prices remain low, which is imperative for US Airways to gain earnings momentum, and if it can lure potential customers away from lower-priced regional airlines and onto its planes. Right now, it seems that price is winning over loyalty no matter how hard the more mature airline brand names try.

Our very own CAPS community gives the company a dreaded one-star rating (out of five), with 42.4% of members expecting it to underperform. Although I've yet to make a CAPScall on US Airways, I'm ready now to anoint it with a rating of underperform. Here's why...

Plain and simple, this is a sector that would be better served by getting smaller, yet all US Airways wants to do is merge with an even larger national carrier. If it does indeed wind up merging with American Airlines, it's my opinion that the result would be the worst airline ever created from a financial standpoint. US Airways has turned to bankruptcy twice in the past decade, and I doubt it will survive another decade without seeking assistance again. As much as I loathe fuel hedges, I don't see how US Airways is going to compete without hedging with oil regularly priced around $100 per barrel. To me, this seems like a no-brainer underperform over the long haul.

US Airways may not be the stock for you; if you'd like the inside scoop on three companies that could help you retire rich, then click here for access to our latest free special report that's bound to make you jump for joy.

Craving more input on US Airways? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.