How Low Will Molycorp Go?

Shares of Molycorp (NYS: MCP) hit a 52-week low yesterday. Let's look at how it got here and whether more clouds are ahead.

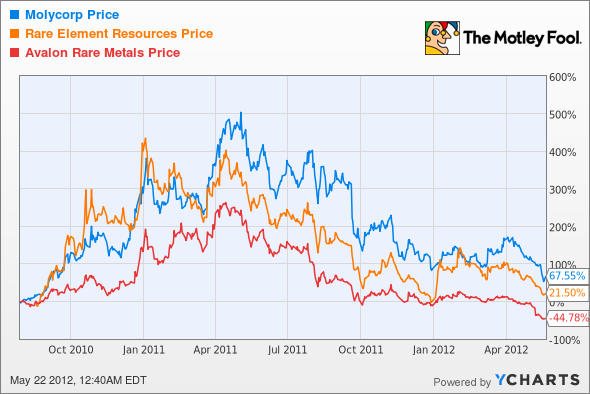

How it got here

Shares of Molycorp have fallen dramatically over the past year in the lead-up to the company ramping up to full production. Falling rare-earth prices have been the driver of the fall as investors become uncertain where prices will go when Molycorp and Lynas reach full production on two massive rare-earth-mineral mines.

Molycorp has tried to ease some of the worry by buying downstream companies, but it has come at a large cost. The latest deal to buy Neo Material Technologieswill cost $1.3 billion in cash and stock, and the cash needed for the deal didn't come cheap. Recently issued senior secured notes commanded a 10% yield, indicating that investors see Molycorp as a very risky bet.

The fall in rare-earth-mineral companies hasn't been limited to Molycorp. Avalon Rare Metals (NYS: AVL) and Rare Element Resources (NYS: REE) have crashed over the last year as well and have underperformed Molycorp since its IPO. These companies' long-term prospects are starting to look dim in the face of falling prices.

Here is a table of important prices in the most recent quarter, prices that have continued to fall since the end of the first quarter. As you can see, momentum isn't on Molycorp's side.

Didymium Products | $159 | $197 | $98 |

Lanthanum Products | $49 | $59 | $23 |

Cerium Products | $38 | $63 | $66 |

Subtotal REO Equivalent | $95 | $124 | $38 |

Source: Company press releases.

There's simply a lot of uncertainty surrounding the company's future, just at the time when revenue should begin shooting through the roof.

What's next?

A bet on Molycorp is really a bet on rare-earth prices, and I'm not prepared to bet that they won't continue to fall. The company's sole mine is enough to supply the U.S.' entire rare-earth-mineral needs, and when combined with Lynas, the two companies will flood the market with their respective products.

This isn't to say that Molycorp couldn't be profitable. Management thinks they can produce minerals for an average cost of $2.77 per kilogram, and if that's the case, there will definitely be a profit. I'm just not going to bet on how large those profits will be until the industry reaches some sort of steady state.

CAPS members are skeptical as well, giving the company a two-star ranking. On CAPS, 122 players have made an underperform call compared to 366 players thinking the stock will outperform the market.

If you want to speculate on rare-earth minerals, this is the best bet. It's just too risky for me until I see where prices are going to go in the next six to 12 months.

Interested in reading more about Molycorp? Click here to add it to My Watchlist, and My Watchlist will find all of our Foolish analysis on this stock.

At the time thisarticle was published Fool contributorTravis Hoiumdoes not have a position in any company mentioned. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.