1 Huge Reason to Buy Procter & Gamble's Stock

The importance of global diversification cannot be overstated. Not only does it expose investors to the blistering speed of the developing world's economic growth, but it also insulates stock returns from regional economic downturns like the Great Recession. Without a doubt, it is one of the principal keys to successful investing in modern times.

The safest and easiest way to do it is by investing in American companies with significant operations abroad. Of particular interest on that front is Procter & Gamble (NYS: PG) , the one stock I've previously recommended to new investors.

The promise and perils of investing abroad

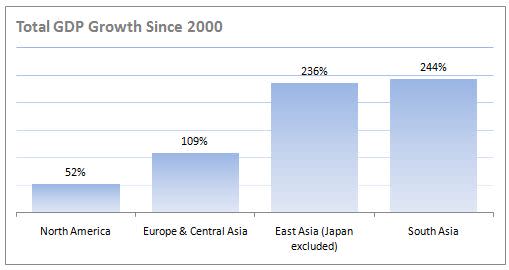

The most obvious reason to diversify globally is to gain exposure to the developing world's economic growth. Over the past decade, emerging markets have expanded much more quickly than the developed world has. South Asian economies, led by India, have more than tripled their output since 2000. And if you take Japan out of the equation, the East Asian economies have done the same, going from $3.3 trillion in 2000 to $11.2 trillion in 2010. In fact, North America is the only continent that hasn't at least doubled its economic output since the turn of the century.

Source: World Bank.

Global diversification also acts as a hedge against regional economic downturns, a benefit that revealed its advantage in 2009. Triggered by the financial crisis, output in North America and Europe shrank that year by 3.4% and 4.3%, respectively. Yet South Asian economies simultaneously grew 8.1%. And while output in the entire East Asian and Pacific region contracted by approximately 1%, weighed down by Japan's 6.3% decline, the region's largest economy in China grew a staggering 9.2%.

These two benefits aside, however, it's important to remember that investing directly in international markets is risky. Just recently, for example, a wave of fraud has washed over Chinese small-cap stocks, costing investors billions of dollars. A typical example is Chinese Internet security software maker Qihoo 360, which saw its shares lose more than 20% of their value by the middle of last month because of questionable accounting practices -- though they have subsequently recovered. Even the most sophisticated of investors were caught in the undertow, as famed hedge-fund manager John Paulson purportedly lost more than $100 million when Chinese forestry company Sino-Forest was revealed to be a fraud.

The best of both worlds

The best way to balance the benefits of global diversification without exposing your portfolio to undue risk, in turn, is to invest in American companies with global exposure. Two that come to mind are Coca-Cola, the Warren Buffett favorite and soft-drink manufacturer that gets nearly half of its net revenues abroad, and Wal-Mart (NYS: WMT) , the global retail giant that looks outside of North America for a third of its sales. Undoubtedly one of the best in this regard is Procter & Gamble, the consumer-products giant.

What we now know as P&G came about in 1837, when William Procter, a candle maker, and James Gamble, a soap maker, were persuaded to become business partners by their father-in-law, whom they shared as a consequence of marrying sisters. The rest is history. Today, the company records more than $80 billion in annual sales and controls some of the best-known brands in the world, including Crest toothpaste, Gillette razors, Pampers diapers, and Duracell batteries, among many others. All told, the company's world-renowned portfolio includes 78 brands, 26 of which generate more than $1 billion in sales each.

Source: Procter & Gamble's Investor Relations.

It should accordingly be no surprise that P&G has an extensive presence around the globe. Its brands are sold in more than 180 countries, just shy of the 193 that are members of the United Nations. And almost 60% of the company's 2011 net sales came from outside North America, with its largest international region being Western Europe at 20% of net sales, followed closely behind by Asia at 16%. In addition, roughly one-third of the company's net sales derived from the developing world.

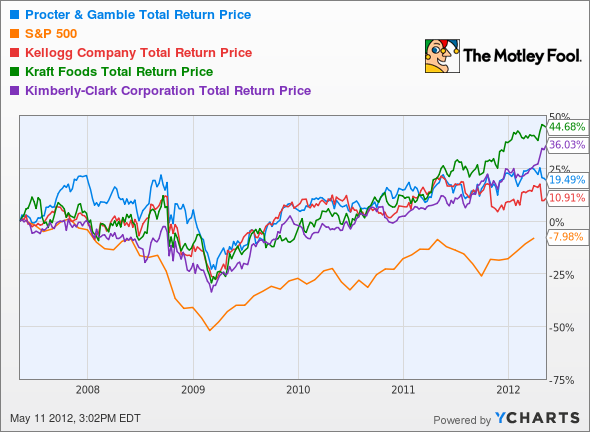

It's this diversification that's contributed to both the company's growth and the fantastic performance of its stock price. Despite the Great Recession in the developed world, since 2007, its total revenues have grown by 8%, from $76.5 billion to $82.6 billion last year. And not surprisingly, its stock price has responded in kind. Over the past five years, an investment in P&G has outpaced the broad market as well.

It's nevertheless true that many of P&G's competitors have fared as well, if not better, over the same time period. The top performer in this space has been Kraft (NYS: KFT) , which returned a staggering 44%, followed by Kimberly-Clark (NYS: KMB) at 36%. The only peer to fare worse was Kellogg (NYS: K) , which came in at 11%. Yet all of these are significantly smaller companies, and thus presumably more vulnerable to financial and economic disruptions, with market capitalizations that are a fraction of P&G's. Indeed, the second largest, Kraft, is less than half P&G's size by this measure.

PG Total Return Price data by YCharts

Foolish bottom line

P&G's globally diversified operations should serve to both preserve and grow investment capital over the years to come -- not to mention that it pays a 3.5% dividend yield. And it's for these reasons that I reiterate my opinion that Procter & Gamble is a great stock for the long term.

For a handful of other companies like P&G, check out our recently released free report about three American companies set to dominate in emerging markets. Among others, it discloses the identify of a stock that's doubled in the last few years and still pays an atypically generous dividend yield. Access this report while it's still available -- and free.

At the time thisarticle was published Fool contributor John Maxfield has no financial interest in any of the companies mentioned above. The Motley Fool owns shares of Coca-Cola.Motley Fool newsletter serviceshave recommended buying shares of Procter & Gamble, Coca-Cola, and Kimberly-Clark and creating a diagonal call position in Wal-Mart Stores. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.