1 Huge Reason to Buy Coca-Cola's Stock

The importance of global diversification cannot be overstated. Not only does it expose investors to the blistering speed of the developing world's economic growth, but it also insulates stock returns from regional economic downturns like the Great Recession. Without a doubt, it is one of the principal keys to successful investing in modern times.

The safest and easiest way to do it is by investing in American companies with significant operations abroad. Of particular interest on that front is Coca-Cola (NYS: KO) , the world's largest soft-drink company and the ultimate rule maker.

The promise and perils of investing abroad

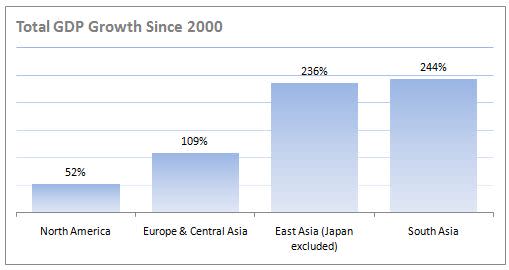

The most obvious reason to diversify globally is to gain exposure to the developing world's economic growth. Over the past decade, emerging markets have expanded much more quickly than the developed world has. South Asian economies, led by India, have more than tripled their output since 2000. And if you take Japan out of the equation, the East Asian economies have done the same, going from $3.3 trillion in 2000 to $11.2 trillion in 2010. In fact, North America is the only continent that hasn't at least doubled its economic output since the turn of the century.

Source: World Bank.

Global diversification also acts as a hedge against regional economic downturns, a benefit that revealed its advantage in 2009. Triggered by the financial crisis, output in North America and Europe shrank that year by 3.4% and 4.3%, respectively. Yet South Asian economies simultaneously grew 8.1%. And while output in the entire East Asian and Pacific region contracted by approximately 1%, weighed down by Japan's 6.3% decline, the region's largest economy in China grew a staggering 9.2%.

These two benefits aside, however, it's important to remember that investing directly in international markets is risky. Just recently, for example, a wave of fraud has washed over Chinese small-cap stocks, costing investors billions of dollars. A typical example is Chinese Internet security software maker Qihoo 360 (NAS: QIHU) , which saw its shares lose more than 20% of their value by the middle of last month because of questionable accounting practices -- though they have subsequently recovered. Even the most sophisticated of investors were caught in the undertow, as famed hedge-fund manager John Paulson purportedly lost more than $100 million when Chinese forestry company Sino-Forest was revealed to be a fraud.

The best of both worlds

The most effective way to balance the benefits of global diversification without exposing your portfolio to undue risk, in turn, is to invest in American companies with global exposure, like the three identified in our free report: "3 American Companies Set to Dominate the World." In addition to those, two that come to mind are Starbucks, the international coffee chain that's looking to triple its store count in China by 2015, and Wal-Mart, the global retail giant that looked abroad for a full 32% of its sales last year. Though undoubtedly one of the best in this regard is Coca-Cola, the undisputed sultan of soda.

The ubiquity of Coke's products renders most introductions unnecessary. Altogether, 1.7 billion servings of various Coke beverages are consumed each day -- if the beverages were evenly distributed, in other words, every person on the planet could have nearly two servings a week. A staggering 94% of the world's population recognizes its iconic red-and-white brand, worth an estimated $72 billion. And the company has even reported that its name is the second-most understood term in the world, behind "OK."

Source: Coca-Cola, Q1 2012 10-Q.

When it comes to international product distribution, Coke has few peers. Its beverages are sold in more than 200 countries, seven more than are members of the United Nations. While the majority of the company's revenues come from North America -- 52%, to be precise -- a full 48% come from abroad. Its largest international region is Asia, which brings in 15% of Coke's net revenues, followed by Europe, Latin America, and Eurasia/Africa, which account for 13%, 13%, and 7%, respectively. Its distribution channel is so wide, in fact, that multibillion-dollar companies like Coca-Cola Hellenic (NYS: CCH) , the company's primary bottler and distributor in more than 28 countries, are able to thrive exclusively by operating within its ecosystem.

This diversification, in turn, is largely responsible for the company's growth over the past few years. For example, despite the Western world's economic woes, since 2007, Coke's total annual revenues have grown a staggering 61%, from $28.8 billion to more than $46.5 billion last year. And for the first quarter of this year, the soft-drink manufacturer saw volume rise by only 1% in United States compared with increases of 9% in China and 20% in India.

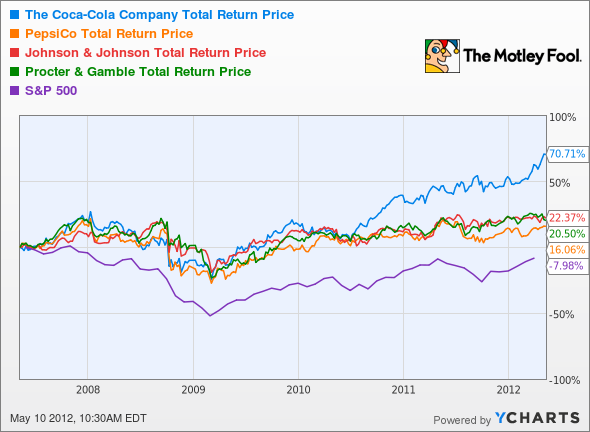

With this in mind, it's no surprise that Coca Cola's stock has responded in kind. Over the past five years, an investment in the soft-drink maker returned 71%, beating the broader market by a whopping 63 percentage points. And it similarly exceeded the otherwise respectable returns of its closest competitor, PepsiCo (NYS: PEP) , which notched a 16% total return over the same time period, and even the well-known consumer-staples companies Johnson & Johnson (NYS: JNJ) and Procter & Gamble (NYS: PG) , the latter of which I have recommended to beginning investors.

KO Total Return Price data by YCharts

Foolish bottom line

Coca-Cola is not a perfect stock, as it's far from cheap, trading for 20 times earnings. Yet its globally diversified operations should serve to both preserve and grow investment capital over the years to come. And it's for this reason, not to mention the fact that it pays a 2.6% dividend yield, that I believe Coca-Cola is a good stock for the long-term investor.

For a handful of other companies like Coca-Cola, check out our recently released free report about three American companies set to dominate in emerging markets. Among others, it discloses the identify of a stock that's doubled in the past few years and still pays an atypically generous dividend yield. Check out this report while it's still available -- it's free.

At the time thisarticle was published Fool contributor John Maxfield has no financial interest in any of the companies mentioned above. The Motley Fool owns shares of Coca-Cola, Johnson & Johnson, Starbucks, and PepsiCo.Motley Fool newsletter serviceshave recommended buying shares of Coca-Cola Hellenic Bottling, Coca-Cola, Johnson & Johnson, Procter & Gamble, Starbucks, and PepsiCo, writing covered calls in Starbucks, and creating diagonal call positions in PepsiCo, Wal-Mart, and Johnson & Johnson. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.