What Will Be Facebook's Next Big Moneymaker?

Facebook (NAS: FB) is free and always will be. It says it right there on the home page before you login. That value proposition has certainly helped the social-networking king garner a worldwide user base of 901 million monthly active users, or MAUs.

The company has now gone public, and public investors are going to want to see lots of dollars coming in to keep their interest. How is Facebook going to increase user monetization now that its user base has reached critical mass?

Stop me if you've heard this one before

Of course, Facebook has traditionally done this through advertising, which is why Google (NAS: GOOG) doesn't take so kindly to the increasing amount of time people spend on Facebook's site as opposed to its own. The bulk of revenue continues to be generated through traditional display ads, which is the oldest Internet business model since the dawn of -- well, since the dawn of the Internet.

In fact, chances are there are at least three ad banners on the page you're reading right now. Luckily, you've mastered the art of selectively tuning them out (I hope).

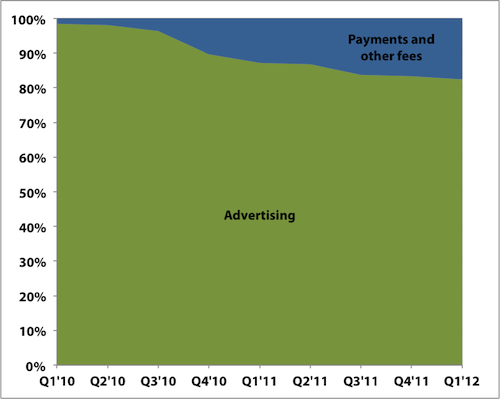

Facebook has been working to diversify its revenue base and grow its payments-and-other-fees segment, which has mostly worked well over the past few years. Two years ago, advertising was 98.5% of sales, and that figure has dropped to 82.4% last quarter.

Source: Facebook S-1 Registration Statement.

Source: Facebook S-1 Registration Statement.

Source: Facebook S-1 Registration Statement.

Payments are generated through Facebook's platform, which so far is mostly thanks to Zynga (NAS: ZNGA) . Facebook's S-1 registration statement makes it clear: "To date, games from Zynga have generated the majority of our payments and other fees revenue." This revenue stream is directly threatened by Zynga's own new platform that it launched a few months ago on Zynga.com.

For now, Zynga.com will continue to use Facebook Credits as the primary virtual currency, but this arrangement is pretty clearly just part of Zynga's longer-term plan to transition itself away from relying on Facebook. This way, players can continue using the Facebook Credits they're already familiar with and may have already paid for, but the seeds are now sown for an eventual move away from Facebook Credits that will hurt Facebook's top line.

Keep in mind that the pair has an agreement where Facebook keeps a 30% cut of Zynga user purchases made on Facebook's platform -- an agreement that expires in three years. It's a safe bet that Zynga wants to become a gatekeeper of its own for Zynga.com, eventually collecting a cut on sales made on its platform.

What's a social network to do?

So Facebook is now scratching its head, pondering how else it can monetize all those MAUs. Average revenue per user, or ARPU, has been trending higher, and it's going to need to branch out to keep that trend going, especially in light of the competitive threat from Zynga on the revenue stream it was just starting to enjoy.

Source: Facebook S-1 Registration Statement.

Source: Facebook S-1 Registration Statement.

Source: Facebook S-1 Registration Statement.

The company is now experimenting, much as Google is known for, with new methods of monetization and moat building.

Is there a social app for that?

Facebook has just introduced its new App Center, a social-app discovery service that's taking a direct shot at Apple's (NAS: AAPL) ability to help users find relevant apps among its swelling stable of 635,000 apps and counting. Apple recently acquired app-discovery startup Chomp for an estimated $50 million to beef up its app-discovery abilities, as its Genius feature has never been a show-stealer. Apps will be ranked based on user ratings, engagement, and other quality metrics to determine whether they make the cut.

Facebook's App Center isn't a new mobile-app storefront, since it will be built directly into Facebook's mobile app and users will still need to download mobile apps through Apple's App Store or Google Play. This move is really more about building a moat to keep users on Facebook's platform, as the App Center will be integrated with Facebook's desktop platform.

It's a subtle way to drive Facebookers from its mobile app, which it has difficulty monetizing, to its desktop platform, where it's improving monetization.

The price of importance

An even more interesting new feature that Facebook is testing is the ability to "Highlight" a particular post or status update, giving it priority in news feeds -- not entirely unlike Big G's sponsored ads in search results. Facebook recently disclosed that the average post reaches only 12% of a user's friends, in part because friends can change what types of updates they see.

Source: TechCrunch.

Source: TechCrunch.

Source: TechCrunch.

For a nominal fee, a user can make sure friends see a post that's been "Highlighted" as important. Part of the test for this feature includes a free "Highlight" to gauge interest, as well as the paid option shown above to see whether users are willing to pay for something like this. "Highlighted" posts may be given prominence in feeds, remain visible for longer periods of time, and show up for more friends.

It's a risky move, but it was spotted in New Zealand, a relatively safer test ground than the United States and Canada in case it backfires. Now, if this particular feature were to be warmly received (which is doubtful), it could do wonders for monetization and ARPU.

Worldwide ARPU was $1.21 last quarter. If you opt to pay $2 to "Highlight" a single post, you're contributing more revenue from that one post than Facebook generated from the average user throughout the entire quarter. Even the United States and Canada's highest ARPU of $2.86 could see meaningful upside if "Highlight" works out, although I have doubts on this one.

All eyes on Facebook

The public pressure is about to be turned on to keep growing sales, and Facebook is obviously well attuned to that fact. Testing new ways to monetize its user base is a requisite for its long-term success, especially from an investor's perspective.

While everyone is focusing on Facebook's IPO, there's another social-media company that recently had its own IPO and looks even more promising. Forget Facebook -- Here's the Tech IPO You Should Be Buying because this social butterfly has a much more reliable monetization model and isn't as vulnerable to the fickle budgets of advertisers. Do yourself a favor and grab a free copy of this report to find out more.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Apple, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Google and Apple.Motley Fool newsletter serviceshave recommended buying shares of Google and Apple and creating a bull call spread position in Apple. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.