Symantec Hits a 52-Week Low: Can It Protect Itself?

Shares of data-security specialist Symantec (NAS: SYMC) hit a 52-week low yesterday. Let's take a look at how the company got there to find out whether cloudy skies remain on the horizon.

How it got here

One major weight on Symantec's stock price of late was its weak late April earnings estimate for its most recent quarter, which undercut both its own guidance and Street expectations. The company met its own projections and satisfied analyst estimates when it made earnings results public, but that wasn't enough to reverse the slide. In fact, Symantec's revenues and free cash flow have been virtually flat for the past five years, with its most recent uptick in net income the only real bright spot in an otherwise lackluster half-decade.

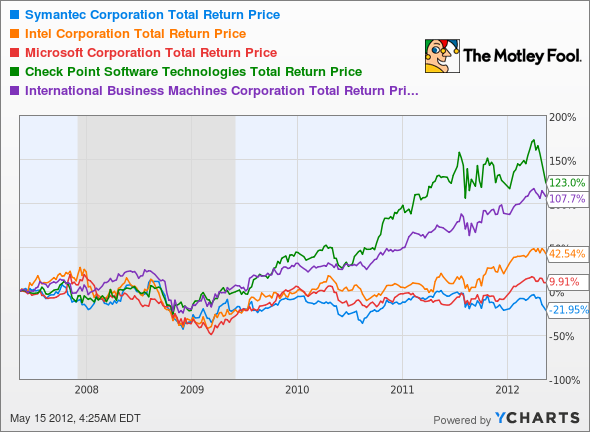

That middling performance has depressed the company's valuation, and it's now one of the cheapest tech stocks on the market. However, with no dividend to help it stand out in a sector that's increasingly moving toward quarterly shareholder rewards, investors may be left wondering whether the stock has become a value trap. Its five-year performance does nothing to dispel this fear:

SYMC Total Return Price data by YCharts.

What you need to know

Symantec's now the largest pure-play software security companies by revenue that's left standing after Intel's (NAS: INTC) 2010 McAfee acquisition, although Check Point Software (NAS: CHKP) boasts a roughly equivalent market cap. However, many of its competitors have at least resisted the decline that's dented Symantec shareholders' portfolios over the last half-decade.

Company | P/E Ratio | Annualized 3-Year Earnings Growth | Net Margin (TTM) |

|---|---|---|---|

Symantec | 9.7 | 13.9%* | 17.4% |

Intel | 11.4 | 42.0% | 23.2% |

Check Point Software | 19.9 | 16.5% | 44.2% |

Microsoft | 11.2 | 17.0% | 32% |

AVG (NYS: AVG) | 9.3 | 19.5% | 31.7% |

Fortinet (NAS: FTNT) | 61.0 | 1.6% | 13.8% |

Source: Yahoo! Finance. TTM = trailing 12 months. *Four-year calculation is used because of one-time goodwill impairment in 2009.

Smaller competitor Fortinet only went public at the tail end of 2009, which was a bit too short to adequately display on the chart above. Antivirus software maker AVG is a recent entrant to public markets but boasts a more attractive valuation than either young Fortinet or established Symantec, despite a better growth rate and net margin than both companies.

Check Point, which focuses on network security, has an enviable net margin that's clearly appealed to investors in spite of its lack of dividend and three-year trailing growth rate in line with dividend stalwarts Intel and Microsoft. Intel's annualized earnings growth is no fluke despite a decline in 2009 -- the company had averaged about $1.4 billion more in earnings the three years before the recessionary hit, but it has nearly tripled earnings since.

Symantec's competition is fierce from all angles, and many competitors have posted better growth over recent years. It's been slow moving into cloud security, which could be a long-term disadvantage as Intel's overwhelming chip dominance in the server space gives it an easy upsell for its McAfee security products.

What's next?

Where does Symantec go from here? That will depend on its ability to successfully move more users toward a recurring-revenue subscription model while simultaneously maintaining its position in a very crowded and competitive security space. The Motley Fool's CAPS community is a bit lukewarm on Symantec, giving it a three-star rating out of five. Though all but one tracked Wall Street analyst on CAPS expects outperformance, 16% of our All-Star players expect the stock to lag the market going forward.

Interested in tracking this stock as it continues on its path? Add Symantec to your watchlist now for all the news we Fools can find, delivered to your inbox as it happens. If you're looking for a surefire way to profit from the cloud, take a look at The Motley Fool's popular (and completely free) report on "The Only Stock You Need to Profit From the New Technology Revolution." Thousands have discovered the secret to success in the Big Data trends shaping cloud computing, and you can be next -- just click here to claim your free copy today.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool owns shares of Microsoft and Intel. Motley Fool newsletter services have recommended buying shares of Microsoft, Check Point Software Technologies, and Intel. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.