OPNET's Earnings May Present an Opportunity

When looking at earnings quality, we at The Motley Fool have two databases -- EQ Scan and EQ Score -- that help us uncover cash flow and revenue recognition issues. Smart financial officers can use several techniques to manipulate financial results, and manipulation of any of the three financial statements usually affects the other two. But a critical eye on these statements can often uncover trends that could be important to help investors protect against losing their hard-earned money.

The EQ Score database assigns an index rank to the company, from 1, for the lowest quality, to 5, for the highest. As the company's financial status changes over time, the database adjusts its rank and illuminates trends that will affect earnings quality going forward. The EQ Score ranks OPNET Technologies (NAS: OPNT) as a "3," equivalent to a "C" letter grade. Let's see why.

OPNET, an up-and-coming software company that provides application and network performance management solutions in the United States and internationally, will report earnings after the market closes tomorrow. Analysts expect it to report $44.79 million in revenue and $0.21 in earnings per share, which will be 5% better than last year's reported $0.20 for the same quarter. If the company meets its revenue target, it will be a 9% increase from last year's $41.1 million.

OPNET competes with several industry heavyweights, including IBM (NYS: IBM) and Citrix Systems (NAS: CTXS) , among others.

Company | Reporting Date | Revenue | EPS | EQ Score |

|---|---|---|---|---|

IBM | July 18 | $26.50 billion | $3.44 | 2 |

Citrix | July 23 | $613.79 million | $0.59 | 1 |

IBM scores a "2," and Citrix ranks as a "1."

Let's look at OPNET's income-statement metrics.

Metric | Quarter Ended 12/31/2011 | Quarter Ended 12/31/2010 | Quarter Ended 12/31/2009 |

|---|---|---|---|

Revenue (Millions) | $45.99 | $39.68 | $33.56 |

Revenue +/- % | 15.90% | 18.24% | NA |

Cost of Goods Sold | 21% | 20% | 23% |

Gross Margin | 79% | 80% | 77% |

Selling, General, and Administrative Costs | 39% | 43% | 42% |

Operating Margin | 18% | 14% | 10% |

Net Profit Margin | 12% | 11% | 7% |

Earnings Before Interest, Taxes, Depreciation, and Amortization | 22% | 18% | 14% |

Earnings Per Share | $0.23 | $0.19 | $0.11 |

Those numbers look promising. Revenue is increasing year over year, and the cost of sales is low, which results in a high gross margin. Selling and administrative costs are high, but decreasing. Operating margins are increasing, which is good news because it shows improved operational efficiency. As projects get larger, operating margins will continue to improve. Margins are moving upward in the right direction, and earnings per share have more than doubled in two years.

Now let's look at the metrics that affect cash flows.

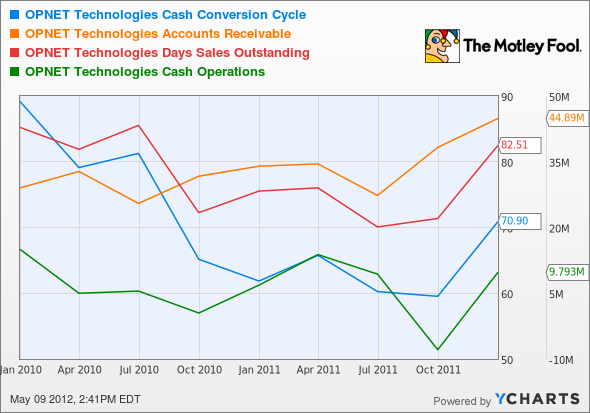

OPNT Cash Conversion Cycle data by YCharts

Receivables, operating cash, days sales outstanding, and the cash conversion cycle were all rising in the last quarter of 2011. Over the past two years, however, receivables have increased slightly while the other metrics have shown declining trends. Receivables hovered at an unfortunate 98% of revenue at year end. Deferred revenue is nicely high at $49.79 million, and this measure of backlogs has been increasing. That's good news. The takeaway here is that if OPNET could improve on collecting monies owed, more selective stock pickers would recognize this company as an opportunity waiting to be realized.

Competitor No. 1 -- IBM

IBM Shares Outstanding data by YCharts

When IBM is the adversary, some historic conflicts come to mind. Not unlike the biblical David who fought the giant Goliath, OPNET appears to be winning the battle against IBM. The latter's EQ Score is a higher "2" probably because this behemoth apparently is using debt to reduce its shares outstanding, thereby artificially inflating earnings. While revenue on average has increased 6% and operating margins have remained flat year over year, earnings per share popped 17% ($1.97 to $2.31) for the quarter ended March 31 -- and for the most recent quarter, earnings increased from $2.31 to $2.61, or 13%. Total debt to total capital stands at 61%, and IBM has $32.05 billion in long-term debt on its balance sheet. Also surprising is that IBM has a negative tangible book value of -$9.02 per share.

Competitor No. 2 -- Citrix Systems

Citrix's earnings quality is at "1" because the company hasn't properly managed its cost structure, and profit margins have suffered as a result. Revenue year over year is up 20%, and the company has an extremely low 9% cost of sales, but administrative costs stand at an unacceptable 52%. The company has been buying growth, through a 2011 acquisition for $455.4 million, and it's also buying earnings through share repurchases totaling $858.5 million over the past two years.

In the hierarchy of metrics affecting earnings quality, revenue is most important, and cash flow is more important than net income. In other words, Wall Street tends to focus on the wrong metric as the basis for its recommendations to buy, hold, or sell a stock. Since last November, OPNET's stock price has fallen from $47.74 to $22.92, or more than 52%. OPNET's trailing P/E is 28.75. Last year's earnings came in at $0.68, and analysts expect the company to earn $0.93 a share this year, a 36.76% increase. Based on this data, OPNET may be an opportunity to buy ahead of the upcoming earnings announcement, and shareholders will receive an annual dividend of $0.48, a yield of 2.10%. Prudent Fools should make investment decisions based on consideration of earnings quality.

One of the great things about companies like OPNET are the great dividends they pay, but there are even better ones out there. You can read about them in our special free report: "Secure Your Future With 9 Rock-Solid Dividend Stocks." See which dividends make the grade.

At the time thisarticle was published Fool contributorJohn Del Vecchiois the co-advisor of Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter, where he goes by @johnfdelvecchio. He owns no shares in the companies mentioned in this article. The Motley Fool owns shares of IBM and has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.