1 Great Dividend You Can Buy Right Now

Dividend stocks are everywhere, but many just downright stink. In some cases, the business model is in serious jeopardy, or the dividend itself isn't sustainable. In others, the dividend is so low it's not even worth the paper your dividend check is printed on. A solid dividend strikes the right balance of growth, value, and sustainability.

Today, and one day each week for the rest of the year, we're going to look at one dividend-paying company that you can put in your portfolio for the long term without too much concern. This isn't to say these stocks don't share the same macro risks that other companies have, but they are a step above your common grade of dividend stock. Here's last week's selection.

This week, I want to take a step back from our discussion last week of dividend aristocrats and again point out an up-and-coming dividend powerhouse in the technology sector: Applied Materials (NAS: AMAT) .

Cloud-y forecast with a chance of a solar storm

Lately, I've been reminding investors to get their heads out of the cloud. But in this instance, just as with Intel (NAS: INTC) , I'm encouraging investors to allow the cloud to drive their imagination as to Applied Materials' potential.

Applied Materials, a manufacturer of equipment used by semiconductor companies, has had a hard time keeping up with demand from consumers for smartphones and tablets. Taiwan Semiconductor (NYS: TSM) and United Microelectronics (NYS: UMC) are the two primary contracted fabless semiconductor producers for smartphones and tablets, and a steady stream of orders from those two have kept Applied Materials' business strong. Intel hasn't had as much of an effect, as it's a vertically integrated company capable of internalizing its entire production process.

Applied Materials' other struggling sectors also have me excited about its future prospects. What I figure is if its display and solar segments are performing this poorly now, and the company is still remarkably profitable, imagine how much of a value Applied Materials will be when its solar or display operations do rebound!

The company's solar segment isn't sitting on its laurels, either, while solar-panel prices crash and supply shoots through the roof. Applied Materials just announced the layoff of 250 workers and plans to move its environmental-solutions manufacturing facility, which makes the equipment that manufactures solar cells and light emitting diodes, to Asia from Switzerland. The company's nearly $5 billion purchase of Varian Semiconductor hasn't paid off yet, but I do see the purchase being a long-term winner for its solar segment.

The king of semiconductor equipment

Now let's get to the nitty-gritty of things -- that Applied Materials is the best buy in a crowded semiconductor equipment sector.

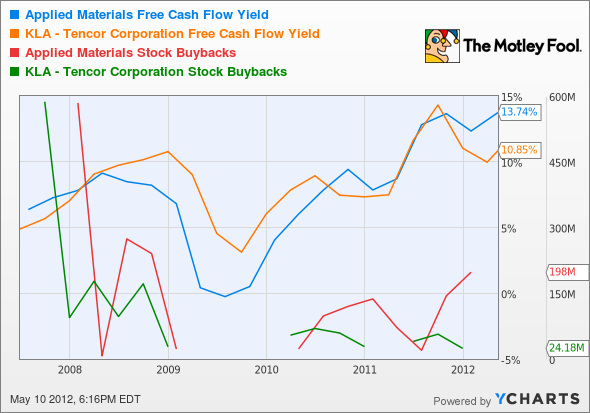

AMAT Free Cash Flow Yield data by YCharts

Although it may seem a little confusing, what I'm aiming to show is that based on free cash flow yield and share-repurchase activity, Applied Materials looks more attractive than KLA-Tencor (NAS: KLAC) right now. This isn't to put down KLA-Tencor's business one bit, because it has performed well and has surpassed Wall Street's estimates recently, just like Applied Materials.

The best news for shareholders wasn't that the company authorized an additional $3 billion share-repurchase program, but that it again boosted its dividend in March to $0.09 quarterly. This marked the fifth time the company has raised its dividend since it began paying out a $0.03 quarterly stipend in mid-2005.

Source: Dividata.

*Estimated annual dividend based on $0.09 quarterly payout for remainder of 2012.

With a new annual yield of 3.2% and $2 billion worth of cash on hand even after its Varian acquisition, Applied Materials is sitting in an advantageous position to expand its business further while also rewarding its shareholders. Its current payout ratio of just 26% is low enough that shareholders can expect future dividend increases (as long as the market cooperates) while its sub-10 forward P/E ratio signifies that investors are giving the company very little respect.

Foolish roundup

Income investors would be foolish to ignore the role Applied Materials will play in the cloud and the solar industry's future and would be wise to give this future dividend juggernaut a second look if they haven't already.

If you're craving even more dividend ideas, I invite you to download a copy of our latest special report, "Secure Your Future With 9 Rock-Solid Dividend Stocks," which is loaded with income-producing companies hand-selected by our top analysts. Best of all, the report is free, so don't miss out!

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any of the companies mentioned in this article. You can follow him on Motley Fool CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool owns shares of Intel.Motley Fool newsletter serviceshave recommended buying shares of Intel. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days. The Motley Fool has adisclosure policythat's simply fab-ulous.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.