3 Things You Need to Know About Annaly Capital's Big Earnings

Annaly Capital (NYS: NLY) reported adjusted earnings per share of $0.54 for the fourth quarter, in line with last quarter, but down from $0.70 a year ago.

Here's an update on Annaly's progress in three critical areas:

1. Profit spreads remain down

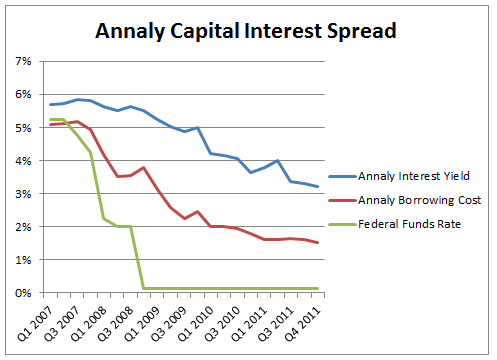

Low short-term interest rates have been a boon for residential mortgage REITs like Annaly. But falling long-term rates have crimped profits over the past year.

Although the Fed hasn't moved ahead with attempts to help out the economy by further lowering long-term interest rates, Operation Twist and QE 1 and 2 continue to hold down Annaly's portfolio yields.

Here's how Annaly's interest rate spread has fared lately:

Q1 2011 | Q4 2011 | Q1 2012 | |

|---|---|---|---|

Annaly Capital | 2.17% | 1.71% | 1.71% |

Sources: S&P Capital IQ and company press release.

Falling spreads have hit the entire industry, regardless of strategy or makeup, including American Capital Agency (NAS: AGNC) , tiny Armour Residential (NYS: ARR) , Chimera (NYS: CIM) and Invesco (NYS: IVR) .

Ordinarily, declining interest rates wouldn't be such a big deal, since it would lower borrowing costs, but with the Fed funds rate up against 0%, there's not a lot of room for short-term rates to fall:

These spreads are still quite wide -- for an agency REIT like Annaly, anything above 1% is good. But they have been declining somewhat. And while it's possible to imagine scenarios where spreads start to widen again in the medium term, I wouldn't bet money on them happening for an extended period.

2. Leverage is down

Annaly has been ratcheting down its leverage over the past year in response to lower yields. Agency-REITs Armour and American Capital Agency are running significantly higher amounts of leverage, with American Capital Agency and Invesco actually ratcheting up over the past year.

Although that puts Annaly's dividend at a relative disadvantage to its peers, it is a safer position to be in. Annaly-managed Chimera took a similar tack last fall.

Company | Q1 2011 Debt-to-Equity Ratio | Latest Debt-to-Equity Ratio |

|---|---|---|

Annaly Capital | 6.3 | 6.0 |

American Capital Agency | 6.6 | 8.5 |

Armour Residential | 9.5 | 9.3 |

Invesco | 3.7 | 6.2 |

Chimera | 1.8 | 1.8 |

Sources: S&P Capital IQ and company press releases.

3. Prepayments are steady

Annaly's constant prepayment rate fell to 19% from 22% last quarter. Mortgage holders generally don't like high prepayment rates, because they reduce interest income. The White House has been attempting to help more homeowners refinance, but most REITs have said they don't expect to be much affected. With so many homes underwater and banks hesitant to extend credit, prepayment rates are lower than you'd expect them to be for such low interest rates, and they're unlikely to increase dramatically, though Annaly has said it's keeping a close eye on this area.

The Foolish bottom line

Despite falling long-term rates, we're still in the golden period for residential mortgage REITs (although we're probably nearing the later stages). Annaly continues to yield 13.4%, while REITs with higher leverage are squeezing out a few more points. With favorable interest and prepayment rates basically locked in, we can expect that to continue for about another couple of years.

But I'll be keeping an eye on those declining interest rates spreads and falling leverage, since they'll continue to hold back Annaly's massive dividend a bit in the meantime. If you're looking for some other great dividend stocks, I suggest you check out "Secure Your Future With 9 Rock-Solid Dividend Stocks," a special report from the Motley Fool about some serious dividend dynamos. I invite you to grab a free copy to discover everything you need to know about these nine generous dividend payers -- simply click here.

At the time thisarticle was published Ilan Moscovitz doesn't own shares of any company mentioned. The Motley Fool owns shares of Annaly Capital Management. Motley Fool newsletter services have recommended buying shares of Annaly Capital Management. The Motley Fool has a disclosure policy.

We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.