Can Dean Foods' Rally Last?

Shares of Dean Foods (NYS: DF) hit a 52-week high on Wednesday. Let's take a look at how the company got there and whether clear skies remain in the forecast.

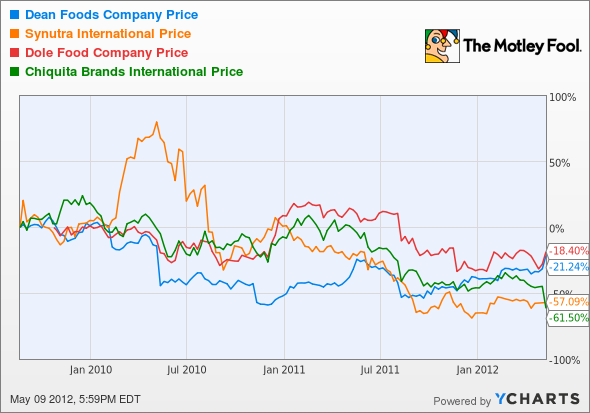

How it got here

Sometimes stocks quietly rise to a 52-week high. That's not been the case with Dean Foods, which roared to a new high yesterday following robust first-quarter results.

Suffice it to say, investors who have stuck with the stock despite its multiyear downswing finally got the report they've been waiting for. Milk prices finally stopped rising, which kept them from squeezing Dean's margins for the first time in a long while. However, the real growth driver wasn't the lack of margin pressure so much as the 13% sales growth it noted in its WhiteWave-Alpro organic foods and plant-based beverages segment.

I wish I could say everything was peaches 'n' cream, but the company did warn that weak retail prices, rising butterfat expenses, and accelerating fuel costs could affect the company's bottom line during the second half of the year. That still didn't stop Dean from boosting its full-year EPS forecast to $1.10-$1.20 versus Wall Street's expectations of just $0.95. Dean now joins Fresh Del Monte (NYS: FDP) as one of the few food producers to have sailed past the Street's estimates. Both Chiquita Brands (NYS: CQB) and Dole Food (NYS: DOLE) fell well short of consensus estimates in their latest reports.

How it stacks up

Let's see how Dean Foods stacks up next to its peers.

Yuck! It's at times like this I wish I had a white flag handy! We've seen what inflationary pressures have done to food producers over the past five years; now let's look more closely at their financials.

Company | Price/Book | Price/Cash Flow | Forward P/E | Cash/Debt |

|---|---|---|---|---|

Dean Foods | N/M | 5.8 | 12.6 | $115 million / $3.87 billion |

Synutra International (NAS: SYUT) | 3.7 | 9.9 | 6.1 | $46 million / $214 million |

Dole Food | 1.0 | 23.3 | 6.5 | $106 million / $1.69 billion |

Chiquita Brands | 0.3 | 6.8 | 5.1 | $45 million / $572 million |

Sources: Morningstar and Yahoo! Finance. N/M = not meaningful.

Holy leverage, Batman! Dean Foods actually boasts such a large amount of debt that it has negative shareholder equity. In fact, CEO Gregg Engles noted yesterday in an interview with CNBC that his company had no intention of paying a dividend until it had reduced its leverage. Chiquita was actually one of yesterday's worst-performing stocks after badly missing Wall Street's estimates and issuing a salad recall at one of its subsidiaries, but it now is the cheapest of the bunch (by far) according to book value. Dole Foods also uses a lot of leverage to run its operations, which has put extra pressure on its management team to perform well. Little Synutra may actually offer the best value of the group with just $214 million in debt and trading at just six times forward earnings. If there's anything to be learned here, it's that rising costs and high levels of debt are not a good combination.

What's next

Now for the real question: What's next for Dean Foods? The answer is going to depend on whether it can keep its pesky costs under control and if it can continue to pass along rising input costs to consumers. Based on its results over the past couple of years, I'm not all that hopeful.

Our very own CAPS community gives the company a three-star rating (out of five), with a robust 89.9% of members expecting it to outperform. Although I have yet to make an official CAPScall either way on Dean Foods, my instinct is to err on the side of caution and rate the stock an underperform.

"Why?" you wonder? Very simply because I don't believe in Dean's management. Dean's CEO, Gregg Engles, has averaged $20.4 million in compensation over the past six years while Dean's stock has fallen by an average of 11% annually over that period. Based on Forbes' rankings of 196 qualifying CEOs, Mr. Engles ranks dead last with regards to value-for-performance. This doesn't even begin to address Dean Foods' nearly $3.9 billion in debt or inability to control costs. I see the company as a ticking time bomb and I will look to enter a CAPScall of underperform if it heads much higher.

If you'd like the inside scoop on three American companies that are looking like they're set to outperform, then look no further than these three picks from our analysts. Get your report for free by simply clicking here.

Craving more input on Dean Foods? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.The Motley Fool owns shares of Dean Foods. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.