Does MAKO Surgical Deserve This Beating?

There's only one word for shareholders of MAKO Surgical (NAS: MAKO) today: Ouch. That includes me, mind you, so I'm also hurting with all you MAKO investors out there. Shares have gotten crushed by more than 37% at the low today after the company reported a weak first quarter. How bad could it be?

Figures first

Revenue in the first quarter came in at just $19.6 million, well short of not only the consensus estimate of $23.8 million, but also shy of even the lowest sales estimate of $22.9 million. MAKO generated a net loss of $11.7 million, or $0.28 per share, also worse than expected.

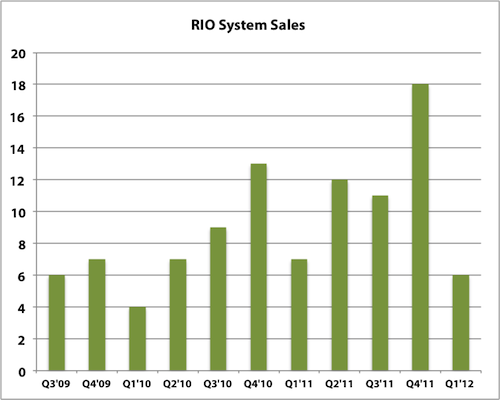

There were only six RIO systems sold during the quarter, increasing the worldwide commercial installed base to 118 and the domestic commercial installed base to 116. MAKOplasty procedures performed in the quarter jumped 76% to 2,297, including 211 Total Hip Arthroplasty, or THA, procedures. MAKO sold 13 THA applications to upgrade older RIO systems for the new procedure, and 53% of the domestic installed base can now serve up THA procedures.

Ouch

One of those six RIO systems was sold to a distributor in Japan to try to land regulatory approvals and also to demonstrate the system to build interest in the region. The revenue on this system has been deferred due to a contingent obligation to reimburse costs associated with the regulatory process if things fall through, but should be recognized if and when regulatory approval is granted.

Deferred revenue only rose by $443,000 from December, so this one system doesn't come close to covering the shortfall. There's really no way to sugarcoat it: RIO system sales were disappointing.

Source: Earnings press releases.

The last time we saw this few RIO system sales was two years ago, when four were sold in first-quarter 2010. A sequential drop-off in the first quarter from seasonal factors is expected, but this quarter's was particularly brutal. Especially considering the strong showing in the fourth quarter that gave investors hope that adoption was accelerating.

CEO Maurice Ferre said the results were on the low end of the company's expectations, although management is encouraged by continued interest in the THA application. As a result of the soft RIO sales, MAKO is now slashing its outlook on RIO systems this year. The company now expects to sell between 52 and 58 systems throughout 2012, down from the previous guidance of 56 to 62 systems. On the bright side, total MAKOplasty procedure volume guidance is standing pat at 11,000 to 13,000 expected this year.

The burning question

MAKO has also entered into a credit facility agreement with Deerfield Management, allowing MAKO to borrow up to $50 million as needed in $10 million increments at any time over the next year. If the company decides to borrow, it has three years to pay it back.

The real kicker to this agreement is that MAKO has issued Deerfield warrants to buy 275,000 shares, which would dilute existing shareholders if exercised. Deerfield can buy those shares at an exercise price that's 20% higher than the average close over the next 20 days, starting today. With today's plunge, Deerfield might have a reasonable entry price if MAKO is able to recover from this quarter's stumble over time, since these warrants are good for seven years.

On top of that, if MAKO draws any of the $10 million increments, Deerfield will get additional warrants for 140,000 shares each time, with an exercise price that's 20% higher than the average close over the following five trading days. So we're talking about a potential total of 975,000 shares being issued if MAKO taps all $50 million, only 2.3% of the current 41.4 million shares outstanding.

The scary part is that just last quarter, CFO Fritz LaPorte had said that it was unlikely that MAKO would need to tap capital markets for funding, and this agreement is laying the foundation for that tapping just three months later.

MAKO still has $46.8 million in cash and investments on the books, and LaPorte is sticking by his forecast of burning through $25 million to $30 million throughout the full year, so hopefully it won't need to tap this credit facility.

What's a Fool to do?

There are a couple of silver linings. Gross margin expanded to 72%, and THA procedures are off to a healthy start. MAKO expects about 1,200 THA procedures to be performed this year.

MAKO is particularly vulnerable to earnings misses as an unprofitable company trading at 21 times sales, and these results really put the pressure on it to deliver for the balance of the year. Shares may have gotten a little too frothy going into the release as expectations were high.

This was undoubtedly a weak quarter, but one miss doesn't unravel MAKO's long-term prospects. If this proves to be the beginning of a trend of misses, then that would be a different story. MAKO has a long way to go to live up to its role model Intuitive Surgical (NAS: ISRG) , and while there are some comparisons there are also some differences.

Today's drop is a buying opportunity for opportunistic bulls, since I still think MAKO will prove to be a multibagger in the long run. It will be a roller coaster along the way, but I knew that on the way in.

If you're looking for a little stability instead of MAKO's volatile ways, then Secure Your Future With 9 Rock-Solid Dividend Stocks. These stalwarts are profitable and have plenty of cash flow, so they won't have nearly the same types of swings. Get the free report now.

At the time thisarticle was published Fool contributor Evan Niu owns shares of MAKO Surgical, but he holds no other position in any company mentioned. Click here to see his holdings and a short bio. The Motley Fool owns shares of MAKO Surgical and Intuitive Surgical. Motley Fool newsletter services have recommended buying shares of MAKO Surgical and Intuitive Surgical. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.