At a 52-Week Low, Is There Any Hope for Coeur d'Alene?

Shares of Coeur d'Alene Mines (NYS: CDE) hit a 52-week low on Monday. Let's take a look at how it got there and whether cloudy skies are still in the forecast.

How it got here

Like other metal miners, Coeur d'Alene has suffered primarily from two factors. First, the cost of its underlying metal, in this case -- silver, has corrected downward, which is putting near-term pressure on margins even though it sold its silver for 4% more than the year-ago quarter based on its first-quarter results released yesterday. The big drag was Coeur d'Alene profits missing Wall Street's earnings expectations because of a shortfall in gold production.

The second aspect hampering the company has been the rising costs of diesel fuel and labor. Although these costs have been more than offset by increased mining efficiencies, Coeur d'Alene has been crushed along with those companies in the silver sector that haven't figured out how to deal with their higher costs.

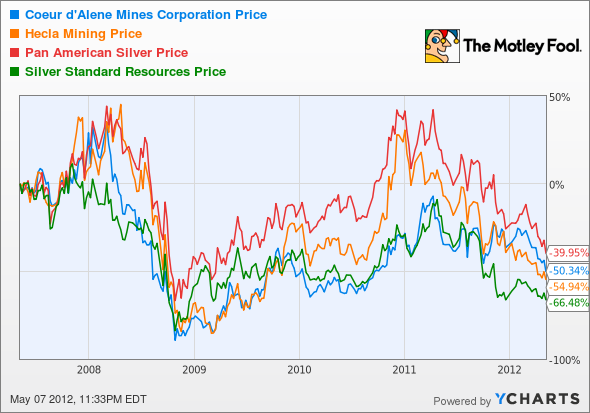

How it stacks up

Let's see how Coeur d'Alene stacks up next to its peers.

Despite silver having risen by a significant amount over the past five years, silver miners haven't exactly come along for the ride.

Company | Price/Book | Price/Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

Coeur d'Alene | 0.8 | 3.9 | 6.4 | 36.3% |

Hecla Mining (NYS: HL) | 1 | 16.2 | 7.1 | 17.1% |

Pan American Silver (NAS: PAAS) | 1.7 | 5.1 | 8.2 | 27.4% |

Silver Standard Resources (NAS: SSRI) | 1 | 177 | 13.7 | N/A* |

Sources: Morningstar, author's calculations, *Silver Standard's production is less than five years old, CAGR = compound annual growth rate.

Unlike the gold mining sector, where seemingly everything is a bargain, you have to dig a little deeper in with the silver miners (pun completely intended).

Hecla Mining is cheap for a reason since the Mine Safety and Health Administration ordered the closing of its Lucky Friday mine in January because of safety issues. With that production on the back burner for at least a year, it's understandable why the stock is lower. Silver Standard Resources recently began producing silver, so its main drag -- outside of that ridiculous price-to-cash-flow of 177 -- is its mining costs, which are higher than its peers mentioned here. Pan American Silver is a company I profiled in December as intriguing because of its valuation and strong cash position. That valuation has only grown even more delectable since then. Finally, there's Coeur d'Alene, which has fended off rising prices and reaffirmed its silver production forecast, looking like the cheapest of the bunch.

What's next

Now for the real question: What's next for Coeur d'Alene Mines? That question is going to depend on what the underlying price of silver does over the long term and whether the company can continue to keep its mining costs under control. Admittedly, no one in the sector can control costs or command the margins that Silver Wheaton (NYS: SLW) can because of its long-term low-cost contracts, but Coeur d'Alene appears, so far at least, to have its costs well under control.

Our very own CAPS community gives the company a three-star rating (out of five), with an overwhelming 94.1% of members expecting it to outperform. Although I have yet to make a CAPScall on Coeur d'Alene in either direction, I'm ready to end that indecisiveness now with a pick of outperform.

Coeur d'Alene hit all the key points for me in its latest quarterly report despite the profit miss. It kept its production forecast unchanged at 18.5 million-20 million ounces of silver and 210,000-230,000 ounces of gold, while also alluding that silver mining costs would remain largely unchanged despite rising fuel and labor costs. The company's cash balance improved, as did its cash flow during the quarter. Finally, the company's Kensington mine in Alaska is back up and running much quicker than anticipated. Coeur d'Alene doesn't deserve to be trading below book value and is an easy outperform call here.

If you'd like the inside scoop on three more stocks that will help you retire rich, then simply click here for access to our latest special report -- it's free!

Craving more input on Coeur d'Alene? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Pan American Silver. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.