This Stock Has Multibagger Potential

Today I'm going to take a closer look at a company that refuses to be ignored. SolarWinds (NYS: SWI) has appeared frequently on two of my Rising Star screens, and the market has rewarded its strong performance with a double over the past year.

Nothing to do with solar

The Austin, Texas, company is not in the energy business, but develops IT infrastructure management software for organizations of all sizes. Its core business is network management software, led by the flagship product Network Performance Monitor.

Over the past several months, management has moved beyond its roots and emphasized growth in other areas, including virtualization management and log and event management. This means the company is squaring off against some heavy hitters, including EMC (NYS: EMC) , NetApp (NAS: NTAP) , and VMware (NYS: VMW) . But SolarWinds is attacking the competition in a novel manner, which I'll get to in a moment.

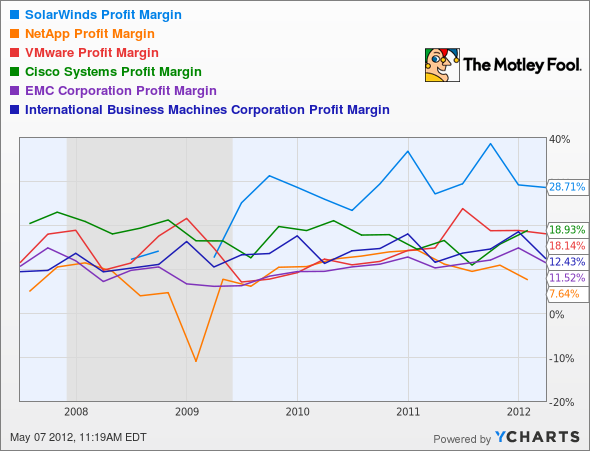

Growth has been fantastic, and that's why the stock price has done so well. The top line grew by more than 30% in 2011, and the recent first-quarter earnings report shows 39% year-over-year growth.

Fresh new breeze

Competitors like Cisco (NAS: CSCO) and IBM get a lot of their software business from brand recognition and natural follow-ons from their hardware installations. SolarWinds can't compete in that manner, and instead brings a disruptive approach to the IT management industry. Its business model emphasizes ease-of-entry for new clients, affordability, and scalability. The company's marketing tends to drive potential users to the website, and the process often begins with clients downloading free software for evaluation or to solve a particular problem. This results in highly qualified leads who often convert to paying customers. This process is more cost-effective than the competition's, and leads to some extremely high margins.

SWI Profit Margin data by YCharts

Buying spree

Management has enacted quite a few acquisitions during this hyper-growth phase. How well it integrates these is a huge key for me. So far, so good, but goodwill write-offs can really hurt a company's stock price.

SolarWinds' intangible assets ratio -- simply the percentage of total assets comprised of goodwill and other intangibles -- is running at about 45%. That's comparable to the ratios at Hewlett-Packard and EMC, which are also over 40%. IBM, NetApp, and VMware carry more reasonable ratios.

As I've mentioned in my ongoing goodwill series, a figure over 20% means write-offs could really dent earnings, so management better be on its game.

At what price?

You're probably guessing that a company with this type of growth is not exactly selling for a bargain price. Well, good guess. SolarWinds' trailing P/E is 50, and it's trading at 33 times next year's earnings. Lofty indeed. But a company at this stage of its life cycle and exhibiting these strong characteristics will naturally carry a high multiple.

My thoughts are that this is a risky stock, but the upside is enough that I'm considering a small starting position for my portfolio. I'll have my decision soon.

Meanwhile, our Rule Breakers team has bought another high-risk, high-reward company. Find out which one in our special report, "Discover the Next Rule-Breaking Multibagger." It's yours for free.

At the time thisarticle was published Fool analyst Rex Moore tweets but is not a twerp. He runs a real-money Rising Star portfolio based on his screens. He owns no companies mentioned in this article. The Motley Fool owns shares of EMC, International Business Machines, and Cisco Systems. Motley Fool newsletter services have recommended buying shares of VMware. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.