How High Can These Retailers Fly?

Shares of department store rivals Dillard's (NYS: DDS) and Nordstrom (NYS: JWN) both hit a 52-week high yesterday. Let's take a look at how the companies got there to find out whether clear skies remain on the horizon.

How they got here

Dillard's has had a relatively quiet year so far, but it's been the bigger gainer of the two, riding investor sentiment higher since the end of January on the combined strength of strong third- and fourth-quarter results and a still-ridiculously low valuation that now sits at a P/E of 7.5. Nordstrom's April same-store sales came in yesterday morning, showing 7.1% growth, with quarterly same-store sales growth even better at 8.5%.

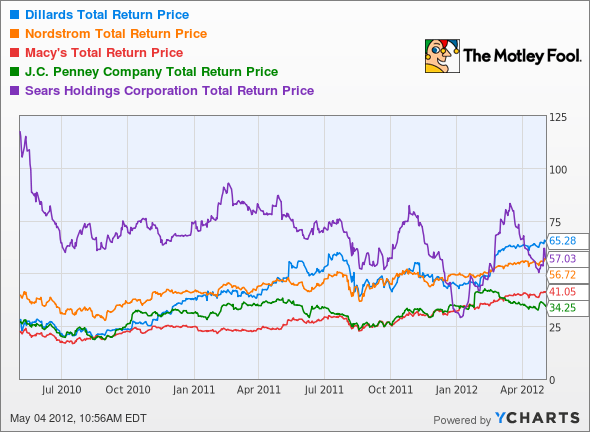

Both companies have done well over the past year, but Dillard's is clearly the stock star of this retail subsector, leaping to greater heights over the past two years as its postrecession recovery kicked into gear:

DDS Total Return Price data by YCharts.

Nordstrom had a pretty good holiday quarter in its own right, and will report first-quarter earnings next week, so another strong performance could be a catalyst for further gains.

What you need to know

A quick glance at some of these competitors' key numbers can give you a quick understanding of why Dillard's has outperformed. Its annualized earnings growth trounces Nordstrom's and Macy's (NYS: M) , which have also successfully rebounded from a poor sales environment (to put it mildly). Its net margin is currently the highest of the group's:

Company | P/E Ratio | Annualized 3-Year Earnings Growth | Net Margin (TTM) |

|---|---|---|---|

Dillard's | 7.7 | 89.2% | 7.3% |

Nordstrom | 18.1 | 15.7% | 6.3% |

Macy's | 14.2 | 56.3% | 4.8% |

JC Penney (NYS: JCP) | NM | NM | (0.9%) |

Sears Holdings (NAS: SHLD) | NM | NM | (7.6%) |

Source: Yahoo! Finance. NM = not material due to negative earnings. TTM = trailing 12 months.

Nordstrom also suffered a (comparatively) mild downturn compared to its peers; it is the only one of this group to have had a solid decade of positive earnings. Macy's and Dillard's both went into the red during their 2008 fiscal years, and both JC Penney and Sears never recovered from steep recessionary drops, entering negative territory in 2011. That accounts in part for Nordstrom's higher valuation. Investors seem to view it as the most stable, and thus the most deserving of a higher premium.

What's next?

Where do these retailers go from here? That will depend, for Nordstrom, on the strength of its upcoming earnings in the near term, and for Dillard's, on the market gaining confidence in its long-term stability. The Motley Fool's CAPS community seems to have little faith in either company, granting Nordstrom a two-star rating, and Dillard's a single star out of five.

Only 39% of those who chimed in on Dillard's CAPS page thought it would outperform the market going forward. I respectfully disagree, and will be initiating an outperform CAPSCall on the stock based on its rock-bottom valuation and on Fool analyst Jim Mueller's analysis of Wall Street's messed-up expectations for the company. I'll be adding Nordstrom to my Watchlist, and might make a call on it one way or the other if earnings show me something unexpected.

Not sure if these retailers can beat the market this year? The Motley Fool's got another retail opportunity that's so appealing we've dubbed it our "Top Stock for 2012," and we're inviting you to learn more at no cost. Find out everything you need to know to make your next great portfolio addition -- click here to claim your free copy of this report now.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.