Will This Consumer Goods Titan Whiff on Earnings?

Church & Dwight (NYS: CHD) will report earnings before the market opens Friday. Analysts expect the household, personal care, and specialty products manufacturer to report $672.96 million in revenue and $0.61 in EPS, which would be a slight 5.17% improvement over last year's reported $0.58 for the same quarter. If the company meets its revenue target, it'll mark a 4.8% increase from last year's $642.3 million.

Let's see how those figures compare with some of Church & Dwight's competitors: The Clorox Co. (NYS: CLX) , Procter & Gamble (NYS: PG) , Kimberly-Clark (NYS: KMB) , and Johnson & Johnson (NYS: JNJ) .

Company | Reporting Date | Revenue | EPS |

|---|---|---|---|

Clorox | May 2 | $1.35 billion | $1.03 |

Procter & Gamble | July 30 | $20.74 billion | $0.85 |

Johnson & Johnson | July 16 | $16.72 million | $1.30 |

Kimberly-Clark | July 12 | $5.92 billion | $1.28 |

Clorox just reported and exceeded revenue expectations but missed earnings estimate. A Clorox spokesperson said the company expects commodity prices to continue their ascent into FY13. Procter & Gamble recently reported $0.94-per-share earnings for its last quarter, a penny better than consensus, but the company missed revenue projections. Johnson & Johnson posted $1.37-per-share earnings last quarter, also one cent higher than estimates, but also missed its revenue target by $200 million. Kimberly-Clark reported in late April and beat earnings estimates by $0.07 a share and revenue by $200 million.

When looking at earnings quality, we at The Motley Fool have two databases -- EQ Scan and EQ Score -- that help us uncover cash flow and revenue recognition issues. Smart financial officers can use several techniques to manipulate financial results, and manipulation of any of the three financial statements usually affects the other two. But a critical eye on these statements can often uncover trends that could be important to help investors protect against losing their hard-earned money. The EQ Score database assigns an index rank to the company, from 1, for the lowest quality, to 5, for the highest. As the company's financial status changes over time, the database adjusts its rank and illuminates trends that will affect earnings quality going forward. The EQ Score ranks Church & Dwight as a "2", equivalent to a "D" letter grade. Let's see why.

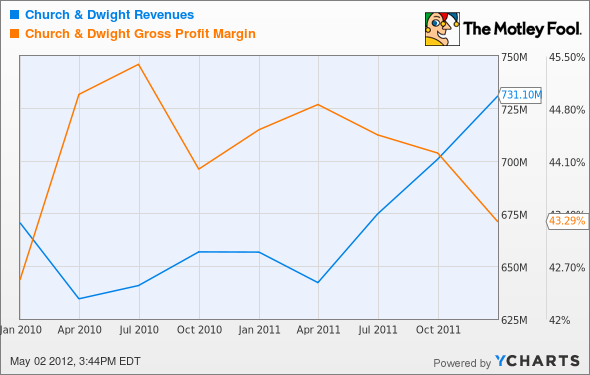

CHD Revenues data by YCharts

The first chart shows revenues trending upwards by 11% year over year. However, remember that analysts expect $673 million in revenue for this quarter, and so the trend line will end up as essentially flat. The gross margin shows some deterioration since last April, down from 44.8% to 43.29% -- a 3% decline. This means the cost of goods sold has been rising, showing an increase of 14% year over year. To summarize, costs are rising slightly faster than is revenue.

CHD Cash Operations data by YCharts

Church & Dwight has been busy making acquisitions over the past several years, spending a total of $196.2 million on acquisitions since the start of 2010, and $922.1 million since 2006. Cash from operations has benefited from a steady diet of deferred income taxes added back from previous years' tax losses accrued. The free cash flow line shows that Church & Dwight has made capital expenditures to benefit its business. But the cost of acquisitions should be factored into the cash flow mix as well. C&D has been buying some growth.

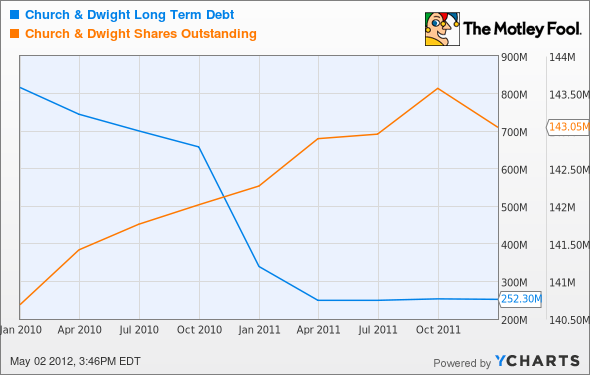

CHD Long Term Debt data by YCharts

The third chart shows Church & Dwight has used long-term debt and the issuance of stock to help fund its acquisitions. As interest rates have come down, the company has retired debt and issued new debt to take advantage of the lower rates. In total, however, Church & Dwight has reduced its debt exposure from $602.5 million at the start of 2010 to $252.3 million as of the end of 2011. Total debt to total capital now stands at a very manageable 11%.

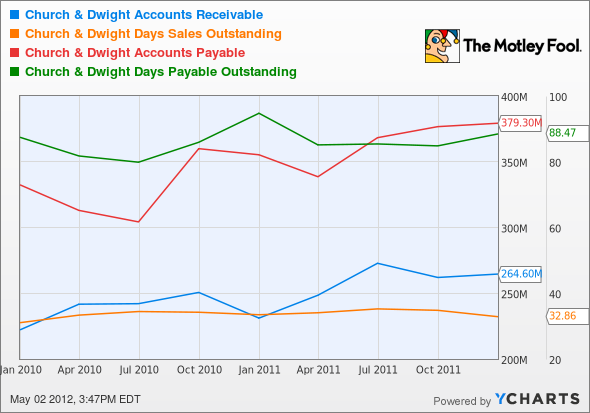

CHD Accounts Receivable data by YCharts

The last chart reveals why Church & Dwight's earnings quality is worse than it could be. Simply put, the company has used the 55-day spread between receivables and payables as short-term financing. Payables have increased by approximately $100 million since January 2010 and days payable outstanding is a very high 88 days. Ouch! On a four-quarter average basis, accounts payable is at a very unhealthy 48% of revenue. On the receivables side, days sales outstanding is around 33 days, but still receivables are up 14% year over year.

Church & Dwight has been adding to its arsenal of products in order to compete with its much larger competitors. But as we have seen, these acquisitions were funded with a combination of debt and stock. Since Aug. 8, 2011, the company's stock price has ticked up from $37.01 to $50.99 currently, a 37.77% jump. Church & Dwight has a trailing P/E of 24.05. Last year's earning came in at $2.22, and analysts expect the company to earn $2.41 a share this year, a modest 8.56% bump up but far lower than the climb of Church & Dwight's stock price. As always, prudent Fools should make investment decisions based on consideration of earnings quality.

To stay current on whether Church & Dwight's earnings report meets, misses, or beats expectations, be sure to add it, or any of the other companies mentioned here, to My Watchlist, a totally free service offered by The Motley Fool that keeps you current on your favorite stocks. Get started with the links below.

Add Procter & Gamble to My Watchlist.

Add Kimberly-Clark to My Watchlist.

Add Johnson & Johnson to My Watchlist.

Add The Clorox to My Watchlist.

Add Church & Dwight to My Watchlist.

At the time thisarticle was published Fool contributorJohn Del Vecchiois Co-Advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter @johnfdelvecchio. He does not own any shares in the companies mentioned in this article. The Motley Fool owns shares of Clorox and Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Procter & Gamble, Johnson & Johnson, and Kimberly-Clark.Motley Fool newsletter serviceshave recommended creating a diagonal call position in Johnson & Johnson. The Motley Fool has adisclosure policy.We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.