Atmel Earnings Preview: Calling the Bottom?

Touchscreen microcontroller specialist Atmel (NAS: ATML) is set to report earnings tomorrow. The company has been held back lately by the absolute underwhelming performance of Google (NAS: GOOG) Android tablets -- those not named the Amazon.com (NAS: AMZN) Kindle Fire.

This is also the same theme that's been limiting rival Cypress Semiconductor's (NYS: CY) upside, although Cypress' share in Android tablets lags Atmel's dominant lead.

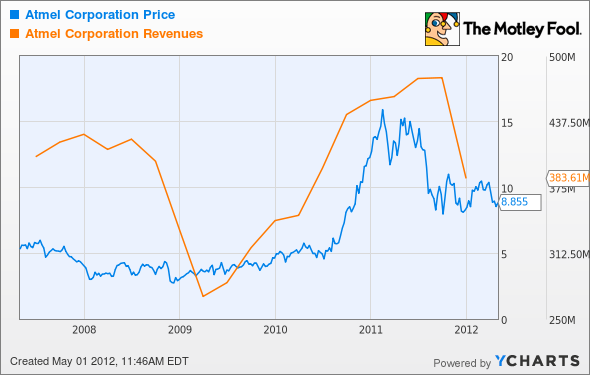

As far as the Street is concerned, analysts are looking for top-line revenue of $352 million, which would be a decline of nearly 24% compared to the $461.4 million in revenue last year. Remember that Atmel divested its lower-margin Smart Card business in the third quarter of 2010, so this year-over-year drop is an apples-to-apples comparison. Up until recently, it was useful to look at Atmel's figures before and after adjusting for this divestiture.

Adjusted earnings per share is predicted to be $0.04, a quarter of what it was a year ago. Analysts have it pegged to a fairly narrow range, with estimates only ranging from $0.03 per share to $0.05 per share. Don't expect this quarter to be a stellar one, as CEO Steven Laub previously said that it should be the bottom before things start getting better.

The Kindle Fire remains the best-selling Android tablet right now, with estimates that it now gobbles up more than half of the Android tablet market. The touchscreen controller in that tablet is provided by Ilitek, although there have been numerous rumors that Atmel has scored the design win in the second-generation Kindle Fire, which would be a cushy spot to sit in.

Atmel's newest maXTouch S Series of touchscreen controllers was also recently certified for Microsoft (NAS: MSFT) Windows 8, which should be another opportunity for Atmel to tap into tablet growth as Windows 8 will spearhead the software giant's tablet strategy. Windows 8 devices aren't expected until later this year, so any upside for Atmel will also have to wait.

The company has been transforming and restructuring itself for years, and has emerged stronger and more profitable. Now it just needs to tap into tablet growth.

Atmel is looking to ride the wave that is "The Next Trillion Dollar Revolution." While it's still waiting to catch its break, another company is already gaining momentum. Get the free report now.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Amazon.com and Cypress Semiconductor, but he holds no other position in any company mentioned.Click hereto see his holdings and a short bio. The Motley Fool owns shares of Microsoft, Amazon.com, and Google.Motley Fool newsletter serviceshave recommended buying shares of Microsoft, Google, Cypress Semiconductor, and Amazon.com.Motley Fool newsletter serviceshave recommended creating a bull call spread position in Microsoft. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.