3 Value Investing Myths Busted

I'll admit it: Value investors aren't the life of the cocktail party. We're usually the underdressed ones who stink-bomb conversations with lines like "Social media is a fad, but let me tell you about this micro-cap asbestos manufacturer!"

But we're not all boring, cynical, curmudgeonly folks. And we didn't get this way because we were born old souls. Here, in advance of the lollapalooza that is the Berkshire Hathaway (NYS: BRK.A) (NYS: BRK.B) annual meeting, are three debunked myths about the artful science that is value investing and its practitioners.

Myth No. 1: Value investing is for old people.

You don't need an AARP membership to appreciate the charm of buying a dollar for $0.50. Value investing is like extreme couponing, only for your stocks instead of Hot Pockets. The idea is that you buy businesses at discounts to their true worth and wait for time, fundamentals, and management to help unlock that value.

It doesn't help matters that the face of value investing, Berkshire's Warren Buffett, is that of an octogenarian. But there are plenty of smart, young investors who have embraced the concept of buying down-on-their-luck businesses at fire-sale prices. Cases in point: Guy Gottfried and Isaac Schwartz, both of whom are speaking at the upcoming Value Investing Congress I'll be attending in Omaha on May 5 and 6. And then there are serial Value Investing Congress presenters Bill Ackman and David Einhorn, arguably the two best investors of their generation and contrarian to their core.

Some young investors tell me they prefer growth over value because they're looking for high-octane results while they can still afford to take on some risk. You can make growth investing work for you -- just ask the guys at Motley Fool Rule Breakers -- but robust empirical research (link opens PDF file) shows that buying cheap stocks instead of high-priced ones is a winning formula over the long term. In his classic book The Future for Investors, Wharton professor Jeremy Siegel explains that stocks with the lowest P/E ratios outperformed those with the highest by almost 5 percentage points annually and with lower volatility from 1957 through 2003. And instead of highfliers, the list of the top surviving firms includes predictable slow-movers Colgate-Palmolive, Hershey (NYS: HSY) , and PepsiCo (NYS: PEP) . So while you can beat the market by investing in high-priced stocks, you're swimming against the tide.

Myth No. 2: You can't beat the market buying large-cap stocks.

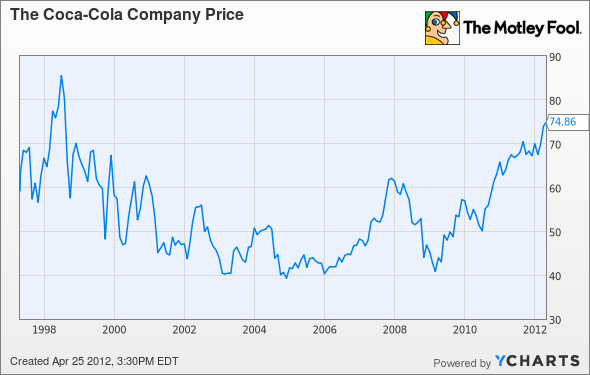

Not so. Case in point: Coca-Cola (NYS: KO) . Coke might have one of the most widely followed, easiest to understand businesses in America. You'd think that means the stock's price is almost stapled to its real worth, or intrinsic value, but that's not the case. Get a load of this chart:

The same Coke shares that sold for an absurd 61 times earnings in 1998 fell by 58% in value over the next five years. And since they hit their low in 2004? They're up a cool 102% -- plus dividends. Coke's century-old business is as simple and widely followed as any, but patient investors who preyed on Mr. Market's emotions could have bought or shorted Coke's stock at points where it was obviously under- or overvalued. Rinse, repeat.

Myth No. 3: Tech is a no-no.

Value hounds are right to be skeptical of high-flying tech stocks: Valuations are rich and competitive advantages can be fleeting. One day you're MySpace and the next, well, you're MySpace. But growth isn't a bad word and investors shouldn't live in the past. The pace of technological change is accelerating, business life cycles are shrinking, and the most important, world-altering businesses are the likes of Apple, Google, and Facebook.

Buffett himself, whom many value investors hide behind for their rationale of avoiding technology, said just last year at Berkshire's annual meeting that he would make learning more about investing in tech companies a top priority if he were an investor just beginning his career today. Lo and behold, he backed up the truck and bought almost $11 billion worth of IBM shares.

Moving cautiously into the tech sector isn't a betrayal of value investing principles. Instead, we're entering an age where some of the biggest potential gains for value investors lurk in the murky, tough-to-value waters of out-of-favor technology companies -- two of my favorites are Google and eBay.

Berkshire 2012

But enough about mythology. The real deal for value investors is happening this Saturday when Warren Buffett and longtime partner Charlie Munger will field dozens of pointed questions at the Berkshire Hathaway annual meeting. And on Sunday and Monday, you can hear from some of the brightest minds in the industry at the Value Investing Congress. Best of all, those of you stuck at home can follow the Fool's coverage of both events online at www.Berkshire.Fool.com. And that's no myth.

At the time thisarticle was published Joe Magyerowns shares of Google, eBay, and Berkshire Hathaway. The Motley Fool owns shares of Google, IBM, PepsiCo, Apple, and Berkshire Hathaway.Motley Fool newsletter serviceshave recommended buying shares of PepsiCo, Berkshire Hathaway, Google, Apple, and eBay, as well as creating a bull call spread position in Apple and a diagonal call position in PepsiCo. The Motley Fool'sdisclosure policyhas a poster of Warren Buffett in its man cave.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.