Will These Gunmakers Shoot Even Higher?

Shares of gunmakers Smith & Wesson (NAS: SWHC) and Sturm, Ruger (NYS: RGR) both hit 52-week highs today. Let's take a look at how the companies got there to find out whether clear skies remain on the horizon.

How it got here

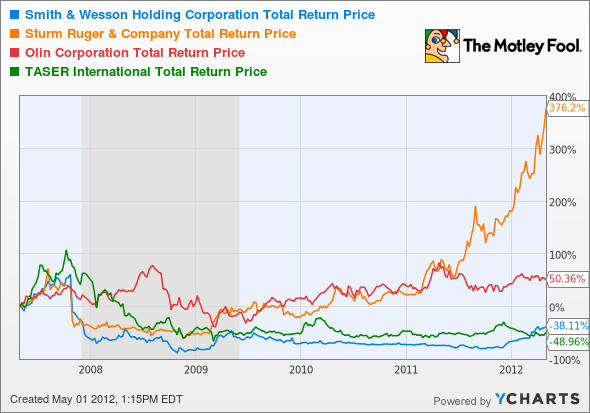

Smith & Wesson's rebound is of recent vintage, but Sturm, Ruger has been heading nearly straight up without pausing to catch its breath since President Barack Obama's inauguration. Until their recent in-tandem movements, the two companies' charts couldn't have looked more different:

SWHC Total Return Price data by YCharts

You got that right -- Sturm, Ruger has absolutely thrashed its personal-protection peers, including not only Smith & Wesson, but TASER (NAS: TASR) and ammo maker Olin (NYS: OLN) as well over the past half-decade. It might even be said that Smith & Wesson is benefiting from a surfeit of demand beyond what Sturm, Ruger can handle. High demand is always good news, and now that Smith & Wesson has left its unprofitable security division behind, it's finally starting to show investors the same positive earnings Sturm, Ruger investors have long enjoyed.

What you need to know

Sturm, Ruger remains the better value of the two gunmakers, and boasts a solid combination of still-reasonable P/E and impressive net margin:

Company | P/E Ratio | Annualized 3-Year Earnings Growth | Net Margin (TTM) |

|---|---|---|---|

Sturm, Ruger | 27.5 | 13.3% | 12.2% |

Smith & Wesson | 125.6 | NM | 1.1% |

TASER | NM | NM | NM |

Olin | 11.5 | 21.2% | 7.2% |

Source: Yahoo! Finance. NM = Not meaningful because of negative earnings.

Though Olin's P/E is lower, its business is more diversified -- with less than 30% of its revenue coming from its Winchester division last year -- and its margins are lower than Sturm's. Meanwhile, TASER's past performance has been simply miserable. Delivering 50,000 volts to assailants doesn't offer the same sense of security as the heft of a gun, I suppose.

Meanwhile, it's little wonder that Sturm, Ruger has beaten the rest of the group over the past few years. Smith & Wesson has gotten its fair share of positive analyst sentiment this year, but it's already blown past price targets set barely a month ago. Though Smith & Wesson has the lower forward P/E -- 18.1 to Sturm, Ruger's 20.2 -- it's the latter that has more demand than it can handle. That's still a better place to be.

What's next?

Where do these gunmakers go from here? That will depend on continued strength in the gun market, which seems unlikely to abate as long as the Democratic anti-gun boogeyman continues to scare gun lovers, however irrational that attitude might seem based on the legislative realities of the past three years.

The Motley Fool's CAPS community has given Sturm, Ruger a four-star rating and grants Smith & Wesson three stars. Sturm, Ruger earns an outperform call from 94% of players, with just under 93% anticipating Smith & Wesson's continued outperformance. I've personally issued outperform CAPSCalls on both and plan to maintain them at least until November -- but shareholders may very well be torn between hoping for an Obama loss for political reasons and his victory for financial ones (at least where these stocks are concerned). There's little reason to expect a big decline while order books remain stuffed full.

Interested in tracking these stocks as they (hopefully) continue to grow? Add these gunmakers to your watchlist now for all the news we Fools can find, delivered to your inbox as it happens.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.