Are These Hotel Stocks Right for You?

So far in 2012, the CEOs of both Marriott International (NYS: MAR) and Starwood Hotels (NYS: HOT) have stated that we are on the cusp of a golden age in travel. But with the global economy still a bit shaky, should investors really be rushing to buy a ticket for this potential gravy train? For the right investor, I give an enthusiastic... maybe. Read on to find out whether you're that investor, and if not, I'll help you find a better fit for your portfolio.

How golden will that new age be?

While the World Travel & Tourism Council recently downgraded the industry's GDP growth prediction for 2012 to 2.8% from 2011's 3%, that's still significant positive growth in a $6 trillion global industry. The outlook for hotels is even better, with revenue per available room expected to increase by 6.5% this year, according to PricewaterhouseCoopers.

But does five-star growth equal five-star returns?

Driving the hotel industry's growth will be the luxury hotel segment. It has been doing well during the economy's slow recovery, and that trend is expected to carry over into the upcoming "golden age."

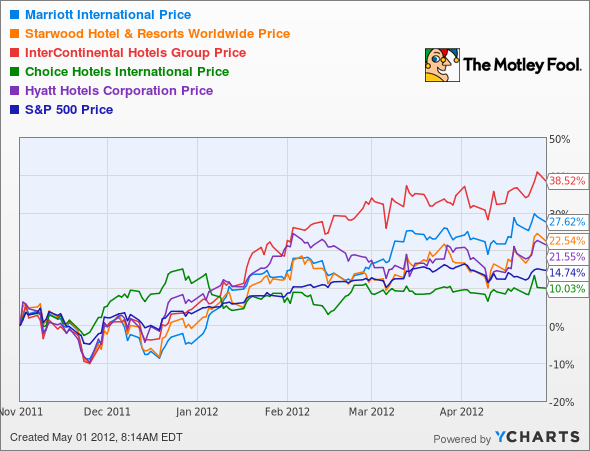

Just take a look at how well hoteliers with luxury brands in their portfolios have done lately. Along with Marriott and Starwood, Hyatt Hotels (NYS: H) and InterContinental Hotels Group (NYS: IHG) have beaten the market over the last six months. Compare that to Choice Hotels International (NYS: CHH) , which focuses largely on budget-friendly brands:

Choice obviously hasn't done poorly, up more than 10%, but it's definitely lagging in an industry that seems ready to take off.

Unfortunately for all of these companies, though, a lot of the industry's expected growth may already be baked into their stocks' current prices. Each is currently trading at or near its 52-week highs, and some have astronomical P/E ratios:

Company | Recent Price | 52-Week Range | P/E Ratio |

|---|---|---|---|

Marriott | $39.09 | $25.49-$39.39 | 67 |

Hyatt | $43.03 | $29.18-$45.72 | 66 |

InterContinental | $23.88 | $14.65-$24.34 | 26 |

Choice | $37.62 | $26.31-$39.50 | 20 |

Starwood | $59.20 | $35.78-$60.38 | 20 |

Source: Fool.com.

The Foolish bottom line

Personally, I have a lot of faith in the growth that these companies are expecting. InterContinental in particular has a well-balanced portfolio, in regard to both brand and geography. I also don't think the company's P/E ratio of 26 is out of reach, especially compared to Marriott's and Hyatt's much higher multiples. That's why I recently purchased shares of InterContinental for my IRA. The 3.1% dividend yield, which is fairly standard for the industry, doesn't hurt either.

It is a bit of a risky bet, though. If you're looking for something a bit more conservative, or maybe just something in a different industry, then you should check out this free report put together by some of our top analysts. It discusses three stocks that will help you retire rich and build a smarter retirement portfolio for long-term wealth. Click here to read it now!

At the time thisarticle was published Fool contributor Amanda Buchanan owns shares of InterContinental Hotels Group, but she holds no other position in any company mentioned. Click here to see her holdings and a short bio. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.