April's 5 Dividend Dynamos

As promised, this will be the year that I finally pay myself. As such, I'm always on the lookout for companies that are putting shareholders first. In 2011, we witnessed 1,953 dividend increases. Yet as Fool contributor Morgan Housel has pointed out, the overall payout ratio of the S&P 500 remains at a record-low 29%. This means it isn't enough just to find a dividend; it's about finding a growing and sustainable dividend.

After perusing some of April's finest, I've settled on five companies that I feel went beyond the call of duty to provide for their shareholders last month by increasing their payout or initiating a dividend payment.

Company | New Quarterly Dividend | Previous Quarterly Dividend | Increase |

|---|---|---|---|

Coach (NYS: COH) | $0.30 | $0.225 | 33% |

ExxonMobil (NYS: XOM) | $0.57 | $0.47 | 21% |

G&K Services (NAS: GKSR) | $0.195 | $0.13 | 50% |

Cracker Barrel Old Country Store (NAS: CBRL) | $0.40 | $0.25 | 60% |

TCP Capital (NAS: TCPC) | $0.34 | None | NM |

Source: Company press releases. NM = not meaningful.

Coach

Consumers' insatiable appetite for brand-name goods continues to be a driving force behind growth in the retail sector, with established names like Coach reaping the greatest benefits.

In its most recently ended quarter, Coach reported that sales in China increased by a whopping 60% and comparable-store sales in the U.S. grew 6.7%. Although Coach cautioned that growth was showing signs of slowing, there are far too many positives here to be erased by that one negative. The company removed coupons from its factory outlets due to strong sales, which should, in turn, propel margins even higher. The lack of coupons should also encourage consumers to trade up to pricier items -- a trend that was prevalent during the recent quarter. Finally, its direct-to-consumer business grew by 18% and gross margin expanded an additional 100 basis points to 73.8%.

Investors really shouldn't be surprised one bit by Coach's 33% hike in its quarterly payout, which will take its new yield to 1.6%. Since Coach began paying a quarterly stipend in June 2009, the company has significantly boosted its payout three times, and come this summer will now be paying out 275% more than it did just three years prior:

Source: Dividata. 2012 annual dividend is estimated based on new $0.30 quarterly payout.

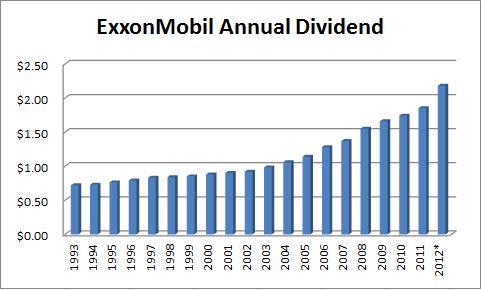

ExxonMobil

Even the largest oil and natural gas company in the U.S. isn't immune from the effects of decade-low natural gas prices and tightening crack spreads. ExxonMobil reported its first quarterly drop-off in profits in three years last week, but that still didn't stop the oil giant from smothering shareholders with a very large dividend increase that will amount to it paying out roughly $10.75 billion in payments next year.

I very easily could have included Chevron here, since it also produced a sizable dividend increase of its own, but I felt Exxon deserved the nod given the magnitude of the increase -- something it's not known for. What makes Exxon so extraordinary is the diversity present among its business segments. When one aspect struggles, like refining or natural gas, another segment picks up the slack. Unless oil prices were to fall to recessionary lows, Exxon shouldn't struggle to produce billions in quarterly profits.

Based on a quick glance at Exxon's payment history, the 21.2% dividend hike marks the largest percentage increase in its dividend in 25 years. That's saying something for a company that has increased its dividend for 30 straight years and will now be yielding 2.6% -- which is more in line with the diversified oil company average.

Source: Dividata. *2012 annual dividend estimated based on $0.57 quarterly payout.

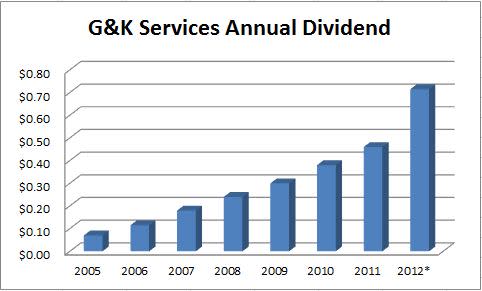

G&K Services

Uniform provider G&K Services may not exactly be a household name, but the company is doing everything under the sun to get income-seeking investors to take notice of it. Following another solid quarter in January in which revenue and margins increased and interest expenses dropped, G&K announced a whopper of a dividend increase earlier this month.

G&K took three steps to get money back to shareholders. First, it boosted its quarterly payout to $0.195, a clean 50% above the $0.13 it paid previously and leaps and bounds above the $0.0175 the company paid out quarterly for 13 straight years prior to 2006. What's more impressive, this marks the sixth time in the past seven years that the company has boosted its payout by 25% or more. Second, G&K still has $58 million remaining under a share repurchase agreement, so it will be looking to "opportunistically buy shares on the open market." Finally, the company declared a $6 special cash dividend that was payable to shareholders last week. I can't say I approve of using a revolving credit facility to pay for the $113 million special dividend, but the company's strong growth is hard to argue against at present.

Based on G&K's new yield of 2.3%, income investors would be wise to take notice of this up-and-coming name. Even better, based on its new annual dividend of $0.78, the company's payout ratio for fiscal 2012 is just 40% based on estimates found at Yahoo! Finance. That means there's still plenty of room for future dividend growth.

Source: Dividata. *2012 annual dividend estimated based on $0.195 quarterly payout.

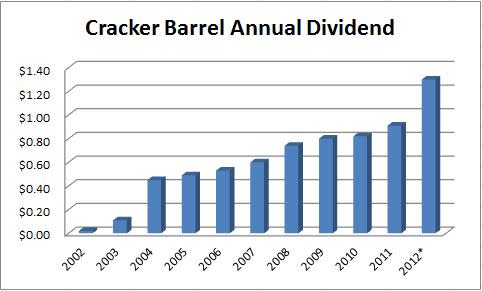

Cracker Barrel Old Country Store

Those of you who live in the Midwest are very familiar with Cracker Barrel restaurant and retail locations -- us West Coasters, not so much. But don't think for a moment that demographic isolation is affecting this company negatively in any way, shape, or form. We're seeing the same trends in Cracker Barrel that we're witnessing nationwide with regard to consumers spending more on discretionary outings. That's great news for Cracker Barrel and its chain of restaurants.

In an update just last week, Cracker Barrel noted that comparable customer traffic at its restaurants was up 0.6% so far in the third quarter with the average check increasing 2.5% and being the biggest growth driver. As consumers spend more, Cracker Barrel can loosen its wallet a bit and reward shareholders who stuck with the company through the worst recession in 70 years.

That's the primary reason the company chose last week to announce a huge increase in its quarterly payout -- 60%. Based on its new yield of 2.8%, the company is sure to turn the heads of income investors - especially since the new quarterly payment of $0.40 is 7,700% higher than the $0.005 it paid out in December 1999 and this is the 10th straight year of dividend increases.

Source: Cracker Barrel Investor Relations. *2012 annual dividend based on $0.40 quarterly payout.

TCP Capital

How's this for a market debut: On the same day that TCP Capital, an investment firm that is essentially an investment arm of Tennenbaum Capital Partners, went public, it initiated a quarterly dividend of $0.34! Well, hello and how do you do, TCP... come right on in!

TCP, which invests in debt securities for middle-market companies with valuations often between $100 million and $1.5 billion, didn't waste any time by declaring an annual dividend of $1.36, which produces an immediate yield of -- get this -- 9.4%! The company's investment portfolio consists of $379 million in investments and is wholly managed by Tennenbaum Capital Partners. Of that $379 million, debt securities make up 81% of the portfolio's fair value with investments across a myriad of industries.

With diversity of debt being at the heart of TCP's strategy, there's minimal risk to the dividend for shareholders despite the slow-growth nature of the business. This is another company that's far from a household name, but this dividend should definitely get the company on investors' radars.

Foolish roundup

Finding great dividends is all about value, growth, and sustainability, and these five companies definitely exhibited that in April. Consider adding these names to your free and personalized watchlist so you can keep track of the latest news on each company.

Also, if you'd like access to even more dividend-paying stocks, you should obtain a copy of our latest special report, "Secure Your Future With 9 Rock-Solid Dividend Stocks." As the name implies, we're going to give you access to some of the best dividend companies in the world, and best of all, this report is completely free, so don't miss out!

Add Coach to My Watchlist.

Add ExxonMobil to My Watchlist.

Add G&K Services to My Watchlist.

Add Cracker Barrel Old Country Store to My Watchlist.

Add TCP Capital to My Watchlist.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. He loves a dividend payment just as much as the next person. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Coach, ExxonMobil, and Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that puts investors first.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.