Will Broadcom Stumble in Qualcomm's Footsteps?

This earnings season is halfway done, and the parade of riders on the mighty coattails of Apple (NAS: AAPL) is coming to a close. Tuesday night, communications-chip designer Broadcom (NAS: BRCM) steps up to take a swing.

Few companies catch Apple's tailwind quite like Broadcom does. Only Samsung and Qualcomm (NAS: QCOM) provide a greater share of the hardware inside your average Apple gadget. Broadcom is a much smaller company than either one of those behemoths, so Apple should move Broadcom's needle farther and faster.

But Apple suppliers don't always follow Cupertino's stock chart swings. Qualcomm edged out analyst estimates on both the top and bottom lines, in no small part thanks to its iPhone and iPad involvement, but shares were punished the next day anyhow. Will Broadcom do any better?

Analysts don't expect any miracles out of Broadcom. Earnings are supposed to dip 19% year over year to $0.55 per share on nearly flat sales of $1.8 billion. Management didn't hand out any earnings guidance for the quarter, but the analyst top-line guesstimate is at the high end of the official revenue range.

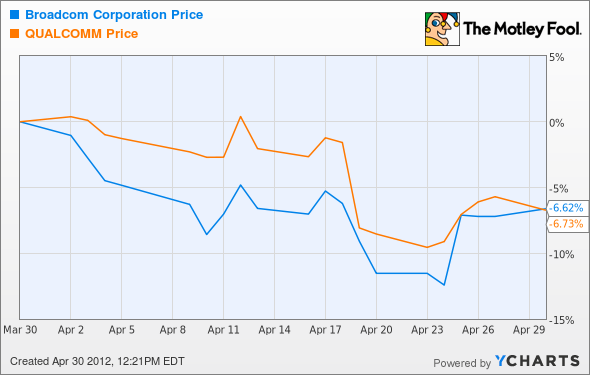

Qualcomm seems like a reasonable proxy for Broadcom's situation, given the way the two often walk hand in hand inside the same gadgets. The stock charts also look eerily similar lately:

So should we apply Qualcomm's pains equally to Broadcom? Well, investors developed an allergy to Qualcomm shares because the company is suffering supply-chain issues. Manufacturing specialist Taiwan Semiconductor Manufacturing (NYS: TSM) has more orders for cutting-edge 28-nanometer wafers than it can handle these days. That process is very popular in the mobile industry, which is why the shortage matters so deeply to Qualcomm and mobile processor expert NVIDIA (NAS: NVDA) .

Broadcom is another TSMC customer with deep interest in mobile computing. But its radio chips are less sensitive to leading-edge manufacturing technologies than the larger and more complicated products from NVIDIA and Qualcomm, so Broadcom often stays behind the curve for a while. In this case, Broadcom doesn't expect to ship high volumes of 28-nanometer chips until 2013.

That's why I give Broadcom a good chance of dodging this particular bullet. Qualcomm's next-quarter forecast looked weak because of the slow manufacturing ramp, but Broadcom really doesn't care yet. By the time the 28-nm process becomes mission-critical, TSMC should have ironed out these problems.

Every stock I've mentioned so far plays an important part in the trillion-dollar mobile computing revolution. Find out more about this market-quaking upheaval in this special report, including a deep analysis of one particularly juicy stock in the sector. But grab your copy quickly, because it won't be free forever.

At the time thisarticle was published Fool contributorAnders Bylundholds no position in any of the companies mentioned. Check outAnders' holdings and bio, or follow him onTwitterandGoogle+.The Motley Fool owns shares of Qualcomm and Apple.Motley Fool newsletter serviceshave recommended buying shares of Apple and NVIDIA, writing puts on NVIDIA, and creating a bull call spread position in Apple. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinion, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.