Why Spain Is Headed for Default

Forget the talk of "if Spain defaults." It's just a matter of time now until the world's ninth-largest economy comes to terms with its failure.

I don't say this lightly or to garner a jaw-dropping reaction but do it instead to point out blaring red flags that are only worsening and signal what appears to be an inevitable pirouette off a cliff.

Back in September I took a closer look at Spain's economic figures and felt there were striking similarities between it and Greece. I opined that if something weren't done quickly, the country would find itself begging for financial assistance in relatively short order. Unfortunately, not only have those fears been worsening, but the metrics I homed in on back then have actually been worsening at an exponential rate.

Let me walk you through some of the factors that have me the most concerned and I'll show you why I feel a Spanish default and subsequent bailout are inevitable.

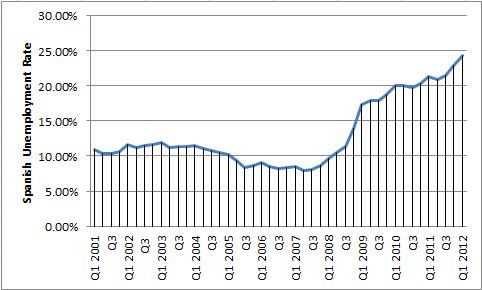

Unemployment rates are skyrocketing

You may have caught last week's headline about Spanish unemployment, but if you didn't, let me recap it for you: 24.4% of the population is now unemployed! That staggering figure doesn't even begin to tell the tale of what's wrong with an economy that has seen unemployment levels triple in just five years.

Source: TradingEconomics.

The real story is how impossible it is for the nation's youth to find work and how quickly the housing bubble has trashed the jobs markets.

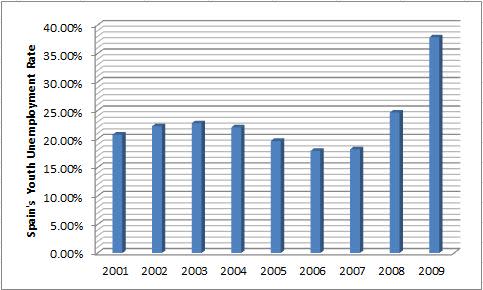

One reason unemployment rates are so incredibly high is the rising rates among youth. If you thought 1 in 4 people out of work was terrible, then don't fall over when I point out that 37.85% of all 15-to-24-year-old eligible workers were unemployed in 2009. Youth unemployment more than doubled from 2007 to 2009, and that rate has only continued to climb. According to the U.K.'s Telegraph, youth unemployment stood at a mind-numbing 50.5% as of April 2012.

Source: TradingEconomics. Note: No reliable data was found after 2009.

There are multiple factors built into Spain's economy that cultivate such high levels of unemployment. First, the wage structure in Spain is extremely rigid, which caters to older and more tenured workers. But, more important, a good portion of Spain's jobs are listed as temporary, which caps worker productivity and makes the firing of workers in that country a normal practice.

The other half of this story relates to Spain's reliance on the housing market to drive growth. Without question, I'd place the housing bubble bursting front-and-center in Spain's woes -- and that's a problem for a rapidly contracting sector that accounted for nearly 1 in 7 jobs at its peak. With the homebuilding sector contracting from 13% to less than 9% of the workforce, it's not surprising to see unemployment rates spiking.

The demise of Spain's only growth engine: housing

Between 1990 and 2011, housing provided the best return on investment for Spanish investors, so it wasn't surprising to discover that they put a significant amount of their wealth into their homes. What did shock me was just how much wealth Spaniards tied up in their homes relative to residents of other developed nations.

Source: Oliver Wyman.

As you can see, Spanish homeowners have tied 79% of their wealth into their homes. That's a dangerous proposition considering that home prices are falling (rapidly), and the amount of potential homebuyers is drying up as the unemployment rate rises. People nearing retirement age who are expecting the sale of their home to finance their remaining years may be in for the unfortunate surprise that they didn't net nearly enough from their home to cover their retirement.

But poor allocation of wealth by Spain's savers is just half of the problem. The bottom line is that Spain's homebuilders didn't really think things through.

From a homebuilding perspective, even during the peak, homebuilders in the United States were only building one home per every 2.5 people. That's a lot, but it was reasonable at the time considering the more than 2.1 million homes being sold. Spanish homebuilders, on the other hand, were building at a rate of one home for every person from 1992 through 2010! I feel as if anyone with half a brain should have seen that this was a poor idea that was simply unsustainable -- but alas, no one did.

A more interesting correlation is that of wages and housing price. From 1995 through 2000, Spanish wages and home prices increased at similar levels, which made Spain's housing growth somehow sustainable. But since then, the difference between workers' wages and home prices has grown disproportionately and unsustainably large. At their peak in 2008, Spanish home prices had more than tripled from their 1995 levels, with wages at the time up by only 70%. This divergence just didn't make sense. Although home prices have fallen about 20% from their peak, they would need to dive another 30% just to be in line with Spanish wage growth!

An even worse decision by Spain's banks

If one person per house seems like a ridiculous idea, then be prepared to be amazed even more by how willing Spanish banks like Banco Santander (NYS: STD) and Banco Bilbao Vizcaya Argentaria (NYS: BBVA) were to lend money to the booming real estate market.

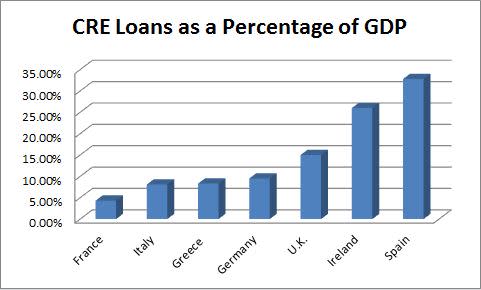

According to research from Morgan Stanley, of the 1.5 trillion euro lent to commercial real estate developers in Europe, Spain alone accounts for more than 20%!

Source: Morgan Stanley Research.

348 billion euro in CRE exposure may not seem like much, but allow me to translate these figures into CRE exposure as a percentage of national GDP, and you'll see why this is such a huge concern.

Sources: TradingEconomics and author's calculations. Assumes euro-dollar conversion of 1 euro to $1.3259.

I was a little surprised to see that U.K.'s banks had lent so much, but the U.K. is also a remarkably healthy and strong economy in comparison to Spain. As you can see, at 32.8%, Spanish banks have lent nearly one-third of Spain's GDP to commercial real estate developers. That's a problem considering that my research in September showed that 125 billion euro of outstanding CRE loans are being placed in the doubtful category with regards to collection. The Bank of Spain, the overseeing body equivalent to the United States' Federal Reserve, noted in March that questionable construction debt could actually be as high as 176 billion euro. It's one thing when a bank absorbs a one-time cost; it's completely different when the nation's top banks could be forced to absorb losses equaling 10% or higher of Spain's annual GDP!

Foolish roundup

Spain is in a quickening death spiral. Austerity measures designed to reduce government spending will only aggravate unemployment figures further, which, in turn, could worsen housing prices that subsequently impact the nation's banks and those nearing retirement. If Spain chooses to do nothing, the interest payments on what it already owes will become too difficult to manage.

Simply put, there is no fail-safe solution and no white knight in this situation -- just the reality that the Spanish government, the homebuilders, and the banks have created a big mess that will require the collective funds of the world to help them get out of.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy that's powered by transparency.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.