I'm Buying This Disruptive Innovator

Last week I introduced five companies I was considering adding to my Roth IRA. Today I'm letting you know which one I'm picking and why.

But to help you better understand how I went about choosing my winner for this month, I want to introduce you to a graph that could supercharge your own portfolio. Below, I'll explain how disruptive innovators work, and at the end I'll offer you access to a special free report on three companies our analysts think will help you retire rich.

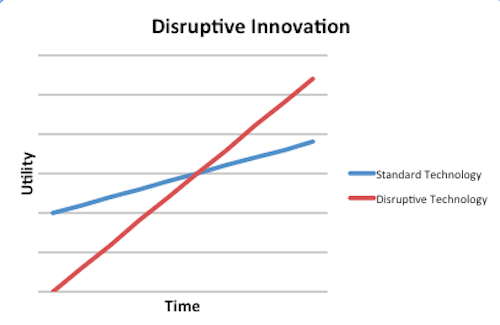

Source: Author, based on The Innovator's Dilemma by Clayton Christensen.

The graph above is my own visual representation of an idea I learned about in Clayton Christensen's The Innovator's Dilemma, which shows how new products designed by relatively small companies eventually usurp standard products designed by large corporations. Of equal importance, disruptive technology generally becomes cheaper as time goes on, while standard technology usually maintains steady price points.

Typewriter, meet desktop

For a simplistic example, consider the typewriter (blue line) and the desktop computer (red line). Back in the 1960s, the typewriter was far more practical for the average office worker. Computers were enormous, expensive, and unwieldy for the average person to use. Its size, cost, and ease of use made the typewriter the obvious choice for businesses.

But fast-forward to today, and the story has changed. The desktop computer, with its dizzying array of executable functions, is now the slam-dunk choice. Over time, its ease of use, size, and price all became much more attractive.

An investment in the right computer firm in the 1960s would have been wildly successful. But it's important to note that not every disruptive innovator has the ability to make it all the way through the graph. Competition and acquisition can play huge roles in thwarting the innovative company, as can the possibility of being disrupted by yet another innovator.

I want to buy a company that is at the intersection of the blue and red lines. Though it may not yield sky-high returns over the long run, by focusing on a company whose technology is starting to outshine the competition, I think I'll be getting a safer bet with outsize returns.

The process of elimination

Of my choices from last week, I can eliminate Westport Innovations (NAS: WPRT) and Solazyme (NAS: SZYM) right off the bat. Westport is surely an innovative company, pioneering the design of tomorrow's natural-gas engines. But if you think about it, it doesn't exactly match the disruptive archetype. Yes, its engines are new on the scene -- and they'll likely improve over time -- but it's not the technology alone that gives the company so much potential. The availability of cheap natural gas plays a huge role as well. Take that variable away, and Westport would be in trouble.

With Solazyme, which can make tailored oils from patented microalgae, it's much the same story. The company is certainly innovative -- and it will likely continue to tweak its algae -- but it doesn't fit the archetype. The key for this company is not necessarily out-innovating traditional oil companies, but simply scaling up production so that its oils become cheaper.

Two that just missed the cut

When it comes to 3-D printing, the technology isn't quite at the point of utility I'd like to see quite yet. Without a doubt, Stratasys (NAS: SSYS) and 3D Systems (NYS: DDD) are both high-quality companies that could produce monster returns for shareholders.

But the companies aren't quite at the stage of adoption or utility where I can see them replacing the standard manufacturing infrastructure we have in place today. If my criteria for this search were different, or if we could fast-forward 10 years into the future, either of these companies would be the perfect choice.

My pick for the month

That leaves us with my pick for the month: IPG Photonics (NAS: IPGP) . The company is a vertically integrated manufacturer of fiber-optic lasers. These lasers are most popular in the welding of large sheets of metal for industrial purposes, but they are gaining headway in other industries as well.

As opposed to standard carbon-based lasers (the blue line), fiber-optic lasers have been making huge leaps in strength over the past few decades. IPG's lasers are typically far less costly for its customers as well, both in their asking price and the amount of energy necessary to run them.

I see IPG's lasers standing at the intersection of the blue and red lines on my graph, and I see no reason to believe the company won't dominate its field in the decade to come. Surely economic slowdowns will hurt the company, as they will any company that relies heavily on industrial customers. But with every cycle, I believe IPG will gain more and more market share.

Worried about retirement

Obviously, I think having a disruptive innovator in my retirement portfolio is a good idea. But as I said above, not every potential innovator reaches the big league. It's important to balance your portfolio with both small up-and-comers and mature, established businesses with wide moats protecting them.

We've created a special free report on such companies: "3 Stocks That Will Help You Retire Rich." Inside, you'll get the names and details of three companies we believe deserve consideration in any investor's portfolio. Get your copy of the report today, absolutely free!

At the time thisarticle was published Fool contributorBrian Stoffelowns shares of all the companies mentioned except for 3D Systems. You can follow him on Twitter, where he goes byTMFStoffel.The Motley Fool owns shares of Solazyme, 3D Systems, Westport Innovations, and IPG Photonics.Motley Fool newsletter serviceshave recommended buying shares of 3D Systems, Westport Innovations, Stratasys, and IPG Photonics. The Motley Fool has adisclosure policy.We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.