How Long Can Amazon.com Defy Gravity?

Amazon.com (NAS: AMZN) continues to amaze me. Not because, as a company, it continues to sell more and more of everything with each passing quarter. That should be expected when you're the de facto Internet sales portal for much of the Western world. No, I was stunned -- flabbergasted, even -- at the market's reaction to declining profit margins, so much so that I've decided to open a bearish CAPScall today on the stock in Motley Fool CAPS.

It could be that the online retail giant handily trounced its lowballed guidance. But coming through the first-quarter finish line with $130 million in net income was good enough for a profit margin that only broke 1% when rounded up. That shrinking bottom line was good enough for Friday's buyers, who gobbled up Amazon stock to the tune of as much as a 17% gain. For years, buyers have ignored Amazon's low, low margins and bought it at high, high valuations. Now that margins are dwindling, the stock is as expensive as ever. I'm not here to argue that the P/E ratio should be your only consideration -- but shouldn't margins matter?

You'll be on a rocket ride to the moon

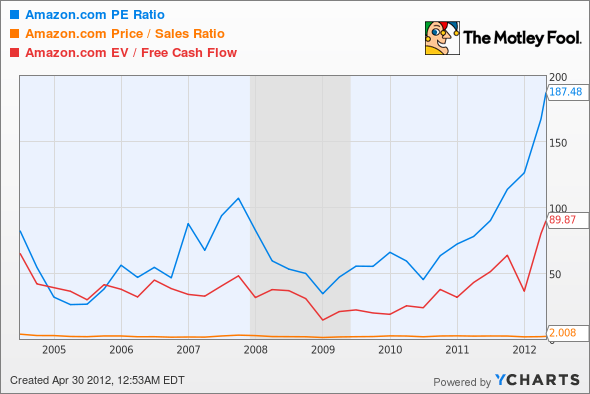

If Amazon's stock was highly valued before, it's getting a bit silly now, as the stock is at its richest valuation in nearly its entire profitable history. Its forward P/E is nudging up against triple digits. Other metrics have gone similarly stratospheric. One key indicator, the price-to-sales ratio, has remained roughly the same:

AMZN P/E Ratio data by YCharts

That might make sense if you're investing in a young start-up blazing a new trail, but Amazon's almost old enough to vote. Its efforts are well known and its success can be estimated to a nearer degree than one might get from that start-up. Whether it's the number of Kindle Fires sold or the revenue those tablets might generate, there are more than enough opportunities for investors to crunch all kinds of Amazon numbers. When those numbers seem lacking, it's worth asking what investors are after, and whether expectations have lost sight of reality.

That moon money is mine!

One common thread seems to underlie most bullish Amazon sentiment. It's a transformational company. Its opportunities are limitless. It's changing everything and it has a bull's-eye on everyone. Being in the sweet spot of online retailing -- and claiming all the ancillary opportunities that come with it -- should offer Amazon the prospect of vastly greater income in the future.

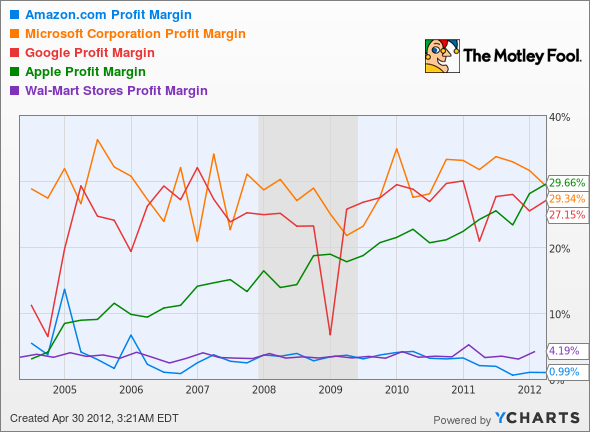

But here's the thing. Most of the transformational companies that have come along have tended to make money more effectively than their peers. Microsoft's (NAS: MSFT) margin has long been enviable. So are Apple's (NAS: AAPL) and Google's (NAS: GOOG) . Heck, even Wal-Mart (NYS: WMT) has matched or beaten Amazon's profit margin for much of its history:

AMZN Profit Margin data by YCharts

Outside of an early margin spike to close out 2004 -- aided in part by a substantial tax credit -- Amazon's earnings, when viewed through a more complete prism that includes free cash flow and capital expenditures, only appeared to be approaching its impressive top-line growth at the end of 2009:

AMZN Free Cash Flow TTM data by YCharts

Gravity hurts

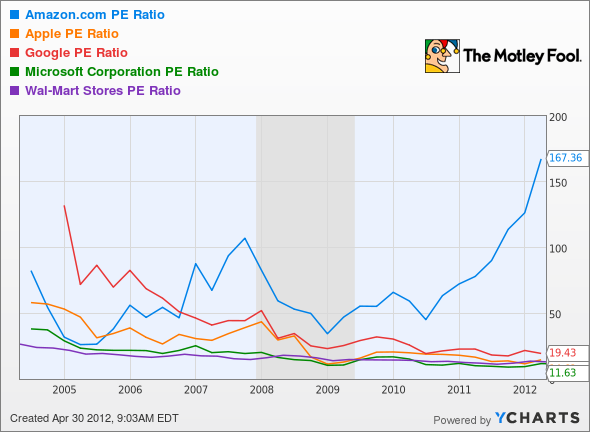

I mentioned in the beginning that P/E shouldn't be your only consideration. However, it does allow us to roughly size up where Amazon is against its high-tech peers, those other companies that have helped transform the way we live. By that measure, Amazon's not just expensive; it looks downright bubbly:

AMZN P/E Ratio data by YCharts

I didn't want to be unfair to Amazon, so I looked at each company's history to find when their absolute highest P/E occurred. The results don't put Amazon's current price in a much better perspective.

Company | Highest P/E Recorded | Date Recorded |

|---|---|---|

Microsoft | 72.6 | Dec. 27, 1999 |

107.5 | Feb. 3, 2005 | |

Apple | 305.4 | Feb. 18, 2003 |

Walmart | 59.6 | Dec. 28, 1999 |

Source: Wolfram Alpha.

Microsoft and Wal-Mart both topped out at the height of the dotcom bubble, while Apple had a few profitability problems in the years immediately following Steve Jobs' return. Google's highest P/E came shortly after its IPO and has been trending downward ever since. Only Amazon has (to date) resisted that old idiom, "What goes up must come down."

Amazon's highest P/E came when it first exited unprofitability, but its current P/E is higher than at any point besides that one. Either investors now expect impressive profit growth in the near future or the stock suffers from some irrational exuberance. When Amazon's CEO goes on record as preferring to grab more customers even if it means lower margins, it seems that the latter case is more likely. No single addition to Amazon's expanding range of businesses, whether cloud offerings, commercial supply sales, or Amazon Prime, can make up for low margins in the company's core businesses, especially if those businesses are themselves rather low-margin to begin with.

In fact, Prime may be a major contributor to the company's declining margin, as it effectively locks consumers into a single yearly payment for shipping costs that have been increasing recently, no doubt thanks to higher fuel expenses for shipping companies. If you have free shipping, you're more likely to order small items with greater frequency, which turns out to be a great benefit to you but a lousy bargain for Amazon. Add in the costs of acquiring and streaming video content for Prime members, and the royalty payments made to authors whenever a Prime member borrows an e-book for free (imagine if your local library had to do that every time you checked something out), and you can see why drawing more users into the service could further erode Amazon's profitability.

Can Amazon ever justify its high price? Does it now? These are questions to ask the market as it pushes Amazon's multiples to new heights. Everything that goes up comes down eventually. If you're looking for a safer alternative with similarly compelling growth arguments, The Motley Fool's top stock for 2012 offers the right mix of sane valuation and substantial growth. Find out more about this opportunity in our free report -- claim your copy while it lasts.

At the time thisarticle was published Fool contributorAlex Planesholds no financial position in any company mentioned here. Add him onGoogle+or follow him on Twitter@TMFBigglesfor more news and insights. The Motley Fool owns shares of Amazon.com, Google, Microsoft, and Apple.Motley Fool newsletter serviceshave recommended buying shares of Apple, Amazon.com, Google, and Microsoft, creating bull call spread positions in Apple and Microsoft, and creating a diagonal call position in Wal-Mart Stores. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.