Green Mountain Comes to a Crossroads

There's no way to be sure which direction the market will go, but that's no reason to hit the panic button. A long-term horizon is still the best path to success -- but not every stock deserves a long-term place in your portfolio. It's important to examine all angles of your favorite stocks to find out how far you should go with them. With that in mind, let's look at Green Mountain Coffee Roasters (NAS: GMCR) , which has fallen on hard times over the past year, to find out if it's poised to recover or if it's about to have its last caffeine crash.

Caffeine crash

It's been pretty easy to find soaring stocks this year, but hard-luck companies aren't quite so common -- at least not the kind we want to find. Since Green Mountain's grown so rapidly (despite its drop over the past year), I wanted to see if its pace is sustainable, and one way to find out is to get a quick snapshot of the company's recently reported information.

Metric | Trailing-12-Month (or Most Recent) Result |

|---|---|

Annual Revenue | $3.24 billion |

Annual Net Income | $302 million |

Profit Margin | 9.3% |

Annual Free Cash Flow | ($252 million) |

Market Cap | $7.6 billion |

Price to Earnings Ratio | 25.2 |

12-Month Stock Price Decline | (27%) |

Coffee Sold (Fiscal 2011) | 136 million pounds |

Sources: Yahoo! Finance, Morningstar, Google Finance, and corporate 10-K filing.

Percolating profits but poor cash flow

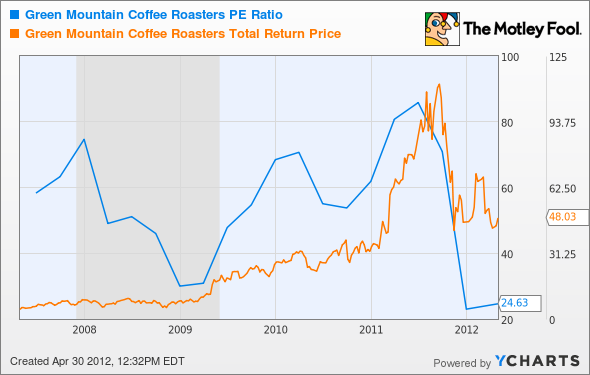

Green Mountain's recent drop came from a dizzying height, and shares are still up nearly 1000% in the past five years. However, with its recent decline comes an affordability never seen before, as the company's P/E continues to hover near historic lows:

GMCR P/E Ratio data by YCharts

Worries have swirled since the fall plunge, when David Einhorn pulled off a perfectly timed short built on patent expirations and accounting concerns. Other bears came out of hibernation to take a swipe at the K-Cup brewer's apparent discounting efforts and shipment declines. Despite these concerns, Green Mountain's big numbers kept getting bigger -- all except one:

GMCR Profit Margin data by YCharts

Free cash flow has been negative since 2007, with the bleed turning into a gusher last year. However, negative free cash flow need not necessarily make for a bad company. My fellow Fool Ilan Moscovitz points out that despite a widening gulf between profit and cash flow, Green Mountain could simply be ramping up its inventory and capital spending. Good news if the K-Cups fly off the shelves, but not so much if it starts piling up at discount retailers.

Patently dangerous?

Patent woes are a big problem for Green Mountain, which will see important patents expire this year. In response, the company's rolled out a new brewing platform to maintain control over its preciously proprietary ideas. The big question is whether or not even this new brewer can fend off Starbucks' (NAS: SBUX) recent high-pressure home-brewing entry, dubbed Verismo. While Starbucks has continued to vocally support Green Mountain's K-Cups, its brand appeal alone could erode the Keurig's market share as caffeinated consumers rush after the new hotness.

Still, brand appeal remains one of Green Mountain's strong suits, as both Dunkin' Brands (NAS: DNKN) and Starbucks will offer branded K-Cup products in their stores by the end of the year (Dunkin' already does). As long as strong brands continue to support the platform, Green Mountain can continue to hide behind its shallow moat. Maintaining an in-store presence at Bed Bath & Beyond (NAS: BBBY) and other quality retailers will also help, but the Keurig system alone can't carry the company. A steady stream of K-Cup purchases will be necessary to keep the top and bottom lines growing.

Foolish final thoughts

Green Mountain is a company facing significant headwinds in the year ahead, but it's also a company that's invested significantly in building its brand. Whether or not that brand matters -- or if it can hold up against the Starbucks Verismo salvo -- will be the defining issue for this stock going forward. Both bull and bear cases have merits, but the ultimate arbiters of Green Mountain's success will be its caffeinated consumers. Pay extra-close attention to any Keurig consumer commentary you see in months ahead. It could be the difference between a stock that keeps growing and one that suffers a crash no amount of coffee can cure.

If you're worried that Green Mountain's multibagger days are behind it, you should take a look at The Motley Fool's latest free report on the next big multibagger. There are plenty of opportunities for explosive growth in this market, and we've got the inside scoop on one stock that's poised to soar. Find out everything you need to know -- click here to claim your free report now.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool owns shares of Starbucks. Motley Fool newsletter services have recommended buying shares of Bed Bath & Beyond, Starbucks, and Green Mountain Coffee Roasters. Motley Fool newsletter services have recommended creating a lurking gator position in Green Mountain Coffee Roasters. Motley Fool newsletter services have recommended writing covered calls on Starbucks. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.