Why Zynga's Earnings Beat Is Still Disappointing

Looks as if social gamer Zynga (NAS: ZNGA) is 2-for-2 with disappointing earnings releases.

Shares lost 18% following last quarter's Valentine's Day report, which was its first ever as a public company. The stock finished down more than 9% today, after Zynga reported first-quarter results last night. How bad could it be?

Growth? Check.

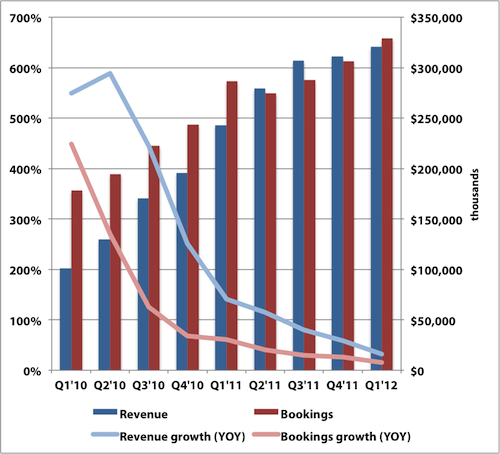

Revenue rose 32% to $321 million, while bookings increased 15% to hit an all-time record of $329.2 million. Non-GAAP net income was $47 million, or $0.06 per share. Those results are ahead of what the Street was looking for, as consensus estimates called for $317.7 million up top and a nickel down below.

On a GAAP basis, Zynga actually lost $85.4 million, or $0.12 per share, again thanks to generous stock-based compensation expenses that it excludes from its adjusted figures.

User activity continued to show improvements, with monthly active users, or MAUs, popping by 24% to 292 million. Daily active users, or DAUs, inched higher by just 6% to 65 million.

Deceleration? Check.

On the surface, all of those metrics sound promising, with growth across the board. But here's what's so troubling about Zynga.

Sources: SEC filings, earnings press releases.

That's massively decelerating growth you're looking at in both revenue and bookings. Growth naturally decelerates as a company's revenue base gets larger, but at the same time we're also talking about a company that's valued at $6.8 billion, which translates into about 5.7 times trailing-12-month sales of $1.2 billion.

GAAP net income also plunged as it swung to a net loss, compared with the $16.8 million profit a year ago. At current prices, investors are clearly expecting a lot from Zynga, and it can't live up to those hopes right now.

Toss in the fact that Zynga just completed a secondary offering earlier this month, and there are now 49.4 million more shares floating around out there to go around, so it should take a lot more buying demand to move the price up. The offering was primarily to facilitate an orderly exit for early backers, as Zynga wasn't actually raising any capital and didn't receive any proceeds from the deal.

The good news

There are some positive aspects to the report, though, specifically looking at its bookings figure, which is probably the most important metric I had my eye on. Bookings is a precursor for revenue, so that figure needs to continue marching higher if Zynga hopes for revenue to follow.

You'll notice in that earlier chart that for the previous three quarters, bookings came in lower than revenue, which meant the pipeline was drying up. Seeing Zynga's bookings this quarter now standing higher than revenue (at an all-time record, no less) is a positive sign for future prospects, despite the fact that it's seeing slowing growth.

That bookings growth is expensive

The flip side of that coin is that bookings growth is now being driven primarily from mobile platforms, as the company has been acquisitively pushing into Apple (NAS: AAPL) iOS and Google (NAS: GOOG) Android with a vengeance. That means its core Web bookings are slowing faster than expected.

It's certainly good to wean itself from its overreliance on Facebook, but it's now shifting that reliance to acquisitive mobile growth. Zynga's $180 million acquisition of OMGPOP scored it a spot on the top charts, although Draw Something's appeal is starting to fade. The title has fallen to the No. 4 paid spot in the iOS charts, although it is still No.1 in Google Play.

That's a ton of money for a one-hit wonder, and Zynga's goodwill and intangibles have soared over the past three months. At the end of last year, goodwill and intangibles totaled $123.9 million, or 5% of total assets; that figure has now nearly tripled to $339.2 million or 13% of total assets. As the largest deal over that timeframe, chances are that OMGPOP contributed a hefty chunk of that jump.

This trend is set to continue. A couple weeks ago, CEO Mark Pincus told Bloomberg that Zynga will probably do a "few" more deals of this magnitude in the coming years, although last night he called the OMGPOP acquisition a "rare instance."

Questionable acquisitions are not good for your health

Pursuing growth through acquisitions is a tricky strategy. Just ask Ebix (NAS: EBIX) , which continues to snap up smaller players in the insurance exchange market, or Nuance Communications (NAS: NUAN) , which does the same in the speech recognition and transcription sectors. It can certainly pay off when done properly, but it presents unique risks with writedowns and impairments if integration doesn't go well or if the company overpays.

I definitely think that Zynga overpaid for OMGPOP, since I have doubts about Draw Something's ability to become a sustainable franchise. If Zynga doesn't execute is acquisition strategy well, that's a lot of goodwill to eat, which always causes indigestion.

Zynga is a Faker Breaker, which doesn't bode well for its chance of delivering multibagger returns. That's something that Rule Breakers excel at, so Discover the Next Rule-Breaking Multibagger by checking out this special free report. It's free.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Apple and Nuance Communications, but he holds no other position in any company mentioned. Check out hisholdings and a short bio. The Motley Fool owns shares of Google and Apple.Motley Fool newsletter serviceshave recommended buying shares of Nuance Communications, Google, Ebix, and Apple and creating a bull call spread position in Apple. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.