52-Week-High Alert: Polaris Industries

Shares of Polaris Industries (NYS: PII) hit a 52-week high yesterday. Let's look at how it got here and whether clear skies are ahead.

How it got here

You would think that a rough economy would have a negative impact on expensive toys but it's been exactly the opposite in the ATV, motorcycle, and utility vehicle business. A week after Arctic Cat (NAS: ACAT) hit a new 52-week high, Polaris followed suit with a new high of its own.

The most recent quarterly report was the latest driver of the stock and showed just how strong the company has been performing. Off-road vehicle sales increased 30% and on-road vehicle sales grew 44% in the first quarter, driven by a 17% increase in North American sales. The company reported earnings-per-share growth of 27%, to $0.85 per share, and increased its full-year earnings guidance to $3.85-$4.00 per share.

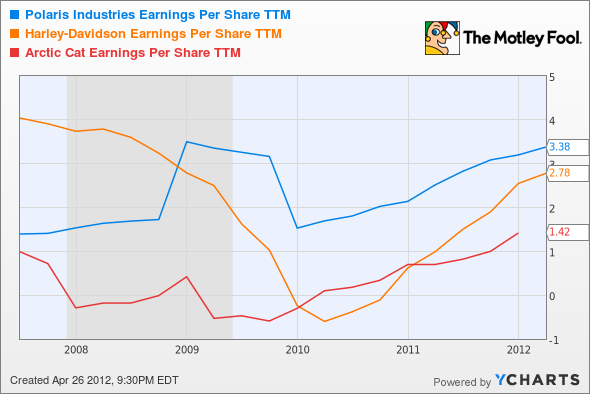

Compared to its closest competitors, Polaris has navigated the recession and the ensuing recovery well. Polaris didn't have nearly the dip in earnings that Harley-Davidson (NYS: HOG) did and has kept pace with Arctic Cat's earnings recovery.

PII Earnings Per Share TTM data by YCharts

A warm winter may have helped push up sales of on- and off-road vehicles into the first quarter this year, and surprisingly it didn't have much of a negative impact on snowmobile sales. Snowmobile retail sales were down just 5% in the winter season, so the downside of the warm winter wasn't really felt by Polaris.

What's next?

The big question for Polaris is: Can the good times last?

I don't see a reason Polaris can't keep growing, since we're really just at the leading edge of an economic recovery in the U.S. and Europe's economy remains weak. As I stated above, North American sales were strong and international sales grew 20% over last year.

I also like the strategic addition of Indian Motorcycles in the last year. It adds some cache to Polaris' line and provides more diversification for the company.

With all of that said, I'm worried about the valuation that the stock is trading at right now. Even if the company hits the top end of its guidance for 2012, the stock is trading at 20 times 2012 earnings. That type of valuation will keep me from buying right now, although if the stock pulls back 10% to 20% I could see a decent value and a good dividend-paying investment.

Interested in reading more about Polaris Industries? Click here to add it to My Watchlist, which will find all of our Foolish analysis on this stock.

At the time thisarticle was published Fool contributorTravis Hoiumdoes not have a position in any company mentioned. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.Motley Fool newsletter services have recommended buying shares of Polaris Industries. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.