Analyst Debate: Is SunPower's Stock Rising or Setting?

The Motley Fool has been making successful stock picks for many years, but we don't always agree on what a great stock looks like. That's what makes us "Motley," and it's one of our core values. We can disagree respectfully, as we often do. Investors do better when they share their knowledge.

In that spirit, we three Fools have banded together to find the market's best and worst stocks, which we'll rate on The Motley Fool's CAPS system as outperformers or underperformers. We'll be accountable for every pick based on the sum of our knowledge and the balance of our decisions. Today we'll discuss SunPower (NAS: SPWR) , a vertically integrated solar company.

SunPower by the numbers

SunPower is one of the leading solar manufacturers and owns nearly the entire supply chain for its products. The company makes the highest-efficiency modules in the industry -- its main competitive advantage in an industry that is in the midst of a shakeout. Here's a quick snapshot of the company's most important numbers:

Statistic | Result (most recent available) |

|---|---|

2011 revenue | $2.3 billion |

2011 net income | ($603.9 million) |

Gross margin (most recent quarter) | 7.9% |

Market cap | $644 million |

2011 MW produced | 922 |

Key competitors | First Solar (NAS: FSRL) Suntech Power (NYS: STP) JA Solar (NAS: JASO) Trina Solar (NYS: TSL) |

Sources: Yahoo! Finance; company filings.

But will SunPower outperform the market over time? Here are our opinions.

Travis' take

The shakeout going on in the solar industry has scared a lot of investors away -- and rightfully so. Once-promising companies like Energy Conversion Devices, Q-Cells, and Evergreen Solar are among those that have bitten the dust, and the companies that remain are posting big losses and hoping for brighter days. First Solar, once the golden child of solar, has been a poster child of the struggle, battling both increased competition from China and a plunging stock price.

What's important to look at right now is who will emerge from the industry after the current consolidation cycle is complete. One big point in SunPower's favor is the backing of oil giant Total, giving it not only financing, but also a research-and-development partner. As the efficiency leader, SunPower has some catching up to do in per-watt cost, but the trajectory is in the right direction. The company ended 2011 with cost per watt at $1.46, down 18% from the year before, and costs are expected to fall another 14% this year. These costs aren't as low as Chinese competitors', but on an efficiency-adjusted basis, SunPower should catch -- and pass -- some rivals by the end of this year.

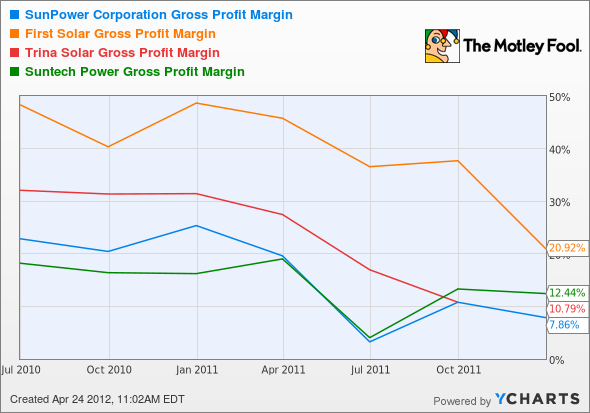

The proxy I am watching most closely is gross margin, which should tell us if SunPower is staying competitive in the market. The company is hanging in with the gross margins of Chinese competitors like Suntech and Trina Solar right now, as you can see below, and hasn't seen the steep drop First Solar saw recently. If margins stabilize (which they seem to be doing) and begin slowly increasing, we should start to see profitability return to the industry.

Source: YCharts. Note: Suntech's gross margin declined to 9.9% in Q4, and Trina Solar's gross margin was 7.1% in Q4.

The major risks for SunPower are national policy and subsidized Chinese competitors. Solar power has suffered from major cuts in the U.S., Germany, and other European countries as budget crunches put pressure on policymakers. There isn't much left to cut, but the transition to a sustainable market will take some time. At the same time, China has been handing out billions of dollars in financing to its manufacturers, forcing companies like SunPower to compete in an oversupplied market. If this continues indefinitely, more companies will fail, and there's a chance that SunPower could board that sinking ship.

With all of the risks considered, I think SunPower is the best bet in solar, an industry I believe has a bright future. The stock is trading at 0.6 time its book value and just 0.2 time sales, so if the company can get back to profitability, this could be a multibagger in the making. But this isn't a stock for the faint of heart. I have a five-year time horizon on this pick, and there could be big short-term swings in the stock price. For a more detailed analysis, check out why SunPower was my top energy stock of 2012.

Alex's take

When I look at solar companies, I try not to think only in terms of panel efficiency and cost per watt, although these are both important considerations in a rapidly advancing industry. Rather, I like to look at their potential to create, adapt, or overcome the disruptive innovations that often crop up in the solar sector, as well as broader technological trends that can make solar energy more reliable. If it's not a more efficient panel, it's light-sensitive plastics or spray-on solar cells that might be easily attached to common objects at low cost. Researchers are also looking for ways to effectively store solar energy when it's not being produced and have developed tinted windows to capture the sun's rays.

Anyone who has followed technology trends understands that major breakthroughs can occur with frightening rapidity and have unexpected consequences. To date, most commercial-scale solar advancements have been in panel efficiency, with little commercialization of the many unorthodox ideas being tweaked in labs. Many that have made it past testing are either panel-based, ultimately inefficient, or both, as Solyndra's cylindrical collectors proved last year.

As long as panels remain king and SunPower remains king of panel efficiency, it retains a vital competitive advantage in an essentially commoditized industry. Should non-panel solutions somehow capture market interest, SunPower would need to address the issue quickly to avoid losing major ground. Vertical integration and a history of industry-leading efficiency are both positive corporate traits to wield against new challenges, as are Total's deep pockets. A new technology might be acquired, rather than battled, fortifying the company's defenses against challengers.

I've already predicted that solar-power gains will be matched with vastly improved energy-storage technology within the next five years to really jump-start mass adoption. At just 0.1% (yes, that's a tenth of a percent) of America's total energy consumption, solar energy has a long way to go to replace fossil fuels, but that just means there's far more room for growth than many give the industry credit for.

I'm wary of currently traded solar companies in general, with their reliance on government subsidies and difficulty competing with other energy sources on cost. I do believe solar power has staying power, and the progress of its technologies will render subsidies unnecessary -- and its energy more than cost-competitive. The companies that can make good on this promise have SunPower's traits, and since there's no other company with that mixture of good stuff, SunPower is it. I wouldn't expect huge gains for the near future, but a longer timeline should reward the (very) patient investor.

Sean's take

After recently writing an article about five green stocks that could energize your portfolio for Earth Day, I purposely left solar stocks off that list because of falling average selling prices and rampant oversupply throughout the industry. First Solar is struggling with a drop in German solar subsidies, while many U.S.-based solar companies just like SunPower are having difficulty matching the low-cost structure of Chinese solar-panel manufacturers.

But as Travis mentioned, SunPower has the unique advantage of being the U.S. solar efficiency leader, as it's a vertically integrated company. Because it can internalize its entire manufacturing process, the company is targeting a 15% reduction in total processes by the end of fiscal 2012, which should reduce overall costs to just $0.86 per watt. I'm not fully certain this will be enough to return SunPower to profitability, but it's far and away better than the majority of its peers.

The backing of Total also makes SunPower an intriguing play. As I've touched on before, I feel one-quarter of publicly traded solar companies could go bankrupt before supply is back in line with demand. Total provides SunPower with guaranteed financial backing, which allows it to focus solely on garnering contracts.

There's no denying that, at 49% of book value, SunPower is an intriguing value play. Although it's likely average selling prices of solar panels will fall further, and government subsidies will be difficult to come by (especially internationally) over the next few years, I see good long-term potential in SunPower. If you are looking to buy a solar company and forget about it for a decade, SunPower is your company.

The final call

So we all agree (surprise!) that SunPower is a long-term buy, but you may want to turn your tickers off for the next few years. We'll add an outperform rating to our TMFYoungGuns CAPS page to track our pick against the market. The sample size is small, but so far our picks are four-for-four and beating the market by a total of 40 points.

At the time thisarticle was published Fool contributor Travis Hoium owns shares of SunPower in both a personal and a managed account. Fool contributors Alex Planes and Sean Williams do not have positions in any companies mentioned. You can follow Travis on Twitter at@FlushDrawFool, Sean at@TMFUltraLong, and Alex at@TMFBiggles.Motley Fool newsletter serviceshave recommended buying shares of Total and First Solar. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.