Where Does the Market Go From Here?

Are we in a bull market or a bear market? That depends on who you ask, but it also depends heavily on the length of your timeline. There's been no shortage of overblown sentiment for both scenarios, including near-panic over a 4% "plunge" earlier this month. Bulls boasted all winter that we might well head to Dow (INDEX: ^DJI) 20,000, only to retreat in the spring as bears, both literal and financial, came out of hibernation.

Seem like a familiar script? The same situation played out in 2010 when the Dow peaked on April 23 and spent all summer struggling to regain its ground. April was again the cruelest month in 2011, when a strong rally to start the year topped out on April 29 and the Dow never fully recovered. Despite those gyrations, the index is still up nearly 16% from its 2010 springtime peak. That seems like good commentary on the value of patience.

But two years isn't much at all for truly patient long-term investors. Stretching out your time horizon helps change the way you examine bull markets and bear markets. If post-2009 conditions were broadly positive for stockholders, post-2000 returns remain underwhelming. Understanding these cycles of advance and retreat can help you be a better investor, and it also can help grant a more placid perspective in the midst of genuine market chaos -- a valuable trait indeed.

Have a little perspective

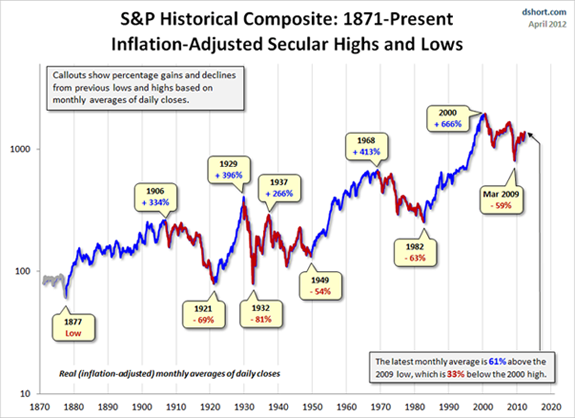

Although the Dow nosed past 14,000 in early 2007, that pre-crash peak is still only the highest all-time index value if you don't count the effects of inflation. When you bring inflation into the picture, things start to look a bit different, and the plight of dot-com investors looks a bit clearer:

Source: Doug Short, Advisor Perspectives.

Ready for a little vocab lesson? This is a great representation of the difference between a cyclical market, which is a smaller period of time -- like the growth phase of 2002 to 2007 -- within the longer secular market trend that eventually undid that growth. In secular bear eras, you can have multiple radical movements between shorter cyclical bull and bear markets, as demonstrated with particular violence during the Great Depression era. On the other hand, secular bull markets tend to mosey pretty consistently upward for long periods of time, taking two (or more) steps forward for every step back.

Sign of the times

Here's the $15 trillion question -- the same one from the start of this article: What kind of secular market are we in? You'd think it'd be easy to tell. Unfortunately, when we look back on three years of steady-to-spectacular growth, we still find ourselves staring uphill at an inflation-adjusted peak 33% higher than our current perch. There's no definitive way to say "the bull was born here" until markets finally advance past the previous high-water mark. That said, we can at least analyze the length and severity of past markets to find out where we stand in history, as a guide to the potential future.

Year | Milestone | Percentage Change | Years | Annualized Return | Annualized Total Return (dividends included) |

|---|---|---|---|---|---|

1921 | Low | (69%) | 14.9 | (7.5%) | (2.0%) |

1929 | High | 396% | 8.1 | 21.9% | 28.4% |

1932 | Low | (81%) | 2.7 | (44.9%) | (41.2%) |

1937 | High | 266% | 4.7 | 32.1% | 38.7% |

1949 | Low | (54%) | 12.3 | (6.2%) | (0.8%) |

1968 | High | 413% | 19.5 | 8.8% | 13.3% |

1982 | Low | (63%) | 13.6 | (7.0%) | (3.0%) |

2000 | High | 666% | 18.1 | 11.9% | 15.3% |

2009 | Low? | (59%) | 8.5 | (9.8%) | (8.1%) |

Now | N/A | 61% | 3.1 | N/A | N/A |

Source: Doug Short, Advisor Perspectives.

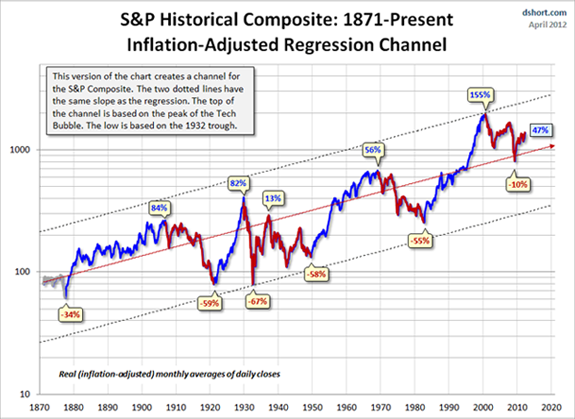

The numbers seem more positive than not at first glance, but they don't offer anything conclusive. If our latest bear era really ended in 2009, it would be the shortest secular bear market of modern memory. Not only that, but it'd make the latest bear market perhaps the least ferocious on record, as this next chart shows:

Source: Doug Short, Advisor Perspectives.

Protect your neck

It's again time for that $15 trillion question: What happens next? Either rough sailing's ahead, things really are different this time, or the starting point skews the results in ways that aren't relevant to modern markets. Take your pick. Nobody knows when the bull rush will start, or if it's already in motion. In my honest opinion, I believe there's light in the tunnel -- but it's still a bit faint.

It pays to be diversified in uncertain times with a well-rounded stock selection, incorporating both stable staples and bust-resistant growth rockets. Here are two of each that I believe can outperform the market's moves in years ahead:

Company | P/E | 5-Year Annualized Growth Rate |

|---|---|---|

Intel (NAS: INTC) | 11.7 | 7.6% |

Philip Morris (NYS: PM) | 18.1 | 20.0%* |

Monster Beverage (NAS: MNST) | 41.5 | 26.7% |

Life Technologies (NAS: LIFE) | 22.6 | 6.5% |

Source: Yahoo! Finance. Assumes reinvestment if dividend paid. *Uses four-year growth rate.

If you don't already have Intel in your portfolio, what are you waiting for? Intel is the closest thing the world may have to a computing utility provider, with a comfortable dividend to boot. There are many cloud computing companies floating around, but the common denominator is that all of them need hardware. Intel just happens to dominate the server processor market. Get ready for the Intel mobile beachhead this year, too. Intel's products are so integral to the modern connected economy it's almost like we're addicted...

Kind of like Philip Morris' customers. We're all well aware of the hazards of cigarettes. We're also free to choose our stocks based on any criteria we like. If you're looking for growth, consistency, and strong resistance to macroeconomic challenges, it's hard to do much better than a tobacco stock, particularly an international one with world-class brand recognition. Fewer regulatory challenges and a much more defensible payout ratio than its former parent are also worth noting.

Monster is the kind of amazing growth story investors should love. A small, scrappy company with strong brand loyalty built itself into the potential heir to the energy-drink throne, giving investors nearly five times the gains of those who bought Apple a decade ago. Monster's revenue growth has outpaced the broader energy drink market's growth for years, and the company's projected to get a major jolt to its earnings this year. Look past the high P/E of this stock to find an investment that's still got a lot of potential ahead.

Any company that can help solve the health care spending dilemma would be in a very lucrative position. Life Technologies, one of two key players in the genome sequencing hardware market, could very well be one of those companies. As I recently wrote, Life Tech could be on the leading edge of a genomics bubble that may be inflated by the tests becoming mass-market affordable. That bubble certainly hasn't swept Life Tech up yet, as its fairly ho-hum P/E masks already-strong growth rates. Sequencing the human genome was a massive $300 million undertaking a decade ago. It will soon be cost-competitive with blood testing. That will generate billions of tests worldwide each year, many of which are likely to run on Life Tech's Ion Torrent machines. That, my friends, is a growth market.

There are investment options no matter what lies ahead. If you worry that another bear is coming, you'll want to look for stable, dividend-paying powerhouses -- the sort The Motley Fool's done its research on, and which are available for our readers at no cost in our popular free report: "Secure Your Future With 9 Rock-Solid Dividend Stocks." Bulls in search of big growth can find an excellent buying opportunity with one rule-breaking multibagger that we think you should take a look at today. Get more information on this revolutionary company in our latest free report; just click here for more information.

At the time thisarticle was published Fool contributor Alex Planes holds no financial position in any company mentioned here. Add him on Google+ or follow him on Twitter @TMFBiggles for more news and insights. The Motley Fool owns shares of Intel and Apple. Motley Fool newsletter services have recommended buying shares of Monster Beverage, Philip Morris International, Apple, and Intel, as well as creating a bull call spread position in Apple. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.