How High Can Kimberly-Clark Fly?

Shares of Kimberly-Clark (NYS: KMB) hit a 52-week high today. Let's look at how it got here and whether clear skies are ahead.

How it got here

Diapers, tissues, feminine care, and health-care products are driving a surge in profits at Kimberly-Clark, and while these products may not be sexy, their returns are. In the first quarter of 2012, which was reported on Friday, the company's net income grew 33.7% and earnings per share reached $1.18.

Strong organic growth of 13% at K-C International helped drive organic growth to 6%, but first-quarter revenue growth was only 4%.

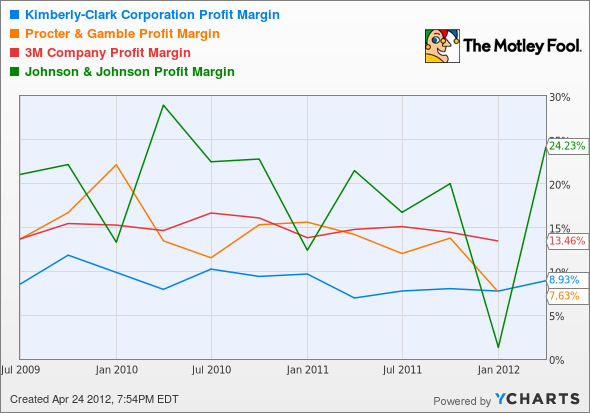

Kimberly-Clark trades in the middle of the pack of diversified consumer companies like Procter & Gamble (NYS: PG) , 3M (NYS: MMM) , and Johnson & Johnson (NYS: JNJ) . Revenue growth hasn't been behind Kimberly-Clark's rise this year -- rather, it's been improvement in margins and profitability.

KMB Profit Margin data by YCharts.

Kimberly-Clark probably won't catch up with 3M and Johnson & Johnson in the margin department, just based on the type of products it makes, but there is some remaining upside based on where margins were historically and the level that Procter & Gamble is able to command in the consumer business.

Kimberly-Clark | 9.3% | 4.2% | 5.3 | 14.2 |

Procter & Gamble | 7.3% | 3.7% | 2.9 | 15.6 |

3M | 12.5% | 5.7% | 3.9 | 12.8 |

Johnson & Johnson | 8.9% | (0.2%) | 3.0 | 11.7 |

Sources: Yahoo! Finance and Morningstar.

Slow and steady wins the race

A single-digit growth rate may not interest some investors, but Kimberly-Clark is in some businesses with strong brand recognition and markets that don't change suddenly. Cottonelle, Kleenex, Huggies, and Kotex are just some of the names that keep customers coming back, and they create a moat that is hard for competitors to get past. If the company continues to expand that moat overseas, it will help ward off competition as emerging markets begin to demand these kinds of products.

What's next?

I don't think there's anything that slows down the slow and steady progress Kimberly-Clark is making. The company's P/E ratio is at a reasonable level based on historical averages, a dividend yield of 3.8% makes the stock attractive to income investors, and a focus on emerging markets and cost-cutting should keep profits growing in the future.

The Motley Fool CAPS community has given Kimberly-Clark its highest rating of five stars, with All-Star players giving the stock 322 outperform calls versus eight underperform calls. I also think the stock can continue to outperform, especially in a market that will be concerned about the U.S. and European recoveries for some time.

For more stock picks that will make money instead of headlines, check out our report called "Secure Your Future With 9 Rock-Solid Dividend Stocks." The report is free when you click here.

At the time thisarticle was published Fool contributorTravis Hoiumdoes not have a position in any company mentioned. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.The Motley Fool owns shares of Johnson & Johnson.Motley Fool newsletter serviceshave recommended buying shares of Procter & Gamble, Johnson & Johnson, 3M, and Kimberly-Clark; and creating diagonal call positions in 3M and Johnson & Johnson. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.