AutoZone Cruises to a 52-Week High: Can It Motor Even Higher?

Shares of AutoZone (NYS: AZO) hit a 52-week high yesterday. Let's take a look at how the company got there and whether clear skies remain in the forecast.

How it got here

The path to AutoZone's success is paved with strong same-store sales growth and the ability to cater to the do-it-yourself car enthusiast. It's no surprise that we've seen earnings weakness from Pep Boys (NYS: PBY) , which relies heavily on service-center margins, while seeing strength from AutoZone.

But mixed in with AutoZone's success has been one huge sleight of hand that takes away from its outperformance. AutoZone has been regularly repurchasing shares for years, which has the effect of reducing the number of shares outstanding and boosting EPS (even if the company isn't growing much organically). This isn't to say that AutoZone isn't growing -- because it is -- but same-store growth across the sector has tapered in recent quarters, with O'Reilly Automotive (NAS: ORLY) , Advance Auto Parts (NYS: AAP) , and AutoZone all dropping significantly from their respective same-store sales growth levels of 11.5%, 9.9%, and 9.5% five quarters ago.

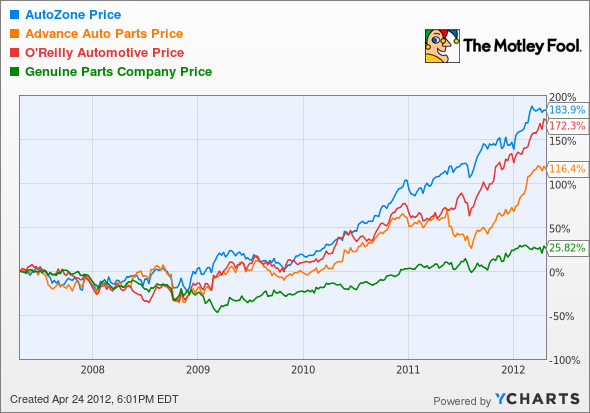

How it stacks up

Let's take a look at how AutoZone stacks up next to its peers.

For those of you (like me) waiting for an auto parts slowdown thanks to cars being built better and lasting longer, you can just keep waiting, according to these results.

Company | Price/Book | Price/Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

AutoZone | N/M | 12.0 | 14.0 | 6.3% |

Advance Auto Parts | 7.6 | 8.3 | 13.2 | 6.0% |

O'Reilly Automotive | 4.2 | 11.6 | 18.4 | 20.5% |

Genuine Parts (NYS: GPC) | 3.5 | 15.8 | 14.5 | 3.6% |

Source: Morningstar; author's calculations. CAGR = compound annual growth rate.

One thing that immediately stands out is that none of the companies in this sector offers compelling valuations. Genuine Parts, which is the most established company of this group and pays out a 3% yield, trades closest to book value but has also grown the slowest over the past five years. Another red flag is AutoZone's negative book value, which stems from the ever-growing debt pile that it uses to finance its operations. With $3.46 billion in debt and its debt load growing year over year, it seems unlikely that AutoZone will ever pay a dividend. I can't say I'm particularly enamored of any of the companies in the auto parts sector.

What's next

Now for the real question: What's next for AutoZone? The answer will depend on how the company plans to address its growing pile of debt and whether it can grow organically without the aid of share repurchases.

Our very own CAPS community gives the company a dreaded one-star rating (out of five), with 31.2% of members expecting it to underperform. As part of that 31.2%, my current CAPScall of underperform on AutoZone is down about 7 points since inception, and I'm not planning to close that pick anytime soon.

AutoZone has given shareholders the EPS growth they've wanted for the past few years, but it's done so without a single insider purchase (Eddie Lampert reduced his stake in the company yet again to 6.2% from 8.3% just two weeks ago), and with multiple share repurchases that artificially inflate profits. In addition, same-store sales growth is slowing and debt levels are rising to what I deem dangerous levels. The way I see it, there's little incentive to owning AutoZone at these levels.

Craving more input on AutoZone? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.