Imation Misses on the Top and Bottom Lines

Imation (NYS: IMN) reported earnings on April 24. Here are the numbers you need to know.

The 10-second takeaway

For the quarter ended March 31 (Q1), Imation missed estimates on revenues and missed expectations on earnings per share.

Compared to the prior-year quarter, revenue contracted and GAAP loss per share improved.

Gross margins improved, operating margins shrank, and net margins contracted.

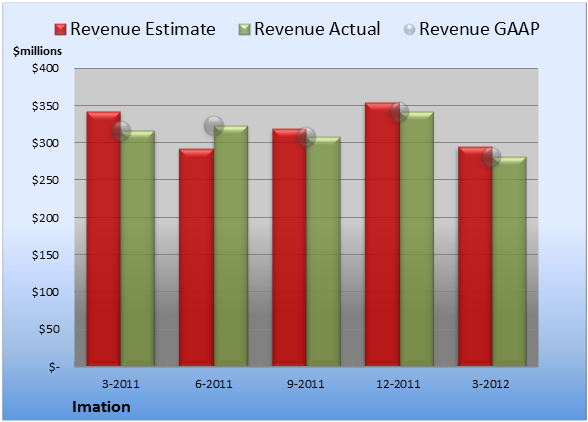

Revenue details

Imation booked revenue of $281.7 million. The one analyst polled by S&P Capital IQ looked for a top line of $295.0 million on the same basis. GAAP reported sales were 11% lower than the prior-year quarter's $316.5 million.

Source: S&P Capital IQ. Quarterly periods. Dollar amounts in millions. Non-GAAP figures may vary to maintain comparability with estimates.

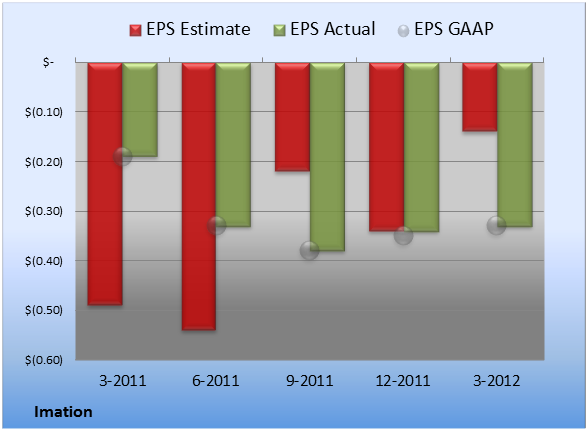

EPS details

EPS came in at -$0.33. The one earnings estimate compiled by S&P Capital IQ forecast -$0.14 per share. GAAP EPS were -$0.33 for Q1 against -$0.19 per share for the prior-year quarter.

Source: S&P Capital IQ. Quarterly periods. Non-GAAP figures may vary to maintain comparability with estimates.

Margin details

For the quarter, gross margin was 19.9%, 310 basis points better than the prior-year quarter. Operating margin was -2.7%, 210 basis points worse than the prior-year quarter. Net margin was -4.3%, 200 basis points worse than the prior-year quarter.

Looking ahead

Next quarter's average estimate for revenue is $276.0 million. On the bottom line, the average EPS estimate is -$0.20.

Next year's average estimate for revenue is $1.18 billion. The average EPS estimate is -$0.46.

Investor sentiment

The stock has a four-star rating (out of five) at Motley Fool CAPS, with 105 members out of 118 rating the stock outperform, and 13 members rating it underperform. Among 45 CAPS All-Star picks (recommendations by the highest-ranked CAPS members), 42 give Imation a green thumbs-up, and three give it a red thumbs-down.

Looking to profit from the makers of computer hardware? You may be missing something obvious about where the money will be made in the tech industry of the future. Is Imation on the right side of the revolution? Check out the changing landscape and meet the company that Motley Fool analysts expect to lead "The Next Trillion-Dollar Revolution." Click here for instant access to this free report.

Add Imation to My Watchlist.

At the time thisarticle was published Seth Jayson had no position in any company mentioned here at the time of publication. You can view his stock holdings here. He is co-advisor ofMotley Fool Hidden Gems, which provides new small-cap ideas every month, backed by a real-money portfolio. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.