How Low Will McMoRan Exploration Go?

Shares of McMoRan Exploration (NYS: MMR) hit a 52-week low yesterday. Let's look at how it got here and whether clouds are ahead.

How it got here

Like all natural gas producers, the falling price of natural gas hasn't helped McMoRan. But operational setbacks have helped drive the stock lower in recent months. In the most recent earnings call, management said that challenging conditions at the Davy Jones well have pushed out commercial production until at least the second quarter. For the full year 2012, production is expected to fall 28%, not good for a company that wasn't posting profits even at higher production levels.

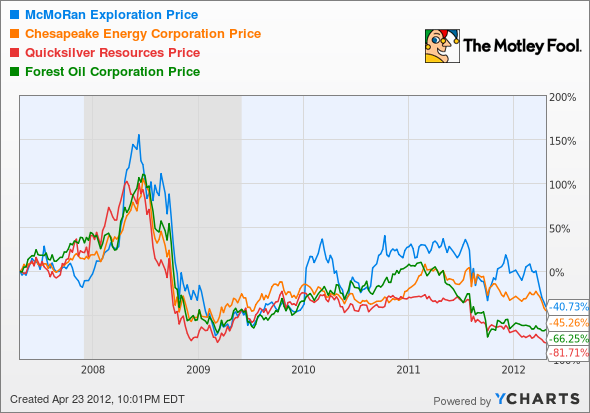

McMoRan isn't the only one hurting in the natural gas space. Quicksilver Resources (NYS: KWK) , Forest Oil (NYS: FST) , and Chesapeake Energy (NYS: CHK) have all been affected by falling natural gas prices since 2008, as their stock performance below shows. As companies transition from searching for more natural gas to trying to produce more oil, these stocks have found new lows.

As you can see below, McMoRan and Quicksilver have struggled mightily under low natural gas prices while Forest Oil and Chesapeake have been helped by a transition to liquids, keeping margins higher.

McMoRan | $1.34 billion | $529 million | 1% | ($0.56) |

Quicksilver Resources | $655 million | $892 million | 10.1% | ($0.15) |

Forest Oil | $1.36 billion | $704 Million | 19.6% | $1.10 |

Chesapeake Energy | $11.44 billion | $11.6 Billion | 15% | $2.79 |

Source: Yahoo! Finance.

Analysts don't have a lot of faith that the future looks better for McMoRan, predicting a $0.56 per-share loss in 2013. That scares me in the energy industry, where larger, more diversified competitors like ExxonMobil and Chevron are posting significantly better results.

What's next?

Natural gas simply isn't an area of the energy sector I would be jumping into right now. Prices are extremely low and even low-cost producers are struggling. I would look at companies that are making the transition to oil and have a bigger balance sheet to play with. An increase in oil production won't impact prices nearly as much as it has natural gas, and there doesn't appear to be enough of a cutback in natural gas production to make these companies profitable.

Chesapeake Energy is a good pick with a 7.8 trailing P/E, 6.4 forward P/E, and a 2% dividend yield. The company is a huge player in natural gas, giving investors exposure if the fuel takes off, but it has made a big push into liquids, which are driving earnings right now. I don't think we've seen the bottom yet for McMoRan Exploration.

Interested in reading more about McMoRan Exploration? Click here to add it to My Watchlist, which will find all of our Foolish analysis on this stock.

At the time thisarticle was published Fool contributorTravis Hoiumdoes not have a position in any company mentioned. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.Motley Fool newsletter services have recommended buying shares of Chesapeake Energy. The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.