Arctic Cat Roars to a 52-Week High: Can It Head Higher?

Shares of Arctic Cat (NAS: ACAT) hit a 52-week high on Friday. Let's take a look at how the company got there and whether clear skies are still in the forecast.

How it got here

You would think that a milder winter would be bad news for a company that generates most of its revenue from snowmobile sales, but it has been quite the opposite.

In its most recent quarter, Arctic Cat reported a 36% increase in sales from strength in its snowmobile and ATV product line. New models, as well as favorable pricing, have been driving strong margins that resulted in a 114% jump in operating profits. Snowmobile sales specifically jumped 61% and accounted for 60% of Arctic Cat's total sales. That's worrisome considering what little control Arctic Cat has over weather patterns that can be unkind and curb sales. It should also be noted that Arctic Cat purchased Suzuki's 6.1 million share stake in the company, which effectively reduces the amount of shares calculated against earnings and inflates reported EPS results.

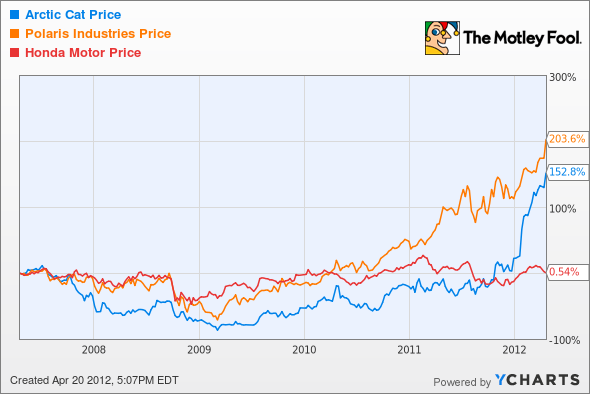

How it stacks up

Let's see how Arctic Cat stacks up next to its peers.

Arctic Cat is one of the few publicly traded snowmobile and ATV manufacturers, and shareholders have little to be upset about over the past five years.

Company | Price/Book | Price/Cash Flow | Forward P/E | 5-Year Revenue CAGR |

|---|---|---|---|---|

Arctic Cat | 4.1 | 9.0 | 17.3 | (8.7%) |

Polaris Industries | 10.9 | 18.7 | 17.4 | 9.9% |

Honda Motor | 1.2 | 6.4 | 9.8 | (2.1%) |

Sources: Morningstar and author's calculations. CAGR = compound annual growth rate.

Sales strength is prevalent across the board in snowmobiles and ATVs, with Polaris Industries (NYS: PII) posting a 63% rise in snowmobile sales. Even Honda Motor (NYS: HMC) , which has been hurt by a combination of flooding in Thailand and by the earthquake in Japan last year, sees ATVs as one of its few bright spots.

But when all is said and done, snowmobile sales represents less than one-quarter of Polaris' revenue and are just a fraction of Honda's. Comprising 60% of Arctic Cat's sales, you can see by the revenue growth figures above what a drastic reduction in sales the recession had on the company. It still has a long way to go to get back to its pre-recession levels. It's also worth noting that Honda and Polaris each pay out a dividend at or near 2% while Arctic Cat currently does not pay a dividend.

What's next

Now for the real question: What's next for Arctic Cat? That question really depends on whether the company can diversify its product line enough to weather inevitable cyclical downturns and if its product line can keep up with the larger Polaris.

Our very own CAPS community gives the company a two-star rating (out of five), with 65 of 99 members expecting it to outperform. Although I had not made a CAPScall as of yet on Arctic Cat, I'm going to use this time to now make an underperform call on the company. The reason for my call is pretty simple: valuation. Arctic Cat is a well-run company, but its product line is too reliant on snowmobile sales to drive growth. Furthermore, Arctic Cat's full-year sales are still considerably lower than at their peak before the recession, yet its stock price has far eclipsed those pre-recession highs despite similar EPS. The company's share buyback is a short-term bonus for shareholders, but this smoke-and-mirrors buyback isn't enough to mask the lack of a dividend and the huge stock run-up.

Craving more input on Arctic Cat? Start by adding it to your free and personalized watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Polaris Industries. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.