Verizon Points the Way to Another Mobile Revolution

Three months ago, Verizon (NYS: VZ) posted record-breaking holiday sales thanks to the Apple (NAS: AAPL) iPhone 4S. While revenue exploded, operating margins imploded, as the heavy subsidies Verizon and other carriers pay to Apple take a big bite out of carrier margins up front. Verizon's gross margin was 57.5% last quarter, down from 67.9% a year earlier, when the iPhone wasn't on the company's service menu.

Fast-forward to Wednesday night, and you heard Verizon singing a slightly different song.

First-quarter sales jumped 4.6% year over year to $28.2 billion. That's slower than the 7% annualized growth seen in the previous quarter. But don't cry for Verizon, because earnings soared 16% to $0.59 per diluted share. Both the top and bottom line beat the Street's expectations, by a significant margin in the case of earnings.

Yes, the company still sold a healthy dose of iPhones and other heavily subsidized smartphones in the first quarter, but Big Red got over the holiday subsidy hump in a hurry. Gross margins bounced back to 59.9%. If only the rest of us could work off Thanksgiving turkey and Christmas ham in a flash like that, the world would be a slimmer place (but maybe not happier).

But wait -- there's more!

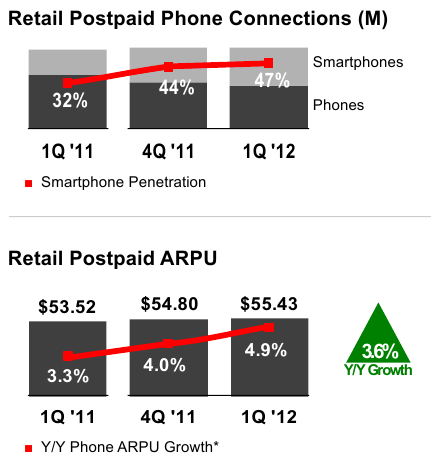

Verizon doesn't live and die by the iPhone alone, but smartphones in general are a very big deal. Consider these trends in tandem:

Source: Verizon. Data and charts used with permission.

As these charts show, more smartphone users lead to higher monthly fees. That's the whole idea behind trading initial subsidies for two-year commitments.

With 47% of Verizon's phone customers now slinging smartphones from the hip, the market is starting to become saturated. Expect AT&T (NYS: T) and Sprint Nextel (NYS: S) to report similarly high smartphone penetration numbers over the coming days, along with indications that smartphone growth probably peaked in the previous quarter.

Don't take that as a sign of impending industry doom, though. If you don't want a smartphone today, you pretty much have to settle for a so-called "feature phone," probably including features like a digital camera and SMS messaging powers. Five years ago, that was the hot item led by the Motorola RAZR, and it was getting hard to find simple phones that just let you make voice calls.

The same thing will happen again, making today's smartphones the de facto standard before you know it. For now, handset makers and service providers will set themselves apart with fancy new features and faster 4G networks -- Verizon grew its 4G customer base from 0.6% to 9.1% of all subscribers over the last five quarters, for example.

Looking ahead

This moment, right now, is a transitional period in the history of mobile communications. Verizon, Ma Bell, and other carriers are taking a bottom-line hit to establish themselves as smartphone powerhouses. When (and I do mean when, not if) the hardware subsidies fall out of fashion, the cash-making power will shift back to the networks and away from, chiefly, Apple.

And maybe that shift has started already. Without holiday-size device sales in this quarter, Verizon was free to build its cash stash instead. Operating cash flows increased year over year while capital expenses fell, and free cash more than tripled as a result. Tellingly, Verizon also "expects increasing free cash flow levels through 2012."

In short, Verizon's beefy dividend is not only safe as houses but sure to increase for many years to come. I can't say the same for your favorite handset maker as the mobile industry's power balance starts to shift. Find out more about sweet and stable dividend policies in this special report on rock-solid dividends for your portfolio. But grab your copy right away because the report won't be free for much longer.

At the time thisarticle was published Fool contributorAnders Bylundholds no position in any of the companies mentioned. Check outAnders' holdings and bio, or follow him onTwitterandGoogle+. The Fool owns shares of Apple.Motley Fool newsletter serviceshave recommended buying shares of and creating a bull call spread position in Apple. The Motley Fool has adisclosure policy. We Fools may not all hold the same opinion, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.