Deep Value Screams When the World Ignores a Supercycle

The coal industry is severely underfollowed and totally misunderstood. As a value investor, I thrive on precisely those sorts of conditions.

Major coal miner Peabody Energy (NYS: BTU) issued an audible wake-up call to the coal market Thursday by crushing analysts' consensus estimates by 24%, with adjusted first-quarter earnings per share of $0.67. Even while absorbing a $41 million hit related to weather-related disruptions to Australian met coal production in March, Peabody saw operating cash flow surge by 79% to $396 million alongside an 18% increase in EBITDA to $513 million.

Peabody has been trying to tell the world for years now that the global coal market is in the early stages of a long-term supercycle of significant proportions. Judging by the prevailing valuations of coal producers, that resilient outlook continues to fall on deaf ears. Instead, the market reacts with predictable nearsightedness to the popularized spoiler du jour. Late last year, a touch of relative softness in global steel production and commodity demand from China had investors ditching the supercycle thesis. But mining-equipment manufacturer Joy Global (NYS: JOY) attributed much of the met-coal weakness to steel inventory de-stocking in response to tightened Chinese credit policies. "With recently relaxed credit policies," Joy Global suggests, "dealers are expected to replenish their steel inventories in 2012, and this will add support to demand for met coal and iron ore."

This year, the substantially impaired U.S. market for thermal coal remains in focus after an unseasonably warm winter combined with cheap natural gas and regulatory uncertainty to yield a triple-whammy of domestic demand disruption. As serious as these threats to domestic demand have become, I maintain that the market's swift punishment of U.S. coal stocks has failed to take proper account of the increasing role that U.S. coal supplies will play in satisfying the long-term expansion of coal demand worldwide.

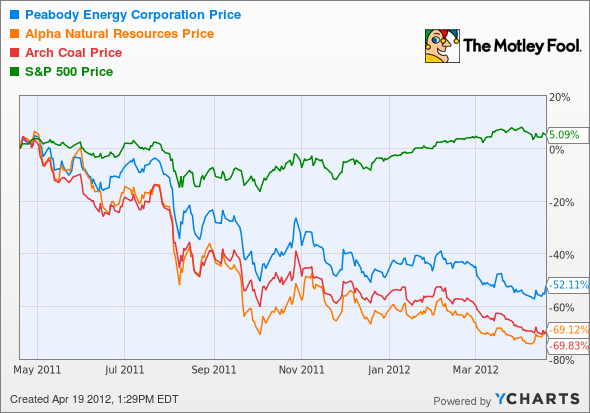

You can see the ferocity of the market's response to these concerns in the following one-year chart, which shows Peabody Energy suffering only a slightly less gruesome decline than rivals Arch Coal (NYS: ACI) and Alpha Natural Resources (NYS: ANR) .

Peabody deserves a solid premium over the competition

Simply stated, Peabody's global production portfolio, featuring world-class assets in Australia and prospective development projects in Asia, render the miner best positioned among its peers to meet the growing demand of the still-intact global coal supercycle. Just as importantly, Peabody's dominant position in both of the highly attractive domestic coal regions in which it operates gives the company a significant leg up on competitors like Arch and Alpha Natural, with exposure to the challenging Appalachian region of the eastern United States.

As I noted while offering Peabody Energy as my No. 1 energy pick for 2012, the company's senior vice president for investor and corporate relations, Vic Svec, opted to move his entire 401(k) into his company's stock after observing the disappearance of Peabody's customary valuation premium over its U.S.-based peers. I found his move a compelling testament to the conviction behind his bullish outlook, and I share his strongly held belief that Peabody Energy deserves a solid valuation premium over its less favorably positioned peers. But the opposite condition still lingers. Peabody trades for about 11 times estimated 2012 earnings, while Arch Coal shares enjoy a corresponding multiple of 16 times the consensus 2012 estimate. Taking expectations for both 2012 and 2013 into consideration, applying Arch Coal's forward P/E multiples to Peabody's earnings outlook implies a value of $44 to $50 just to match the Arch Coal multiple. Of course, Arch Coal's dividend yield of nearly 4.5% justifies some premium of its own, but I believe Peabody Energy's fundamentally more competitive position warrants, at the very least, a matching earnings multiple.

Because I consider the entire field undervalued in the wake of a sustained and overblown correction, I believe it would take a full doubling of the share price to approach fair value, even as adjusted for the possibility of sustained weakness in U.S. coal demand. I maintain that Peabody represented a serious bargain when I reinitiated my bullish CAPScall on the stock back in December, but I think it's a screaming value today after underperforming the S&P 500 by 19% in just four months.

All the world's a stage for coal

Peabody has stated its position over and over again, and it's about time the investment world began to take notice. The global coal supercycle is "alive and well," and Joy Global continues to corroborate that perspective with a forecast for incremental growth in annual demand for thermal coal of 300 million tons to fuel the roughly 90 gigawatts of coal-fired electricity plants currently under construction. Peabody's five-year outlook has only grown stronger since late 2010, as the company now calls for 1.3 billion tons of cumulative, incremental thermal-coal demand over the coming five-year period. Although the miner remains meaningfully exposed to U.S. utility demand, my value detector begins to buzz when I see Cloud Peak Energy (NYS: CLD) growing its exports to coal-hungry Asia by 42% during 2011.

Although dialed back slightly from calls last year for 300 million tons of incremental demand for metallurgical coal over the next five years, Peabody's still-exciting outlook for 50 million tons of new demand per year rests comfortably within supercycle-range. In my view, that renders the market for metallurgical coal one of the most compelling investment targets anywhere in the commodity complex. Given the stock's glaringly oversold condition after a brutal decline, I view junior producer Cline Mininga compelling option for value-hungry investors seeking targeted exposure to metallurgical coal. To track my ongoing coverage of both thermal and metallurgical coal markets, and the underfollowed stocks of the companies that mine them, I invite you to bookmark my article list or follow me on Twitter.

Like my colleague Sean Williams, I believe that now is the time to buy coal. Bargain valuations appear to abound in this deeply impaired segment of the commodity space, but nowhere do I find a more inviting combination of deep value, favorable competitive and geographical positioning, strategic growth potential, and proven execution than I do in the once and future king of coal: Peabody Energy.

Add Peabody Energy to My Watchlist.

Add Joy Global to My Watchlist.

Add Alpha Natural Resources to My Watchlist.

Add Arch Coal to My Watchlist.

Add Cloud Peak Energy to My Watchlist.

At the time thisarticle was published Fool contributorChristopher Barkercan be foundblogging activelyand acting Foolishly within the CAPS community under the usernameTMFSinchiruna. Hetweets. He owns shares of Alpha Natural Resources, Cline Mining, and Peabody Energy. The Motley Fool owns shares of Joy Global. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.