Spirit Airlines Just Hit a 52-Week High: Can It Head Higher?

Shares of Spirit Airlines (NAS: SAVE) just hit a 52-week high yesterday. Let's look at how the company got here and whether clear skies remain in the forecast.

How it got here

We are beginning to see a major shift from the dominance of national carriers to that of regional airlines, and Spirit Airlines is at the heart of the explosion in growth. Spirit, along with Allegiant Travel (NAS: ALGT) , a company I've profiled as my favorite play in the airline sector, are two discount airline companies that have really piled on the high-margin service fees to pad their bottom line. These discount airlines tease consumers with low rates, then let them choose high-margin optional fees that go almost exclusively to these airlines' bottom lines.

Spirit Airlines is a relative small-fry with just 37 planes at the end of fiscal 2011, but it is planning to add an additional seven in 2012. The key points here are that the law of big numbers is a long way off from catching up to Spirit, which could easily grow in excess of 20%, by my estimates, for many years to come, and that the company is rapidly growing capacity at a time when national carriers like United Continental Holdings (NYS: UAL) and Delta Air Lines (NYS: DAL) are reducing capacity to cut costs. That's a solid recipe for Spirit to continue to pick up market share.

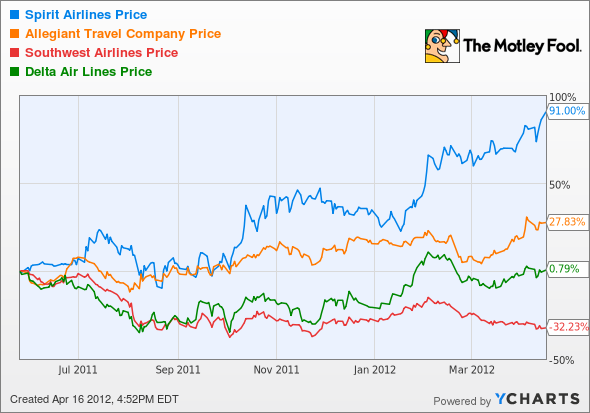

How it stacks up

Let's see how Spirit Airlines stacks up next to its peers.

Spirit is dominating its peers based on its performance since going public.

Company | Price/Book | Price/Cash Flow | Forward P/E | Cash / Debt |

|---|---|---|---|---|

Spirit Airlines | 3.4 | 6.9 | 9 | $343 million / $0 |

Allegiant Travel | 3.2 | 8.7 | 12.6 | $306 million / $146 million |

Southwest Airlines (NYS: LUV) | 0.9 | 4.5 | 8 | $3.14 billion / $3.75 billion |

Delta Air Lines | NM | 3.1 | 3.8 | $3.62 billion / $13.88 billion |

Sources: Morningstar, Yahoo! Finance. NM = not meaningful

As a capital-intensive business with razor-thin margins, having ample liquidity and being able to turn a profit are the two most important factors for any airline. Spirit is well-covered with absolutely no debt and $343 million in cash. In fact, it actually boasts a better net cash balance and a lower forward P/E and price-to-cash-flow than my sector favorite, Allegiant. Wall Street darling Southwest Airlines, on the other hand, has seen a net cash position turn into a net debt position of $617 million over the past year. National carriers continue to struggle despite their ebb-and-flow profitability. Delta, with its $10.3 billion in net debt, is a prime example of the risk associated with investing in the airline sector.

What's next

Now for the real question: What's next for Spirit Airlines? The answer really depends on whether it can continue to maintain and introduce what it refers to as its "optional fees" without alienating or angering its customer base.

Our very own CAPS community gives the company a two-star rating (out of five), with 35 of 49 members expecting it to outperform. Although I have not personally made a CAPScall on Spirit Airlines either way, I remain cautiously optimistic about its future. There's little denying that it appears cheap given its growth forecasts, and its balance sheet is impeccable. I am, however, concerned that the company's "charge first, ask questions later" business model could wind up ostracizing its customers over the long run. Spirit can get away with these extra fees because of extremely low teaser fares, but I wonder what will happen when more airlines attempt to follow suit? That's a tough question that only time can answer.

Craving more input on Spirit Airlines? Start by adding it to your free and personalized Watchlist. It's a totally free service offered by The Motley Fool to keep you current on the news and events you care about most.

At the time thisarticle was published Fool contributor Sean Williams has no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen name TMFUltraLong, track every pick he makes under the screen name TrackUltraLong, and check him out on Twitter, where he goes by the handle @TMFUltraLong.Motley Fool newsletter services have recommended buying shares of Southwest Airlines. Try any of our Foolish newsletter services free for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.