Sorry, Critics: Lululemon Will Keep Winning

Not everything is black and white when it comes to investing. Shares of yoga-apparel retailer lululemon athletica (NAS: LULU) may seem wildly overpriced, with a P/E of almost 60. However, they still trade at a bargain to their ultimate potential.

Haters be warned

Critics who can no longer dismiss Lulu as a passing trend now say that much of the growth is already indicated in the current share price. However, I think the naysayers underestimate management's ability to execute more growth strategies. The retailer also has a few tricks up its luon sleeves as it plans to launch new product categories and open in new markets later this year.

Last year, lululemon passed $1 billion in sales. Now, the company is laying the groundwork for record growth in 2012, with a showroom set to open in London later this month and another showroom in Hong Kong at the end of May. According to CEO Christine Day, shoppers in China don't mind paying up for the merchandise. In fact, Day says, "Many customers are coming into the Hong Kong store and buying in bulk."

Lulu has room to grow the business not only overseas, but also online. E-commerce sales increased 104% to $50 million for the fourth-quarter of fiscal 2011 -- representing about 13% of total sales. The company encourages shopping on its website by offering free shipping on any item, anytime. That's more than you can say for the competition. If that's not enough, the company plans to boost direct-to-consumer sales to more than 15% of net revenue in its next quarter.

Game on

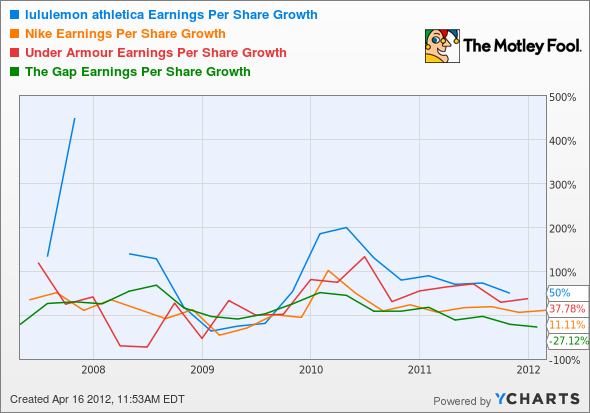

Lulu understands that part of its appeal is creating a positive customer experience. This has helped the company build a powerful brand, despite fierce competition from more established players such as Nike (NYS: NKE) and Under Armour (NYS: UA) , and even Gap (NYS: GPS) is getting in on the action, but Lulu has more yogi enthusiasm than these competitors and should be able to easily keep them at bay. Let's see how Lulu looks next to these rival sports-apparel names.

LULU Earnings Per Share Growth data by YCharts

Looking at earnings-per-share growth here, we can see that three of the four stocks are increasing in profitability, led by Lulu. Meanwhile, Gap shows declining profitability. Gap opened a chain of wannabe Lulu stores called Athletica in hopes of tapping into Lululemon's tremendous success in the niche market of yoga sportswear. The retail chain is so far behind Lulu, I doubt it will ever catch up.

Not only has Lululemon's explosive growth put it miles ahead of the competition, but also a rock-solid balance sheet with zero debt means the company has plenty of cash to fund future expansion. Lululemon is a quality company that I think will continue to be a winner. It's time for the critics to get onboard. Add these companies to MyWatchlist, The Motley Fool's free tool that lets you track and monitor your favorite stocks.

Add Under Armour to My Watchlist.

Add Nike to My Watchlist.

Add lululemon athletica to My Watchlist.

Add Gap to My Watchlist.

At the time thisarticle was published Fool contributor Tamara Rutter owns shares of Lululemon. Follow her onTwitter, where she uses the handle@TamaraRutter, for more Foolish insight and investing advice. The Motley Fool owns shares of lululemon athletica and Under Armour. Motley Fool newsletter services have recommended buying shares of lululemon athletica, Under Armour, and Nike and creating a diagonal call position in Nike. The Motley Fool has a disclosure policy. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.