How Low Will Telefonica Go?

Shares of Telefonica (NYS: TEF) just hit a 52-week low on Friday. Let's look at how the company got here and see whether cloudy skies remain in the forecast.

How it got here

Telefonica shares are suffering right along with those of Spanish large-cap bank Banco Santander (NYS: STD) , as the Spanish economy is grappling with how it should go about dealing with rising lending rates and a weakening economy. Spain's GDP is currently contracting at 0.3% while dealing with an absolutely unfathomable unemployment rate of 22.9%. With figures like these, it's easy to see where Wall Street gets its negativity surrounding Telefonica, considering the mess that Greece currently finds itself in.

The thing to remember with Telefonica is that, despite its reliance on the Spain for land-line and mobile revenue, it does have business divisions in Latin America and throughout Europe that are growing rapidly. Organic wireless-data revenue growth jumped 19% in its most recent quarter thanks to Latin America. But we need to also keep in mind that capital expenditures for Telefonica remain high. Between expansion into Latin America and big spectrum buys in Spain to spur growth, the company spent north of $10 billion on capital expenditures in 2011.

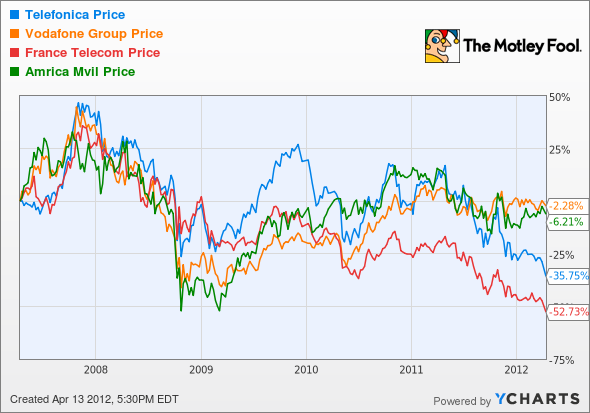

How it stacks up

Let's see how Telefonica stacks up with its peers.

Foreign telecoms have been a depressing sector for shareholders in recent years, which is why I have been recently flocking to this sector as a safe haven of value.

Company | Price/ Book | Price/ Cash Flow | Forward P/E | Dividend Yield |

|---|---|---|---|---|

Telefonica | 2.4 | 2.9 | 7.4 | 11% |

Vodafone Group (NYS: VOD) | 1 | 7.5 | 12.4 | 3.5% |

France Telecom (NYS: FTE) | 1 | 2.1 | 7.7 | 13% |

America Movil (NYS: AMX) | 3.4 | 6.1 | 10.6 | 1.1% |

Source: Morningstar. Yields are projected forward yields.

Based on these figures, you can probably get a feel for why I'm so bullish on foreign telecom companies. My Foolish colleague Anand Chokkavelu made France Telecom his stock to buy in March and even backed up his bullishness by purchasing the stock for his Rising Stars portfolio. Valued around book value and at a minuscule 2 times operating cash flow, it's a huge bargain in my eyes. The same can be said for Telefonica, which is valued at just 3 times operating cash flow and generated record free cash flow in its most recent quarter. America Movil, despite rising costs, reports double-digit revenue growth in its service and equipment segments, which makes it a compelling buy candidate as well. Vodafone Group might be the one exception of the bunch, since it reported a decrease in service revenue in Europe because of weakness from Italy and Spain.

What's next

Now for the real question: What's next for Telefonica? That question really depends on how much Spain's inability to cope with its enormous debt burden and high unemployment rates affects Telefonica's operations. In December, Telefonica announced that it was lowering its annual dividend by 14% in response to weakening market conditions, so clearly macroeconomic issues are weighing on the company.

Our very own CAPS community gives the company a highly coveted five-star rating, with an overwhelming 97.4% of members expecting it to outperform. Although I have not made a CAPScall on Telefonica before today's low, I am finally ready to back up my optimism on this stock and the sector with an outperform rating.

Telefonica clearly has built-in risks. You simply can't count on its dividend to continue to deliver double-digit yields, and you can almost bet on seeing rising capital expenditures bringing down earnings in the near term as the company will struggle to keep pace with its peers. But there's something to be said for a company that produces record cash flow in a country with 23% unemployment and a shrinking GDP. This is a survivor and at roughly 3 times operating cash flow is a bargain, too.

Craving more input on Telefonica? Start by adding it to your free and personalized Watchlist. It's a free service from The Motley Fool to keep you up to date on the stocks you care about most.

At the time thisarticle was published Fool contributorSean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, track every pick he makes under the screen nameTrackUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley fool owns shares of France Telecom.Motley Fool newsletter serviceshave recommended buying shares of France Telecom and Vodafone Group. Try any of our Foolish newsletter servicesfree for 30 days. We Fools don't all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.