How Much Is Melco Crown Really Worth?

I'm working my way around the gaming market, asking what each company is really worth. On Monday, I coveredLas Vegas Sands (NYS: LVS) , the most valuable company in gaming, and determined that the stock is overvalued based on my analysis.

Using those same assumptions, I'll take a look at Melco Crown (NAS: MPEL) today.

The little company that could

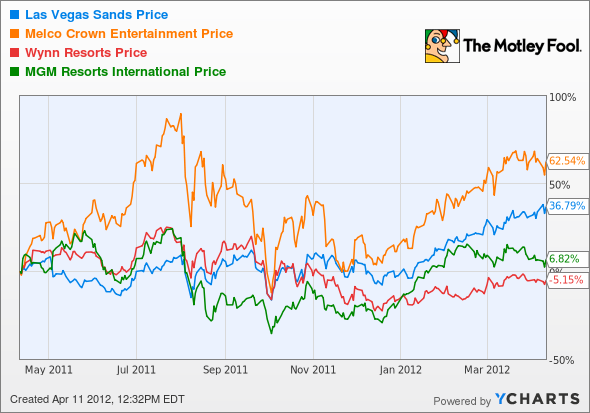

Melco Crown is the often forgotten company among Macau casino operators. Las Vegas Sands, MGM Resorts (NYS: MGM) , and Wynn Resorts (NAS: WYNN) capture most of the headlines, but it's the smaller Melco Crown that's outperformed all three over the past year.

Melco is also the only U.S.-traded casino company that's solely focused on Macau. It owns two major casinos and its Mocha Clubs. Altira, the company's first casino, is located on the island of Taipa, which is now connected to Cotai. But the real crown jewel is City of Dreams, the company's casino located across the street from The Venetian Macau and next to Sands Cotai Central, which opens today. When Wynn and MGM build developments on Cotai, they will be on the opposite side of the Venetian, surrounding City of Dreams in arguably the best location in Cotai.

Value versus size

Unlike with Las Vegas Sands, there aren't a lot of locations and other factors to consider when valuing Melco Crown. The company made $826.5 million in EBITDA in 2011, and if we assign the same eight to 10 times enterprise value multiple I used with Las Vegas Sands, it would indicate the company (including debt) is worth $6.6 billion to $8.3 billion. Now, subtract $1.2 billion in net debt and the equity should be $5.4 billion to $7.1 billion.

That is at the top end of the company's market cap of $7.1 billion as of last night.

As some argued in response to my Las Vegas Sands analysis, Macau gaming stocks could be worth more than the multiple I've assigned because infrastructure improvements are coming and gaming revenue will likely increase. Sands China is currently trading at 20.0 times trailing EBITDA and 12.3 times EBITDA if you assume Cotai Central will generate $1 billion in EBITDA, so comparison companies are even more expensive.

More upside potential

Unlike Las Vegas Sands and Wynn, Melco Crown still isn't hitting on all cylinders. The company's EBITDA margin in the fourth quarter was 23%, versus a 37.1% margin at The Venetian Macau and 34.3% at Wynn's resort.

This provides potential upside in operations and also shows that Melco Crown is not as efficient as competitors. In the past, the company has been aggressive working with junkets, like casinos who work with Asia Entertainment & Resources (NAS: AERL) , but as companies like Las Vegas Sands move into the junket market, the competition for this business is heating up.

The next two quarters should give us an idea of whether the company is losing junket business or junkets are losing power in the market as table game supply starts becoming more constrained. After Sands Cotai Central is opened, no new capacity is expected before 2015, so this should leave room for Melco to gain the upper hand on junkets and increase margins. That's one theory, anyway.

The other potential upside is more rooms Cotai is getting that cost Melco Crown absolutely nothing. Sands Cotai Central will add thousands of rooms next door and should bring more foot traffic into the casino. This could spell additional upside for Melco Crown.

Foolish bottom line

Melco Crown is trading at the top end of my enterprise value/EBITDA multiple of eight to 10 times, meaning the stock is probably fairly valued. I don't see it as a screaming buy, but I do think it's a better value than Las Vegas Sands at its current price.

For a stock pick that our analysts do think is a screaming buy, check out "The Motley Fool's Top Stock for 2012." The report highlighting this stock is yours free by clicking here.

At the time thisarticle was published Fool contributorTravis Hoiumdoes not have a position in any company mentioned. You can follow Travis on Twitter at@FlushDrawFool, check out hispersonal stock holdingsor follow his CAPS picks atTMFFlushDraw.The Motley Fool has a disclosure policy. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.