How High Can Coinstar Fly?

Shares of Coinstar (NAS: CSTR) hit a 52-week high yesterday. Let's look at how it got here and whether clear skies are ahead.

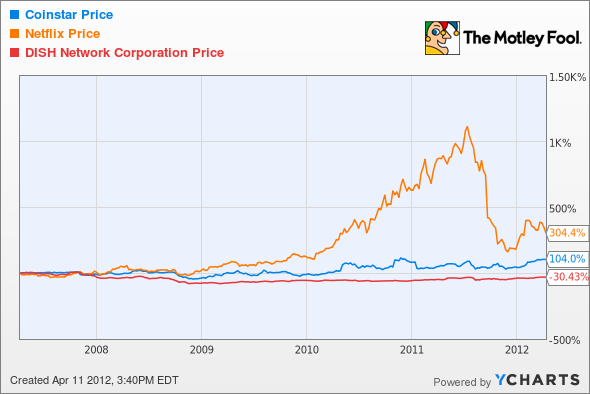

How it got here

Shares have enjoyed a healthy run so far this year, enjoying a gain of roughly 38% year to date.

I even started off the year by calling the stock a buy, primarily on strength in its Redbox division, which is driving all of the growth. Not long after that call (and accompanying CAPScall), the company posted a stellar quarter that blew past analyst estimates. The buck per share in profit trounced the $0.64 per share that the Street was looking for, while revenue similarly came in strong. The company also said it was buying NCR's (NYS: NCR) DVD kiosk business, taking out its closest competitor.

Around the same time, it also announced that it was hooking up with wireless carrier Verizon to at long last get into online streaming to threaten streaming king Netflix (NAS: NFLX) , after years of overpromising and nonexistent delivering on those promises.

Last month, Coinstar said Redboxes have now dispensed a cumulative total of 2 billion DVDs since inception.

The big earnings beat has provided the biggest catalyst for the recent run, as shares soared 19% on that day alone. Shares have been coasting higher ever since.

How it stacks up

Let's see how Coinstar stacks up with some of its peers and soon-to-be streaming competitors.

Let's add some fundamental metrics to the mix.

Company | P/E (TTM) | EPS Growth (5-Yr. Rate) | Net Margin (TTM) | ROE (TTM) |

|---|---|---|---|---|

Coinstar | 17.3 | 40.3% | 6.2% | 23.6% |

Netflix | 24.4 | 42.5% | 7.0% | 48.5% |

DISH Network (NAS: DISH) | 9.3 | 20.0% | 10.8% | N/A |

Source: Reuters. TTM = trailing 12 months. Note: DISH has negative shareholders' equity. N/A = not available.

As mentioned above, Coinstar's Redbox now has no meaningful direct competitors in the DVD kiosk business -- its greatest growth market. As it enters streaming, it will be going against Netflix, DISH's Blockbuster, Amazon.com's (NAS: AMZN) Prime Instant Video, and Hulu, among many others.

Amazon is aggressively growing its Prime Video library, but it's also getting in on app sales for its Kindle Fire and other types of digital content.

What's next

Coinstar still looks reasonably valued when you consider its strong growth prospects and return on equity.

There will always be a place in viewers' collective hearts for the instant gratification of picking up a DVD and staying in for the night -- a place that Redbox owns. I think Coinstar still has room to run.

Interested in more info on Coinstar? Add it to your watchlist byclicking here.

At the time thisarticle was published Fool contributorEvan Niuowns shares of Amazon.com and Verizon Communications, but he holds no other position in any company mentioned.Click hereto see his holdings and a short bio.Motley Fool newsletter serviceshave recommended buying shares of Netflix and Amazon.com. The Motley Fool has adisclosure policy.We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.