Will Google's Earnings Quality Hold Up?

Another earnings season is upon us, and it's make-or-break time for most publicly held companies. If a company exceeds Wall Street's expectations for revenue and earnings, the stock price could be off to the races. On the other hand, any shortfall could spell disaster. Coming up: Google (NAS: GOOG) , which reports after the market closes on Thursday.

Analysts expect Google to report $8.13 billion in revenue and $9.64 in earnings per share. EPS last year came in at $8.08 for the quarter and revenue was $6.54 billion, so if the company meets expectations, it will represent a healthy 19.3% year-over-year increase in EPS and a 24.3% revenue bump.

Google competes directly or indirectly with more than 1,500 companies in the IT space, including Yahoo! (NAS: YHOO) , Apple (NAS: AAPL) , Red Hat (NYS: RHT) , and RealNetworks. For comparison, let's look at their revenue and earnings expectations. (I selected a few of the more popular competitors so you can see how diverse a company Google really is.)

Company | Reporting Date | Revenue | EPS |

|---|---|---|---|

Yahoo! | April 17 | $1.06 billion | $0.17 |

Apple | April 24 | $36.04 billion | $9.80 |

Red Hat | June 28 (estimated) | $310.76 million | $0.27 |

RealNetworks | May 15 (estimated) | $65.96 million | ($0.29) |

When looking at earnings quality, we at The Motley Fool have two databases -- EQ Scan and EQ Score -- that help us uncover cash flow and revenue recognition issues. Smart financial officers can use several techniques to manipulate financial results, and manipulation of any of the three financial statements usually affects the other two. But a critical eye on these statements can often uncover trends that could be important to help protect investors from losing their hard-earned money. The EQ Score database assigns an index rank to a company from 1, for the lowest quality, to 5, for the highest. As the company's financial status changes over time, the database adjusts its rank and illuminates trends that will affect earnings quality going forward.

Let's see how the earnings quality stacks up for Google. The EQ Score model ranks Google as a "2," which is equivalent to a "D" letter grade.

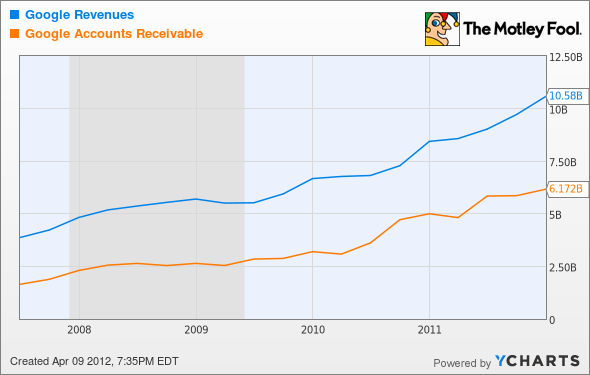

GOOG Revenues data by YCharts

Google's revenues are excellent, with an average year-over-year increase of 29% for the past four quarters. However, accounts receivable have also increased 32% on average for the past four quarters, and average quarterly receivables have increased from $3.565 billion to $4.675 billion over the past two years. The trend for receivables as a percentage of revenue has been rising and last quarter stood at 51%, the highest in three years.

Days sales outstanding, another metric that measures how well the company is managing its cash, also increased slightly on average during 2011, from 44 days to 45, with the fourth quarter of 2011 at 47 days -- again, the highest this metric has been in the past three years. In a nutshell, this is the reason for Google's earnings quality score.

In a recent commentary that I wrote comparing Apple, priceline.com (NAS: PCLN) , and Google, I noted that since the start of 2012, Google's share price has declined slightly. Last year's EPS came in at $36.04, and it's anticipated to be $42.58 this year and $50.17 in 2013. On a percentage-change basis, these numbers translate into 18.1% growth this year and 17.8% growth in 2013. The takeaway here is that Google's earnings trend is positive but is decelerating.

In the hierarchy of metrics that affect earnings quality, revenue is at the top of the chart, and cash flow is more important that net income. In other words, Wall Street tends to focus on the wrong metric as the basis for its recommendations to buy, hold, or sell a stock. Google is the preeminent global leader among Internet content providers and in several other areas, but its earnings quality is hurt by receivables that are rising both in terms of amounts owed and as a percentage of revenue, but also by the time it takes to collect amounts due. This not only acts as a drag on cash flow, but it also often portends weaker earnings in future quarters. Investors would be wise to keep an eye on Google's earnings quality in the quarters to come.

At the time thisarticle was published John Del Vecchiois the co-advisor to Motley Fool Alpha and co-manager of the Active Bear ETF. You may follow him on Twitter, where he goes by @johnfdelvecchio. He owns no shares in the companies mentioned in this article. The Motley Fool owns shares of Apple, Yahoo!, and Google.Motley Fool newsletter serviceshave recommended buying shares of priceline.com, Apple, Google, and Yahoo! and creating a bull call spread position in Apple. The Motley Fool has adisclosure policy. We Fools don't all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. Try any of our Foolish newsletter servicesfree for 30 days.The Motley Fool has adisclosure policy.

Copyright © 1995 - 2012 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.