What's Wrong With VMware Today?

Virtual computing giant VMware reported (link opens PDF) record fourth-quarter results last night. And it was good.

Sales jumped 22% year over year to $1.3 billion. Non-GAAP earnings soared 31% to $0.81 per share. The revenue figure was right in line with analyst expectations. Earnings crushed the $0.78 Street target.

That's where the fun ends. The company issued timid revenue guidance for the coming quarter and full year, and investors took that warning to heart in a hurry. Shares plunged as much as 22% overnight, setting new 52-week lows in the process.

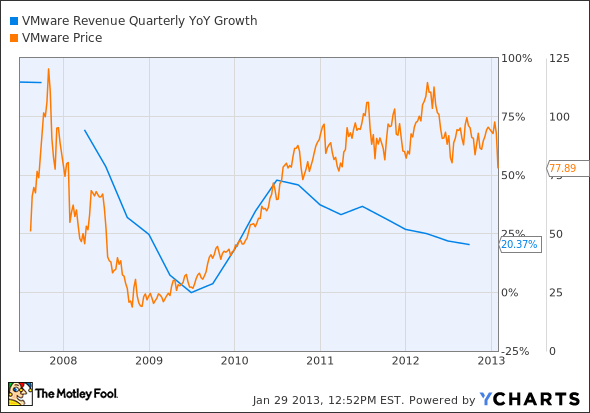

Management pointed to about 15% sales growth in 2013, starting with a 12% increase in the first quarter. That would be a drastic slowdown from 2012 levels, and from VMware's history in general. In fact, it looks like a return to the cold, sad days of the 2008 crisis. The early days of the recession were not kind to VMware:

VMW Revenue Quarterly YOY Growth data by YCharts.

Why the cloudy outlook? It's easy to jump to conclusions. The virtualization space is getting crowded, and sector leader VMware has more to lose than anyone else. Market share shifts could wreak havoc on this company's top line in a hurry.

CFO Jonathan Chadwick explained that he's making four important assumptions. The macroeconomic environment isn't improving as fast as he'd like. VMware made several huge deals in the first quarter of 2012, making for tough year-over-year comparisons this time. Many multiyear contracts are coming up for renewal in 2013 -- but mostly in the back half of the year, leaving little low-hanging renewal fruit for the first two quarters. Finally, VMware will refocus its business on core markets to set the stage for long-term growth. But again, the company will suffer right up front.

VMware is also sending some assets and employees off to work specifically on cloud computing services in a brand new joint venture with EMC . The storage giant already owns most of VMware, so this is strictly a family affair. But that's another potential driver of weaker top-line sales in the first half of 2013.

All things considered, I see this as a terrific investment window for long-term owners. Virtual computing is an unquestionable growth driver for the next five years or more. VMware is still the far-and-away leader of the pack. Nothing in this report shows any cracks in the core business, but you're getting a quick 20% discount based on a bundle of short-term concerns.

I'd start a bullish CAPScall here if I didn't already have one running.

The amount of data we store every year is growing by a mind-boggling 60% annually! To make sense of this trend and pick out a winner, The Motley Fool has compiled a new report called "The Only Stock You Need to Profit From the NEW Technology Revolution." The report highlights a company that has gained 300% since first recommended by Fool analysts but still has plenty of room left to run. Thousands have requested access to this special free report, and now you can access it today at no cost. To get instant access to the name of this company transforming the IT industry, click here -- it's free.

The article What's Wrong With VMware Today? originally appeared on Fool.com.

Fool contributor Anders Bylund holds no position in any company mentioned. Check out Anders' bio and holdings or follow him on Twitter and Google+.The Motley Fool owns shares of VMware and EMC. Motley Fool newsletter services have recommended buying shares of VMware. The Motley Fool has a disclosure policy.We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. Try any of our Foolish newsletter services free for 30 days.

Copyright © 1995 - 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.